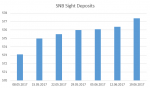

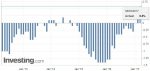

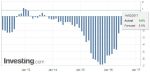

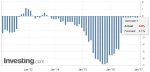

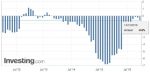

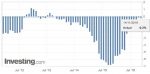

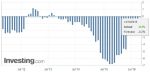

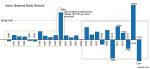

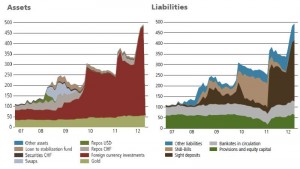

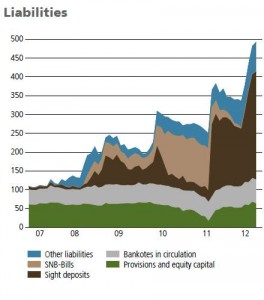

The sight deposits at the SNB decreased by 2.2 billion francs compared to the previous week.

Read More »2026-05-27

SNB Sight Deposits: decreased by 2.2 billion francs compared to the previous week

2026-05-27

The sight deposits at the SNB decreased by 2.2 billion francs compared to the previous week.

Read More »2026-05-25

Werbung / Sponsored ArticleDieser Beitrag wurde von CrownexCapitalGroup gesponsert. Die Darstellung basiert auf öffentlich verfügbaren Informationen und Angaben des Unternehmens. Die Finanzmärkte haben sich in den letzten Jahren erheblich verändert. Während ein Broker früher hauptsächlich als technischer Vermittler zwischen Investor und Börse wahrgenommen wurde, ist seine Rolle heute deutlich umfassender. Eine moderne Brokerplattform ist ein …

Read More »2026-05-16

EU regulation is moving fintech compliance from a back-office function into the centre of business strategy. For years, many fintech firms focused first on speed: launch the product, acquire users, then adapt controls later. That approach is becoming harder to defend. The new European regulatory environment is broader, more technical and more operational. It now …

Read More »2026-05-06

Learn how MAS licensing works under the Payment Services Act, what separates approved applications from rejected ones, and how Prifinance helps you get licensed faster.

Read More »2026-01-28

Vergleich der KMU-Rechnungslegung in Deutschland und der Schweiz: HGB und OR, Steuern, Bewertungsspielräume, Prüfung und Praxisfallen für den Mittelstand.

Read More »2025-11-15

For many people in the euro area, the “digital euro” still sounds like a distant central-bank experiment. In Lithuania, it is increasingly treated as something much more concrete: a piece of future-critical infrastructure that needs to work when other systems fail. The difference is partly geography and history. Lithuania is a small euro-area country …

Read More »2025-09-27

Mit der Reform wird der Eigenmietwert abgeschafft, dafür fallen Schuldzinsenabzüge (Hypothek, Lombard) weitgehend weg. Gewinner sind schuldenfreie Hauseigentümer, Verlierer sind Kreditnehmer. Mieter und Anleger ohne Kredit bleiben unverändert (EFD).

Read More »2025-07-16

In today’s rapidly changing world, where human attention has become the scarcest resource, practices that develop critical thinking, resilience, and mindfulness are more important than ever. One such practice is Go—an ancient strategic game from the East, over 2,500 years old. More than just an intellectual exercise, Go is a lifelong tool for personal …

Read More »2025-07-02

2025-05-28

2025-04-14

On Monday, April 14, 2025, during the European afternoon, the U.S. dollar experienced a notable decline against the Swiss franc, reversing earlier gains. This shift was primarily influenced by escalating trade tensions between the United States and China. Specifically, the U.S. administration announced the immediate implementation of tariffs on a range of Chinese imports, including …

Read More »2025-04-06

Reducing workload from 100% to 80% leads to a smaller proportional drop in after-tax income than in gross income. That’s a powerful financial lever for those considering part-time work:You’re “buying back time” at a discount, thanks to tax savings.

Read More »2025-03-23

Swiss National Bank (SNB) Policy Update Policy Rate Cut: SNB lowered its policy rate from 0.50% to 0.25% due to low inflationary pressure and rising downside risks. 2025 Outlook: The policy rate is expected to remain at 0.25% for the rest of the year.

Read More »2024-11-06

2024 vs 2020 same time vs 2020 final Time 05:32 UTC 2024 Nov6 05:36 UTC Nov 4, 2020 05:32 2024 near Final (Nov 18) Overall (image from Foxnews) Overall Harris: 59,248,216 votes Trump: 63,797,332 votes Biden: 60,995,579 votes (49.8%) Trump: 59,639,660 votes (48.6%) Biden: 79,308,019 votes (51%) Trump: 73,483,233 votes (47.3%) Georgia (screen) …

Read More »2024-10-17

As the 2024 US presidential election approaches, investors worldwide are closely monitoring potential ramifications on global markets, including the euro. The outcome of this election could significantly influence currency fluctuations, trade policies, and international relations as Republican candidate Donald Trump seeks to regain the White House from the Democratic party – which has nominated …

Read More »2024-05-21

Die Finanzmärkte durchlaufen derzeit eine Phase beträchtlicher Veränderungen, die von verschiedenen globalen und lokalen Faktoren beeinflusst werden. Wirtschaftliche Unsicherheiten und geopolitische Spannungen haben die Märkte volatiler gemacht, was sowohl Risiken als auch Chancen für Investoren mit sich bringt. Insbesondere die Schweizer Wirtschaft, bekannt für ihre Stabilität und Robustheit, muss sich an diese neuen Herausforderungen anpassen, um weiterhin erfolgreich zu sein.

Read More »2024-04-16

Die Luftfahrtindustrie ist ein integraler Bestandteil des globalen Transportsystems und verbindet Menschen und Güter über große Entfernungen hinweg. Im Jahr 2023 zeigte die Branche trotz beispielloser Herausforderungen aufgrund der COVID-19-Pandemie Widerstandsfähigkeit und Anpassungsfähigkeit. Während wir uns auf das Jahr 2024 vorbereiten, wollen wir uns die Zahlen aus dem Jahr 2023 genauer ansehen und die Prognose für den Luftfahrtsektor im kommenden Jahr erkunden.

Read More »2024-04-11

Switzerland is gaining recognition for something beyond its stunning landscapes and precision timepieces – its rapidly expanding online gambling industry. The remarkable growth in gaming platforms’ popularity has been partly fueled by the adoption of igaming white label casino online solutions. These pre-built, fully licensed operational setups allow new ventures to launch their online casinos or sports betting sites swiftly.

Read More »2024-01-11

Investieren unterscheidet sich grundlegend vom bloßen Spekulieren oder dem Hoffen auf schnelle Gewinne, wie man sie vielleicht in einem Casino erwarten könnte. Es geht vielmehr darum, durchdachte und informierte Entscheidungen zu treffen, die auf einer langfristigen Perspektive und einem Verständnis des Marktes basieren. Für Neulinge in der Welt der Finanzen kann dies eine Herausforderung darstellen, aber mit den richtigen Werkzeugen und Kenntnissen ist es ein durchaus erreichbares Ziel.

Read More »2024-01-09

Überweisungen kennen viele von uns, oder? In Deutschland haben wir viele Möglichkeiten, unser Geld sicher von A nach B zu überweisen. Doch was steckt eigentlich hinter diesen Methoden? Schauen wir uns die gängigsten Wege an. Was macht sie so besonders und sicher?

Read More »2023-12-08

Investors constantly seek new avenues for diversification and higher returns in the ever-evolving finance landscape. One such frontier that has gained significant attention in recent years is private credit. This alternative asset class offers unique opportunities and challenges, attracting institutional investors, high-net-worth individuals, and fund managers. In this comprehensive guide, we’ll explore the intricacies …

Read More »2023-11-29

For many, tax refunds feel like a mini-windfall—a delightful surprise at the beginning of the year. A chance to cover old debts, splurge on something desired, or simply bolster savings. But what happens when this eagerly anticipated money doesn’t arrive on time? Delays can, unfortunately, throw a wrench in your financial plans, causing unnecessary stress. …

Read More »2023-10-16

In today’s hyper-connected world, the efficient management of a company’s fleet is an imperative that can’t be overlooked. Businesses that rely on fleet operations must prioritize their management not only for financial prudence but also to ensure the safety and efficiency of operations. Whether you’re overseeing a fleet of delivery trucks, rental cars, or …

Read More »2023-10-13

Wahrscheinlich ist Ihnen schon aufgefallen, dass Ihre Gas- und Stromrechnungen teurer sind als früher. Falls Sie nach Möglichkeiten suchen, Ihre Stromkosten zu senken, gibt es viele einfache Maßnahmen, die Sie ergreifen können, um Ihre Energierechnungen zu senken – vom Ausschalten des Lichts bis hin zum kosteneffizienten Wäschewaschen. Hier finden Sie die 23 besten Möglichkeiten, …

Read More »2023-09-28

Finding the right retirement portfolio balance is an individual journey, especially in today’s ever-evolving environment. No two individuals are alike when it comes to investing and planning for financial security in retirement, which can make it daunting to find a suitable option that provides protection yet also offers growth potential. One less conventional …

Read More »2023-08-11

In today’s fast-paced world, technological advancements are changing the game in almost every industry. Restaurants, a sector once considered traditional and manual, are no exception. With the increasing demands of the 21st-century customer, the integration of technology has become inevitable. In this article, we will explore emerging technologies in restaurant management software, the benefits it …

Read More »2023-08-09

When discussing different ways to run an economy, one idea that stands out is the “free market” system. Instead of being a mouthful, it’s essentially a way of doing things where the government doesn’t get too involved, and businesses are free to compete. This setup has some pretty cool perks that can make life …

Read More »2023-08-08

Texas is not the only US state to have deregulated electricity. The states of Delaware, Connecticut, Maine, Massachusetts, and New Hampshire have several deregulated electricity zones as well. However, there are significantly more deregulated electricity sectors in Texas than in any other state. As per official reports, more than 26 million residents of the state live …

Read More »

Celebrating individual and team successes and encouraging team bonding are among the best ways of improving workplace culture. Employees who feel appreciated regardless of the team they are in are more likely to be highly productive, ensure their team succeeds, and be more motivated and energetic in the workplace. Here are a few ways your …

Read More »2023-07-21

Fleet management is a critical aspect of any business that utilizes multiple vehicles for its operations. It’s an area of business operations that can often seem riddled with complexity and high costs, especially for businesses with a large fleet. However, successful businesses find ways to minimize these costs while maintaining optimal fleet operations. This article …

Read More »2023-06-01

Year in and year out, online gambling continues to increase in popularity in Australia. With the industry’s growth, there has been a surge in the number of payment methods available to players. With the many payment options available, AstroPay stands out as one of Australia’s most secure and reliable online gambling options. What is AstroPay? …

Read More »2023-05-11

As a small business owner, there are numerous benefits to taking advantage of the tax incentives associated with life insurance. It can provide you and your loved ones financial security and help you maximize profits for your business in the long run. This article will explain the basics of life insurance for small business …

Read More »2023-05-08

The auto market can be challenging and unpredictable, but with the right strategies and insights, automotive business owners can thrive. This article will explore the financial savvy ways to succeed in the auto market, focusing on understanding the current landscape, saving money, using modern financial tools and AI, and navigating warranties and service contracts. …

Read More »2023-02-27

Are you looking to invest in Singapore but feeling overwhelmed by all the different options? Finding the correct brokerage account can be challenging, especially if you are not an experienced investor. That’s why we’ve broken down some of the top-rated brokers in Singapore, explaining the pros and cons each offers so you can choose which online trading platform is best for your needs.

Read More »2022-12-20

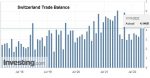

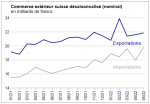

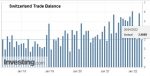

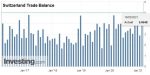

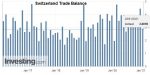

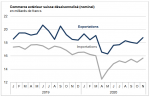

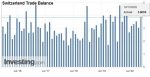

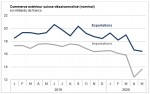

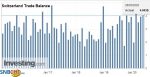

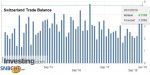

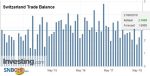

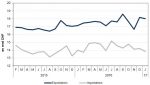

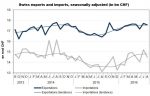

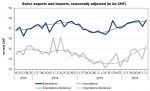

In November 2022, seasonally adjusted exports plunged by almost a tenth while imports increased by 1.4% month on month. At the exit in particular, the chemical-pharmaceutical sector weighed down the result. The trade balance closes with a small surplus of half a billion francs.

Read More »2022-11-18

In October 2022 and after two consecutive monthly increases, seasonally adjusted exports fell by 1.1% (real: −1.8%). However, they remain on a positive trend. Imports fell by 1.4% over one month (actual: −0.8%), but have stagnated since the middle of the year. The trade balance ends with a surplus of 3 billion francs, the highest recorded in the last six months.

Read More »2022-10-20

Also in the 3rd quarter of 2022, Swiss foreign trade experienced a positive development: while exports increased by 1.3%, imports grew by 0.8%. However, the latter have lost their vigor since the middle of the year. Both imports and exports nevertheless posted a record quarterly result. The trade balance closes with a surplus of 8 billion francs.

Read More »2022-07-29

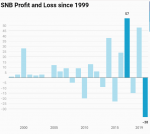

I was predicting for many years that the SNB will suffer a big loss when inflation comes. The time of reckoning has come. I expected some 150 billion loss in one year: at half time we are 95 billion CHF.

Read More »2022-07-19

Swiss foreign trade strengthened further in both traffic directions in the 2nd quarter of 2022, reaching new highs. Exports increased by 0.9% and imports by 2.4% compared to the previous quarter. Prices have risen both at entry and exit. The trade balance closes with a surplus of 7.6 billion francs.

Read More »2022-06-22

In May 2022, Swiss foreign trade strengthened in both directions of traffic: seasonally adjusted exports increased by 1.2% while imports jumped by 10.3%. The latter thus confirmed their upward trend despite strong fluctuations. Due to the different pace of growth at the outflow and the inflow, the trade balance surplus stood at CHF 2.0 billion.

Read More »2022-05-03

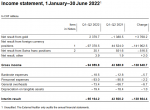

The Swiss National Bank reports a loss of CHF 32.8 billion for the first quarter of 2022. The loss on foreign currency positions amounted to CHF 36.8 billion. A valuation gain of CHF 4.2 billion was recorded on gold holdings. The profit on Swiss franc positions was CHF 10.6 million.

Read More »2022-04-27

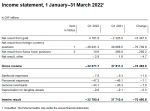

Swiss foreign trade also grew in the 1st quarter of 2022, climbing to a record level. Imports strengthened further (+6.7%) while exports lost ground somewhat (+1.2%). Both at entry and exit, prices stood at very high levels. Due to different trends in the two directions of traffic, the trade balance surplus fell sharply (–2.8 billion francs).

Read More »2022-03-18

In February 2022, seasonally adjusted exports jumped 15.4% – after their setback in the previous two months – while imports fell 2.9%. The output boom was driven by the strength of chemicals and pharmaceuticals. For the first time, the trade balance surplus passed the 5 billion franc mark.

Read More »2022-01-27

After a year 2020 strongly affected by the Covid-19 pandemic, Swiss foreign trade proved to be very dynamic in 2021. Exports thus jumped by 15.2% – reaching a record level – while imports swelled by 10 .1%. The different pace of growth at entry and exit explained the jump in the trade surplus to the imposing level of 58.7 billion francs.

Read More »2021-11-18

In October 2021, Swiss foreign trade lost its vigor. Exports declined 1.4% and imports 2.3% from the previous month. The chemicals and pharmaceuticals sector weighed on the results in both directions of traffic. The trade balance closed with a surplus of 4.4 billion francs, similar to that of previous months.

Read More »2021-10-29

The Swiss National Bank reports a profit of CHF 41.4 billion for the first three quarters of 2021. The profit on foreign currency positions amounted to CHF 42.2 billion. A valuation loss of CHF 1.3 billion was recorded on gold holdings. The profit on Swiss franc positions amountedto CHF 0.8 billion.

Read More »2021-09-23

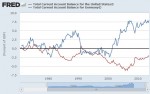

In the second quarter of 2021, the current account surplus amounted to almost CHF 11 billion, CHF 7 billion higher than in the same quarter of 2020. The rise was mainly attributable to a higher receipts surplus in goods trade.

Read More »2021-08-19

Secondary sector production rose by 14.2% in 2nd quarter 2021 in comparison with the same quarter a year earlier. Turnover rose by 15.5%. These sharp increases can largely be explained by the weak 2nd quarter of 2020, during which measures against the COVID-19 pandemic came into effect.

Read More »2021-07-20

Swiss foreign trade showed dynamism in the second quarter of 2021. Exports rose 3.2% to a record level. They posted a fourth consecutive quarterly increase since the drop recorded at the start of the coronavirus pandemic. Imports continued the momentum of the previous quarter and increased 3.8%. The trade surplus stood at 11.5 billion francs.

Read More »2021-05-27

After jumping 5.9% in March, exports stagnated in April, however, rising to a high level of 20 billion francs. Imports confirmed their vitality in previous months, up 3.5% to 16.8 billion francs (actual: + 2.2%). The trade balance closes with a surplus of 3.3 billion francs.

Read More »2021-04-23

During the 1st quarter of 2021 and on a seasonally adjusted basis, exports increased by 4.8% (+ 2.7 billion francs; actual: + 4.9%), signing a third consecutive quarterly increase. At 58.1 billion francs, they not only exceeded their pre-crisis level, but also their second largest quarterly result. Imports increased by 1.7% or 805 million francs (actual: + 1.9%).

Read More »2021-03-04

Bern, 04.03.2021 – The 2020 statistics of the Federal Customs Administration (AFD) are strongly influenced by the COVID-19 pandemic. In order to reduce the risk of transmission of the coronavirus, Switzerland has reintroduced systematic checks at national borders for the first time since joining Schengen, imposed entry restrictions and temporarily closed small border posts.

Read More »2021-03-01

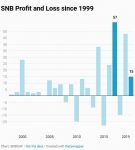

The Swiss National Bank reports a profit of CHF 20.9 billion for 2020 (2019: CHF 48.9 billion). The profit on foreign currency positions amounted to CHF 13.3 billion. A valuation gain of CHF 6.6 billion was recorded on gold holdings. The profit on Swiss franc positions was CHF 1.3 billion.

Read More »2021-02-18

After declining in December 2020, Swiss foreign trade again showed a strong increase at the start of 2021. In January and in seasonally adjusted terms, exports rose 5.4% to 18.9 billion francs and imports by 3.3% to 15.3 billion. In both directions of trafficking, the boom relied heavily on chemicals and pharmaceuticals. The trade balance closed with a surplus of 3.6 billion francs.

Read More »2021-01-28

Switzerland’s 2020 foreign trade will bear the brunt of the consequences of the COVID-19 pandemic: exports (-7.1% to 225.1 billion francs) and imports (-11.2% to 182.1 billion) posted a historic decline. Never before have they suffered such a significant quarterly decline as in the second quarter of 2020. Foreign trade has fallen back to its level recorded three years earlier. The trade balance closed the year with a record surplus of CHF 43.0 billion.

Read More »2021-01-19

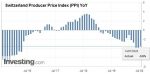

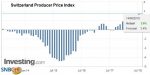

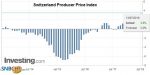

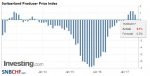

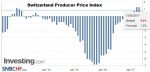

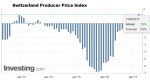

The Producer and Import Price Index rose in December 2020 by 0.5% compared with the previous month, reaching 98.4 points (December 2015 = 100). Compared with December 2019, the price level of the whole range of domestic and imported products fell by 2.3%.

Read More »2021-01-05

In the third quarter of 2020, the current account surplus amounted to CHF 9 billion, CHF 3 billion less than in the same quarter of 2019. This decline was particularly due to the lower receipts surplus in trade in goods and services. In the case of the goods trade, the decline was attributable to gold trading. This decrease was curbed by the expenses surplus for primary and secondary income, which decreased compared to Q3 2019.

Read More »2020-12-17

In November 2020, Swiss foreign trade stood out with an increase in both directions of traffic. In seasonally adjusted terms, exports advanced 4.8% and imports 4.2%. Falling over the previous two months, exports resumed their growth path and the trade balance closed with a surplus of 3.1 billion francs.

Read More »2020-12-15

The Producer and Import Price Index fell by 0.1% in November 2020 compared with the previous month. The index stood at 97.9 points (December 2015 = 100). This decline was due in particular to lower prices for petroleum products and pharmaceutical preparations.

Read More »2020-11-19

In October 2020, Swiss foreign trade took off. In seasonally adjusted terms, exports stagnated (-0.4%) while imports fell 3.3%. The slowdown recorded since this summer in both directions of traffic has thus been confirmed. The trade balance closed with a surplus of 2.9 billion francs.

Read More »2020-11-18

Over the last 48 hours, Switzerland’s Federal Office of Public Health (FOPH) reported a further 227 deaths among laboratory-confirmed Covid-19 cases, bringing the death toll to 1,654 since summer and 3,385 since the beginning of the year.

Read More »2020-11-16

Over the last 72 hours, Switzerland’s Federal Office of Public Health (FOPH) reported 198 deaths among laboratory-confirmed Covid-19 cases, bringing the death toll to 1,427 since summer and 3,158 since the beginning of the year.

Read More »2020-11-13

Over the 7 days to 13 November 2020, Switzerland’s Federal Office of Public Health (FOPH) reported 553 deaths among laboratory-confirmed Covid-19 cases, bringing the death toll to 1,229 since summer and 2,960 since the beginning of the year.

© Sudok1 | Dreamstime.comThe 553 reported deaths this week represent 19% of the total so far, making the last 7 days the deadliest 7-day period since the virus arrived in Switzerland.

There are currently 3,945 Covid-19 patients in hospitals across Switzerland, according to FOPH figures published by RTS, a number significantly above the peak during the first wave.

Switzerland is currently using 77% of its current intensive care capacity (1,142 places), according to SRF. The number of Covid patients in intensive care has reached 512, a number

Read More »2020-11-10

On 9 November 2020, Switzerland’s Federal Office of Public Health (FOPH) reported 17,309 new laboratory-confirmed Covid-19 cases over 72 hours, bringing the total to 229,222.

Read More »2020-11-06

On 5 November 2020, Switzerland’s Federal Office of Public Health (FOPH) reported 62 deaths among laboratory-confirmed cases of Covid over 24 hours, bringing the total death toll since summer to 606.

Read More »2020-10-31

The Swiss National Bank reports a profit of CHF 15.1 billion for the first three quarters of 2020. We explain why these profits are possible.

Read More »2020-10-21

The second wave of the Coronavirus is currently raging in Europe. The attached image shows the number of newly infected people in European countries on a linear scale. In particular in the Czech republic, but also in Switzerland, France or Spain, one can see a tendency of exponential growth.

Read More »2020-10-20

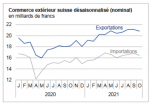

After its historic decline in the second quarter, Swiss foreign trade showed a clear recovery in the third quarter of 2020. In seasonally adjusted terms, exports swelled by 6.5% and imports by 11.5%. The two traffic departments, however, remained well below their record level for the second quarter of 2019. The trade balance closed with a surplus of 8.2 billion francs.

Read More »2020-10-15

The Producer and Import Price Index rose in September 2020 by 0.1% compared with the previous month, reaching 98.0 points (December 2015 = 100). The rise is due in particular to higher prices for scrap as well as for basic metals and semi-finished metal products.

Read More »2020-09-23

In the second quarter of 2020, the current account surplus amounted to CHF 10 billion; in the same quarter of 2019 it was CHF 21 billion. This decline was principally due to lower receipts from direct investment abroad. While the goods trade balance and the services trade balance changed only marginally, there was a significant decrease in receipts and expenses.

Read More »2020-09-16

The Producer and Import Price Index fell in August 2020 by 0.4% compared with the previous month, reaching 97.9 points (December 2015 = 100). This decline was due in particular to lower prices for chemical and pharmaceutical products. Compared with August 2019, the price level of the whole range of domestic and imported products fell by 3.5%.

Read More »2020-08-17

The Producer and Import Price Index rose in July 2020 by 0.1% compared with the previous month, reaching 98.3 points (December 2015 = 100). The rise is due in particular to higher prices for petroleum products. Compared with July 2019, the price level of the whole range of domestic and imported products fell by 3.3%.

Read More »2020-08-03

Fed and ECB money printing and massive fiscal stimulus help the SNB to come back into positive territory for the year.

The renewed asset price inflation compensate for losses on the US dollar.

2020-07-21

Swiss foreign trade recorded a record decline in the second quarter of 2020. In seasonally adjusted terms, exports plunged by 11.5% compared to the previous quarter and imports even by 16.0%. This result stems from the traffic collapse recorded in April in the wake of the coronavirus pandemic, with May and June having regained some color. The trade balance closed with a record surplus of 9.6 billion francs.

Read More »2020-07-14

14.07.2020 – The Producer and Import Price Index rose in June 2020 by 0.5% compared with the previous month, reaching 98.1 points (December 2015 = 100). The rise is due in particular to higher prices for petroleum products as well as petroleum and natural gas. Compared with June 2019, the price level of the whole range of domestic and imported products fell by 3.5%.

Read More »2020-06-29

Key figures: Current Account: Down 13.72% against Q1/2019 to 17.4 bn. CHF of which Goods Trade Balance: Plus 8.05% against Q1/2019 to 17.4 bn. of which the Services Balance: Minus 53.84% to 3.02 bn. of which Investment Income: Minus 0.54% to 6.3 bn. CHF.

Read More »2020-06-18

After its historic setback of the previous month, foreign trade recovered a few colors in May 2020. Imports posted a seasonally adjusted increase of 9.8% to 13.6 billion francs; however, they are still below their March 2020 level. Although exports fell again (-1.2%), they eased compared to April. The trade balance closed with a surplus of 2.8 billion francs.

Read More »2020-06-15

15.06.2020 – The Producer and Import Price Index fell in May 2020 by 0.5% compared with the previous month, reaching 97.6 points (December 2015 = 100). This decline is due in particular to lower prices for pharmaceutical and chemical products as well as for petroleum products. Compared with May 2019, the price level of the whole range of domestic and imported products fell by 4.5%.

Read More »2020-05-26

Compared with the previous month, April 2020 exports contracted by 11.7% (actual: -10.0%); this is the largest seasonally adjusted decline ever recorded. They retracted by 2.2 billion to reach 16.7 billion francs. Imports even plunged by 21.9%, that is, by a drop of 3.5 billion francs, to 12.4 billion francs (actual: -17.8%); they thus fell almost to their July 2005 level. The trade balance closed with a record monthly surplus of 4.3 billion francs.

Read More »2020-05-14

14.05.2020 – The Producer and Import Price Index fell in April 2020 by 1.3% compared with the previous month, reaching 98.1 points (December 2015 = 100). The decline is due in particular to lower prices for petroleum products, petroleum and natural gas. Compared with April 2019, the price level of the whole range of domestic and imported products fell by 4.0%.

Read More »2020-05-11

2020-04-24

The Swiss National Bank reports a loss of CHF 38.2 billion for the first quarter of 2020. The loss on foreign currency positions amounted to CHF 41.2 billion.

Read More »2020-04-22

The boom in chemicals and pharmaceuticals enabled Swiss exports to increase in March as well as in the first quarter of 2020 (+ 2.2% respectively + 1.0%). Despite the global economic situation linked to the “Covid-19”, the performance of this sector offset the decline suffered by most of the other groups. As in the previous quarter, seasonally adjusted imports fell (- 2.8%). The trade balance for the first three months of 2020 ends with a surplus of 8.3 billion francs.

Read More »2020-04-16

16.04.2020 – The Producer and Import Price Index fell in March 2020 by 0.3% compared with the previous month, reaching 99.4 points (December 2015 = 100). This decline is due in particular to lower prices for petroleum products. Compared with March 2019, the price level of the whole range of domestic and imported products fell by 2.7%.

Read More »2020-03-23

In the fourth quarter of 2019, the current account surplus was CHF 26 billion, CHF 11 billionmore than in Q4 2018. The increase was primarily attributable to the higher receipts surplus in investment income and goods trade. The transactions reported in the financial account showed a net acquisition of financial assets (CHF 40 billion) and a net incurrence of liabilities (CHF 19 billion) in Q4 2019.

Read More »2020-03-22

Key for understanding the expansion of the Coronavirus, is the slope (or steepness / derivation) of the curve.

This post compares the slope values of different countries.

2020-03-19

After their strong increase the previous month, exports plunged 5.0% in February 2020 and thus continue on their negative trend that started in September 2019. Imports weakened by 1.4%. The trade balance closed with a surplus of 2.0 billion francs.

Read More »2020-03-02

The increasing volatility of SNB Earnings Annual results are not really definite. Given that the SNB accumulates foreign currencies with interventions, they have huge swings. But the SNB may lose 50 billion in one year and win 60 billion in the next year or vice verse. Good years of the Credit Cycle This trend was … Continue reading »

Read More »2020-02-26

We suggest that the first month of a bigger virus outbreak is a good time for buying stocks. History has proven this timing decision right.

Read More »2020-02-20

20.02.2020 – Secondary sector production rose by 1.3% in 4th quarter 2019 in comparison with the same quarter a year earlier. Turnover rose by 0.3%. This rise has continued without interruption since the 1st quarter 2017 but was slightly weaker in the reporting quarter. This is shown by provisional results from the Federal Statistical Office (FSO).

Read More »2020-02-14

The Producer and Import Price Index remained unchanged in January 2020 compared with the previous month. The index stood at 100.7 points (December 2015 = 100). Petroleum products in particular saw higher prices, while pharmaceutical preparations became cheaper. Compared with January 2019, the price level of the whole range of domestic and imported products fell by 1.0%.

Read More »2020-01-28

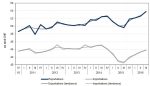

Despite a climate of uncertainty linked to trade tensions and the global economy, Swiss foreign trade grew in 2019, albeit at a slower pace. Exports increased by 3.9% to 242.3 billion francs while imports increased by 1.6% to 205.0 billion francs, the two directions of traffic thus reaching an historic peak. The trade balance closed with a record surplus of 37.3 billion francs.

Read More »2020-01-17

17.01.2020 – The Producer and Import Price Index rose in December 2019 by 0.1% compared with the previous month, reaching 100.7 points (December 2015 = 100). Compared with December 2018, the price level of the whole range of domestic and imported products fell by 1.7%. The average annualised inflation rate in 2019 was –1.4%.

Read More »2019-12-20

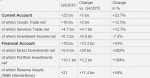

In summary: Nearly any change against the third quarter of 2018. About the same figures. But clearly and – as usual – a massive surplus. Key figures: Current Account: Up 39.15% against Q3/2018 to 18.09 bn. CHF. of which Goods Trade Balance: Plus 49.78% against Q3/2018 to 16.76 bn. of which the Services Balance: Minus 12.94% to 5.25 bn.

Read More »2019-12-19

As in the previous month, cross-border flows of goods fell in both directions of traffic in November 2019. In seasonally adjusted terms, exports fell 1.7% on a month compared to 1.1% for imports. Swiss sales fell back to their level at the start of 2019, while admissions fell by almost a billion francs. The trade balance closed with a surplus of 2.2 billion francs.

Read More »2019-12-12

12.12.2019 – The Producer and Import Price Index fell in November 2019 by 0.4% compared with the previous month, reaching 100.5 points (December 2015 = 100). This decline was due in particular to lower prices for chemical and pharmaceutical products. Compared with November 2018, the price level of the whole range of domestic and imported products fell by 2.5%.

Read More »2019-11-19

In October 2019, Swiss foreign trade declined in both traffic directions. Exports fell sharply (-5.3%); however, they had jumped 8.8% the previous month, setting the bar very high. Imports fell 2.4%. Since the beginning of the year, foreign trade has thus revealed stagnation. The trade balance closes with a surplus of 2.4 billion francs.

Read More »2019-11-14

The Producer and Import Price Index fell in October 2019 by 0.2% compared with the previous month, reaching 100.9 points (December 2015 = 100). Compared with October 2018, the price level of the whole range of domestic and imported products fell by 2.4%.

Read More »2019-10-17

In the third quarter of 2019, foreign trade showed a positive trend: while exports rose by 0.9%, imports posted double growth (+ 1.8%). Both the first and the second have achieved a record quarterly result. The trade balance is closing with a surplus of 5.9 billion francs.

Read More »2019-10-15

15.10.2019 – The Producer and Import Price Index fell in September 2019 by 0.3% compared with the previous month, reaching 101.1 points (December 2015 = 100). This decline is due in particular to lower prices for petroleum products and scrap. Compared with September 2018, the price level of the whole range of domestic and imported products fell by 2.0%.

Read More »2019-10-02

Dear readers, SNBCHF has changed sending service. If you are missing the daily newsletters, please look in your spam or quarantine program.

Read More »2019-09-20

The assets side of the financial account registered a total net acquisition of CHF 11 billion (Q2 2018: net reduction of CHF 30 billion). Other investment contributed CHF 7 billion to this net acquisition (Q2 2018: net reduction of CHF 36 billion), in part because the SNB increased its foreign claims in connection with repo transactions.

Read More »

In August 2019, Swiss exports fell for the second month in a row. Down 4.3% year-on-year, they dropped below 19 billion francs. On the other hand, imports rose by 3.4% and thus regained their level at the beginning of the year. The trade balance closed with a surplus of 1.2 billion francs.

Read More »2019-09-12

12.09.2019 – The Producer and Import Price Index fell in August 2019 by 0.2% compared with the previous month, reaching 101.4 points (December 2015 = 100). The decline is due in particular to lower prices for rubber and plastic products as well as basic metals and semi-finished metal products. Compared with August 2018, the price level of the whole range of domestic and imported products fell by 1.9%.

Read More »2019-08-20

After shining the previous month, foreign trade turned red in July 2019. Despite a decline of 3.9% to 19.6 billion francs, exports had their second largest monthly result ever reached. Down 1.7%, imports were close to CHF 17 billion. The chemistry-pharma has greatly impacted both directions of the traffic. The trade balance is closing with a surplus of 2.7 billion francs.

Read More »2019-08-15

15.08.2019 – The Producer and Import Price Index fell by 0.1% in July 2019 compared with the previous month, reaching 101.6 points (December 2015 = 100). The decline is due in particular to lower prices for scrap as well as petroleum and natural gas. Compared with July 2018, the price level of the whole range of domestic and imported products fell by 1.7%.

Read More »2019-07-31

The Swiss National Bank reports a profit of CHF 38.5 billion for the first half of 2019. The profit on foreign currency positions amounted to CHF 33.8 billion. A valuation gain of CHF 3.8 billion was recorded on gold holdings. The profit on Swiss franc positions was CHF 1.1 billion. The SNB’s financial result depends largely on developments in the gold, foreign exchange and capital markets.

Read More »2019-07-18

In the second quarter of 2019, exports increased by 1.4% and imports by 0.2%. The two traffic departments have thus set a record quarterly result. The trade surplus, on the other hand, stood at 6.8 billion francs.

Read More »2019-07-15

The Producer and Import Price Index fell in June 2019 by 0.5% compared with the previous month, reaching 101.7 points (December 2015 = 100). The decline is due in particular to lower prices for petroleum products, petroleum and natural gas as well as basic metals and semi-finished metal products. Compared with June 2018, the price level of the whole range of domestic and imported products fell by 1.4%.

Read More »2019-06-24

In the first quarter of 2019, the current account surplus amounted to CHF 17 billion, on a par with the same quarter of 2018. Trade in services recorded a higher receipts surplus compared with the year-back quarter, whereas secondary income registered a higher expenses surplus. The balances of trade in goods and primary income barely changed.

Read More »2019-06-13

13.06.2019 – The Producer and Import Price Index remained unchanged in May 2019 compared with the previous month. The index stood at 102.2 points (December 2015 = 100). Petroleum products in particular saw higher prices, while chemical and pharmaceutical products became cheaper. Compared with May 2018, the price level of the whole range of domestic and imported products fell by 0.8%.

Read More »2019-05-14

The Producer and Import Price Index remained unchanged in April 2019 compared with the previous month. The index stood at 102.2 points (December 2015 = 100). Higher prices were seen in particular for petrol and machinery, while diesel and heating oil became cheaper.

Read More »2019-04-25

The Swiss National Bank reports a profit of CHF 30.7 billion for the first quarter of 2019. The profit on foreign currency positions amounted to CHF 29.3 billion. A valuation gain of CHF 0.9 billion was recorded on gold holdings. The profit on Swiss franc positions was CHF 0.6 billion.

Read More »2019-04-18

Swiss foreign trade saw a mixed evolution during the first half of 2019. In seasonally adjusted terms, exports fell slightly, still remaining above the 57 billion franc mark. Imports, on the other hand, continued to rise (+1 , 0%) to reach a record level of 51.2 billion francs. The trade balance closes with a surplus of 6.2 billion francs.

Read More »2019-04-16

15.04.2019 – The Producer and Import Price Index increased in March 2019 by 0.3% compared with the previous month, reaching 102.2 points (December 2015 = 100). The rise is due in particular to higher prices for petroleum products. Compared with March 2018, the price level of the whole range of domestic and imported products fell by 0.2%.

Read More »2019-03-25

The current account surplus for 2018 was CHF 71 billion, CHF 26 billion more than in the previous year, an increase by over 50%.

Read More »2019-03-20

In February 2019, like the previous month, seasonally-adjusted exports increased (+ 2.3%), reaching a record level of 19.4 billion francs. On the other hand, imports fell by 1.2% in one month to 17.4 billion francs. The trade balance shows a surplus of 2.0 billion francs.

Read More »2019-03-14

The Producer and Import Price Index increased in February 2019 by 0.2% compared with the previous month, reaching 101.9 points (December 2015 = 100). The rise is due in particular to higher prices for petroleum products. Compared with February 2018, the price level of the whole range of domestic and imported products fell by 0.7%. These are some of the findings from the Federal Statistical Office (FSO).

Read More »2019-03-05

The SNB earned 2 billion on negative interest rates (Swiss franc positions below), but lost nearly 17 billion CHF on FX investments, of which 5 bn on bonds and 12 bn on stocks. Gold was nearly unchanged.

Read More »2019-02-28

2019-02-19

Swiss foreign trade started the year 2019 in a positive way. Seasonally adjusted exports rose by 1.1% to 18.9 billion francs and imports by 3.4% to 17.5 billion. The trade balance closed with a surplus of 1.4 billion francs.

Read More »2019-02-14

14.02.2019 – The Producer and Import Price Index fell in January 2019 by 0.7% compared with the previous month, reaching 101.7 points (December 2015 = 100). This decline is due in particular to lower prices for petroleum products. Compared with January 2018, the price level of the whole range of domestic and imported products fell by 0.5%.

Read More »2019-01-18

18.01.2019 – The Producer and Import Price Index fell in December 2018 by 0.6% compared with the previous month, reaching 102.5 points (December 2015 = 100). Compared with December 2017, the price level of the whole range of domestic and imported products rose by 0.6%. The average annualised inflation rate in 2018 was 2.4%.

Read More »2019-01-10

15 Billion Francs Losses in 2018. Given that the good years have finished: Will the SNB will ever make profits again? And compensate for the ever rising Swiss franc?

Read More »2018-12-21

Current Account Key figures: Current Account: Up 85% against Q3/2017 to 14.6 bn. CHF of which Goods Trade Balance: Up 16.6% against Q3/2017 to 10.5 bn. of which the Services Balance: Minus 5.6% to 5.0 bn. of which Investment Income: Up 74.4% to 7.6 bn. CHF. Financial account Net acquisition of financial assets The … Continue reading »

Read More »2018-12-20

In November 2018, exports confirmed their growth the previous month with a 1.8% increase, posting a new monthly peak. Imports, on the other hand, weakened by 1.2% and remain in a negative spiral. The trade balance closed with a surplus of 3.1 billion francs.

Read More »2018-12-13

The Swiss National Bank (SNB) is maintaining its expansio nary mo netary policy, thereby stabilising price developments and supporting economic activity. Interest on sight deposits at the SNB remains at –0.75% and the target range for the three-month Libor is unchanged at between –1.25% and –0.25%.

Read More »

The Producer and Import Price Index fell in November 2018 by 0.3% compared with the previous month, reaching 103.1 points (December 2015 = 100). This decline is due in particular to lower prices for pharmaceutical products. Compared with November 2017, the price level of the whole range of domestic and imported products rose by 1.4%.

Read More »2018-11-20

In October 2018, seasonally adjusted exports grew 6.0%, after their slightly negative evolution since June. They thus reach a level monthly record. Conversely, the decline in imports continued (-1.8%). The balance commercial loop with a surplus of 2.6 billion francs.

Read More »2018-11-13

The Producer and Import Price Index increased in October 2018 by 0.2% compared with the previous month, reaching 103.4 points (December 2015 = 100). The rise is due in particular to higher prices for petroleum products, petroleum and natural gas. Compared with October 2017, the price level of the whole range of domestic and imported products rose by 2.3%.

Read More »2018-10-31

The Swiss National Bank (SNB) reports a loss of CHF 7.8 billion for the first three quarters of 2018. A valuation loss of CHF 3.7 billion was recorded on gold holdings. The loss on foreign currency positions amounted to CHF 5.3 billion. The profit on Swiss franc positions was CHF 1.5 billion.

Read More »2018-10-18

After a year and a half of continued growth in Swiss foreign trade, exports in the third quarter of 2018 contracted by 2.9% compared with the previous quarter’s record. However, they remained above the 54 billion franc mark. Evolving at a high level, imports fell by 1.5% (-768 million francs). The trade balance closes with a surplus of 3.5 billion francs.

Read More »2018-10-15

The Producer and Import Price Index fell in September 2018 by 0.2% compared with the previous month, reaching 103.2 points (December 2015 = 100). The decline is due in particular to lower prices for scrap. Compared with September 2017, the price level of the whole range of domestic and imported products rose by 2.6%. These are some of the findings from the Federal Statistical Office (FSO).

Read More »2018-09-24

Key figures: Current Account: Up 27.0% against Q1/2018 to 22.1 bn. CHF, Goods Trade Balance: Up 4.8% against Q1/2018 to 15.2 bn., Services Balance: Minus 20.6% to 4.6 bn., Investment Income: Plus 107.7% to 10.7 bn. CHF.

Read More »2018-09-20

After the dynamism registered until May 2018, Swiss foreign trade has been stalled since. In August and after seasonal adjustment, exports stagnated at a high level and imports fell by 1.1%. The trade balance has a surplus of 1.4 billion francs.

Read More »2018-09-13

The Producer and Import Price Index remained unchanged in August 2018 compared with the previous month. The index stood at 103.4 points (December 2015 = 100). Prices were higher in particular for pharmaceutical and chemical products, while scrap became cheaper. Compared with August 2017, the price level of the whole range of domestic and imported products rose by 3.4%.

Read More »2018-08-22

After stagnating the previous month, both exports and imports fell in July 2018. In seasonally adjusted terms, they fell by 3.0 and 2.8%, respectively. The decline in the chemicals-pharmaceuticals sector weighed on the result in both directions of the traffic. The trade balance is closing with a surplus of 1.2 billion francs.

Read More »2018-08-14

The Producer and Import Price Index increased in July 2018 by 0.1% compared with the previous month, reaching 103.3 points (December 2015 = 100). The rise is due in particular to higher prices for watches, petroleum and natural gas. Compared with July 2017, the price level of the whole range of domestic and imported products rose by 3.6%.

Read More »2018-07-31

The Swiss National Bank (SNB) reports a profit of CHF 5.1 billion for the first half of 2018. A valuation loss of CHF 0.9 billion was recorded on gold holdings. The profit on foreign currency positions amounted to CHF 5.2 billion. The profit on Swiss franc positions was CHF 1.0 billion.

Read More »2018-07-20

The dynamism shown by exports since the beginning of 2017 continued in the second quarter of 2018. They are thus flying from record to record for the fifth quarter in a row. Imports, on the other hand, came to a standstill, at a high level, however, after posting strong growth in previous quarters. The trade balance closes on a surplus of 4.6 billion francs.

Read More »2018-07-13

The Producer and Import Price Index increased in June 2018 by 0.2% compared with the previous month, reaching 103.2 points (December 2015 = 100). The rise is due in particular to higher prices for petroleum products and timber products. Compared with June 2017, the price level of the whole range of domestic and imported products rose by 3.5%.

Read More »2018-06-25

The current account surplus amounted to CHF 18 billion in the first quarter of 2018, an increase of CHF 5 billion over the same quarter of 2017. This rise was attributable to the higher receipts surplus on trading in non-monetary gold, which is recorded under trade in goods. In the case of services as well as primary and secondary income, the balances remained stable.

Read More »2018-06-21

After stagnating in previous months, exports rose in May 2018. Seasonally adjusted exports rose 0.9% in one month. Imports were more dynamic, at + 3.8%. Chemistry-pharma and the vehicle sector generated 90% of growth in both traffic directions. The trade balance closed with a surplus of 2.3 billion francs.

Read More »2018-06-13

The Producer and Import Price Index increased in May 2018 by 0.2% compared with the previous month, reaching 103.0 points (December 2015 = 100). The rise is due in particular to higher prices for petroleum products. Compared with May 2017, the price level of the whole range of domestic and imported products rose by 3.2%. These are some of the findings from the Federal Statistical Office (FSO).

Read More »2018-05-29

In recent months, both exports and Swiss imports have been apathetic. On April 1, 2018, and after seasonal adjustment, they respectively stagnated and fell by 3.4%. The chemistry-pharma has sealed the result in both directions of the traffic. The trade balance closed with a surplus of 2.8 billion francs.

Read More »2018-05-24

2018-05-18

2018-05-15

The Producer and Import Price Index increased in April 2018 by 0.4% compared with the previous month, reaching 102.8 points (December 2015 = 100). The rise is due in particular to higher prices for petroleum products and machinery. Compared with April 2017, the price level of the whole range of domestic and imported products rose by 2.7%.

Read More »2018-04-27

The Swiss National Bank (SNB) reports a loss of CHF 6.8 billion for the first quarter of 2018. A valuation loss of CHF 0.2 billion was recorded on gold holdings. The SNB’s financial result depends largely on developments in the gold, foreign exchange and capital markets. Strong fluctuations are therefore to be expected, and only provisional conclusions are possible as regards the annual result.

Read More »2018-04-24

In the first quarter of 2018 and on a seasonally adjusted basis, foreign trade confirmed the positive trend of previous quarters. Both traffic directions have also reached record levels. Exports increased by 0.2% and imports by 4.1%. The divergent evolution of inflows and outflows has led to the smallest trade surplus in four and a half years.

Read More »2018-04-16

The Producer and Import Price Index fell in March 2018 by 0.2% compared with the previous month, reaching 102.3 points (December 2015 = 100). This decline was due in particular to lower prices for petroleum products and pharmaceutical preparations. Compared with March 2017, the price level of the whole range of domestic and imported products rose by 2.0%. These are some of the findings from the Federal Statistical Office (FSO).

Read More »2018-03-27

Key figures: Current Account: -9.6% against Q4/2016 to 19,679 bn. CHF, Record High Trade Surplus in Goods: +24.4% to 17,279 bn., Services Surplus : -4.0% to 4,820 bn., but Investment Income: down 42.7% to 5,877 bn.

Read More »2018-03-23

2018-03-20

In February 2018, exports increased by 1.8%, confirming their positive trend. After their January record, imports fell back (-9.8%). However, they continued to grow at a high level, at 16.1 billion francs. At the entrance, the flagship markets Europe and North America led the result.

Read More »2018-03-15

The Producer and Import Price Index rose in February 2018 by 0.3% compared with the previous month, reaching 102.6 points (December 2015=100). The rise is due in particular to higher prices for chemical and pharmaceutical products. Compared with February 2017, the price level of the whole range of domestic and imported products rose by 2.3%. These are some of the findings from the Federal Statistical Office (FSO).

Read More »2018-03-06

The Swiss National Bank (SNB) reports a profit of CHF 54.4 billion for the year 2017 (2016: CHF 24.5 billion). The profit on foreign currency positions amounted to CHF 49.7 billion. A valuation gain of CHF 3.1 billion was recorded on gold holdings. The profit on Swiss franc positions was CHF 2.0 billion.

Read More »2018-02-28

2018-02-20

Although exports fell in January 2018 from the December peak, their trend remains upward. Imports, for their part, began the year with fanfare to sign a record result. In both traffic directions, chemicals and pharmaceuticals made rain and shine.

Read More »2018-02-13

Neuchâtel, 13 February 2018 (FSO) – The Producer and Import Price Index rose in January 2018 by 0.3% compared with the previous month, reaching 102.2 points (December 2015=100). The rise is due in particular to higher prices for petroleum products, electricity and gas as well as metals and metal products. Compared with January 2017, the price level of the whole range of domestic and imported products rose by 1.8%. These are some of the findings from the Federal Statistical Office (FSO).

Read More »2018-01-30

Last year, Swiss foreign trade accelerated yet again relative to 2016: exports rose by 4.7% to reach a new record high. Imports grew by 6.9%, posting their strongest growth rate since 2010. Aside from the improved economic situation worldwide, the weakening of the Swiss franc and price trends played a decisive role in both directions of trade. With a surplus of CHF 34.8 billion, the balance of trade closed the year 6% (or CHF 2.1bn) lower than the previous year.

Read More »2018-01-19

The Producer and Import Price Index rose in December 2017 by 0.2% compared with the previous month, reaching 101.9 points (December 2015=100). Compared with December 2016, the price level of the whole range of domestic and imported products rose by 1.8%. The average annualised inflation rate in 2017 was 0.9%. These are some of the findings from the Federal Statistical Office (FSO).

Read More »2017-12-30

The Swiss current account surplus went down by 15% against the same quarter in 2016. In the third quarter of 2015. The current account surplus was still at 22 bn. CHF.

It seems to be a change in the usual movement that sees a higher Q3 surplus compared to the other quarters.

2017-12-21

Swiss foreign trade proved dynamic in November 2017. After correction of working days, exports grew by 9.5% and imports even 16.4% year on year, both boosted by rising prices. In real terms, they increased by 4.4 and 6.8%, respectively. The balance commercial loop with a surplus of 2.7 billion francs.

Read More »2017-12-14

The Producer and Import Price Index rose in November 2017 by 0.6% compared with the previous month, reaching 101.6 points (base December 2015 = 100). The rise is due in particular to higher prices for petroleum products, chemical and pharmaceutical products and scrap. Compared with November 2016, the price level of the whole range of domestic and imported products rose by 1.8%.

Read More »2017-11-30

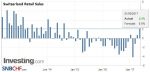

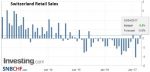

Turnover in the retail sector fell by 2.7% in nominal terms in October 2017 compared with the previous year. Seasonally adjusted, nominal turnover fell by 1.6% compared with the previous month. These are provisional findings from the Federal Statistical Office (FSO).

Read More »

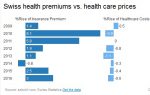

The health insurance premiums index (CIPI) recorded a growth of 3.8 percent over the previous year for the 2017 premium year. The KVPI thus achieved an index level of 185.3 points (base 1999 = 100). The impact of premium development on the growth of disposable income can be estimated using the CIPI. According to the KVPI model calculation by the Federal Statistical Office (FSO), the increase in premiums reduces the growth in average disposable income in 2017 by 0.3 percentage points.

Read More »2017-11-21

In October 2017, Swiss foreign trade continued its advance. Adjusted for working days, exports grew by 5% against 7% for imports. Growth, however, weakened slightly compared to previous months. The trade balance is closing with a surplus of 2.4 billion francs.

Read More »2017-11-14

The Producer and Import Price Index rose in October 2017 by 0.5% compared with the previous month, reaching 101.0 points (base December 2015 = 100). The rise is due in particular to higher prices for machinery, electrical equipment and metal products. Compared with October 2016, the price level of the whole range of domestic and imported products rose by 1.2%.

Read More »2017-11-02

Turnover in the retail sector remained stable in nominal terms in September 2017 compared with the previous year. Seasonally adjusted, nominal turnover rose by 0.8% compared with the previous month. These are provisional findings from the Federal Statistical Office (FSO).

Read More »2017-10-31

The Swiss National Bank (SNB) reports a profit of CHF 33.7 billion for the first three quarters of 2017. But in 2017, the picture is changed. Assuming a “biblical” cycle of seven good years and seven bad years, the SNB could now increase profits every year – thanks to a weaker franc and the seven good years.

Read More »2017-10-19

With adjusted working days, exports grew by 2.5% and imports by 7.4% in the third quarter of 2017. Trade was thus consolidated at a high level. The balance of the trade balance contracted from 10.3 to 8.5 billion francs.

Read More »2017-10-02

Turnover in the retail sector fell by 0.6% in nominal terms in August 2017 compared with the previous year. Seasonally adjusted, nominal turnover fell by 0.3% compared with the previous month. These are provisional findings from the Federal Statistical Office (FSO).

Read More »2017-09-26

Key figures, Current Account: -3.6% against Q2/2016 to 18,748 bn. CHF, Trade Balance: +6.5% to 15,550 bn, Services Balance: -12.8% to 4,087 bn, Investment Income: -22.9% to 7,369 bn.

Read More »2017-09-21

In August 2017, Swiss foreign trade grew stronger both at entry and exit. With growth of 9.9%, imports were much more dynamic than exports (+ 3.9%). The balance of trade closed with a surplus of 2.2 billion francs.

Read More »2017-09-14

The SNB projects that she will reach her inflation target, shortly under 2% in the medium term, i.e. in 2019/2020. One reason might be the weakening of the Swiss Franc. But she does not prepare for a normalization of her policy: From the history we know that – once the franc is weakening – inflation may rise very quickly.

Read More »2017-09-10

The euro rose close to CHF 1.15 with the ECB meeting this week. Finally traders realized that the ECB committed not to hike rates for a very long time. The ECB will review and take a first decision on the bond purchasing program this autumn. However, this program will come to an end only when the inflation target of 2% becomes in reach.

Read More »2017-09-04

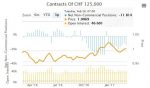

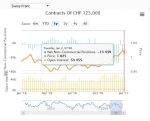

The net speculative CHF position has fallen from 2K short to 1.8K contracts short (against USD). Speculators did not make any significant adjustment to gross positions, which we define as 10k or more contracts in the currency futures, during the CFTC reporting week ending August 29.

Read More »2017-09-03

For us, the sudden euro rise from 1.08 to 1.14 is an illusion, the euro will fall sooner or later again. Macron will not help the French economy and low core inflation will prevent that the ECB ends her bond buying program.

Read More »2017-09-01

Turnover in the retail sector fell by 0.8% in nominal terms in July 2017 compared with the previous year. Seasonally adjusted, nominal turnover fell by 1.1% compared with the previous month. These are provisional findings from the Federal Statistical Office (FSO).

Read More »2017-08-28

The net speculative CHF position has risen from 1.2K short to 2K contracts short (against USD). Speculators continued to amass a significant short sterling position in the futures market. In the CFTC reporting week ending August 22, speculators added 11.7k contracts to the gross short position, lifting it to 107.4k contracts.

Read More »2017-08-26

The broad technical condition of the dollar deteriorated materially before the weekend. The dollar had some gains versus the franc during the last month, but it lost all during the last days.The EURCHF continues with a 2.5% win for the last month.

Read More »2017-08-22

In July 2017, after adjusting for working days, exports grew by 4.5%, which were less dynamic than the previous two months. Imports rose red (-0.5%). The trade balance loops with a surplus of 3.6 billion francs.

Read More »2017-08-21

The net speculative CHF position has fallen from -1.4K short to -1.2K contracts short (against USD). Speculators made several significant position adjustment in the CFTC reporting week ending August 15, that included an escalation of aggressive rhetoric by the US and North Korea.

Read More »2017-08-20

The euro has lost some momentum, Draghi does not want to talk about an early end of his bond buying programming. Confirmed by economic data, 1.2% core inflation compared to a long-term inflation target of 2%. Consequently the Swiss appreciated during the week.

Read More »2017-08-15

The Producer and Import Price Index remained unchanged in July 2017 compared with the previous month at 99.7 points (base December 2015 = 100). Petroleum products in particular became cheaper. Prices were higher for scrap, computers and metal products. Compared with July 2016, the price level of the whole range of domestic and imported products fell by 0.1%.

Read More »2017-08-14

Despite the tensions between Donald Trump and North Korea’s Kim Jong-un, the EUR/CHF only depreciated to 1.13. In the last week, the SNB did not have to intervene. This proves that investors have not taken the tensions seriously.

Read More »2017-08-07

The net speculative CHF position has risen from -1.5K short to 1.4K contracts long (against USD). In the CFTC reporting week ending August 1, speculators in the futures market continued to build long exposure in the dollar-bloc currencies. In the three sessions after the reporting period closed, the dollar-bloc currencies have traded heavily.

Read More »2017-08-06

The Swiss Franc entered the second week of stronger losses. While the euro gained 4% last week, the dollar appreciated against the Swiss Franc 2% during this week.

Read More »2017-08-02

Turnover in the retail sector rose by 1.1% in nominal terms in June 2017 compared with the previous year. Seasonally adjusted, nominal turnover rose by 0.5% compared with the previous month. Real turnover in the retail sector also adjusted for sales days and holidays rose by 1.5% in June 2017 compared with the previous year.

Read More »2017-07-31

The Swiss National Bank (SNB) reports a profit of CHF 1.2 billion for the first half of 2017. A valuation gain of CHF 0.3 billion was recorded on gold holdings. The profit on foreign currency positions amounted to CHF 0.1 billion and the profit on Swiss franc positions stood at CHF 0.9 billion. The SNB’s financial result depends largely on developments in the gold, foreign exchange and capital markets.

Read More »

The net speculative CHF position has risen from -3.7K short to -1.5K contracts short (against USD). Speculators were active in the currency futures in the CFTC reporting week ending July 25. In particular, speculative sentiment continues to be drawn to the Canadian and Australian dollars.

Read More »2017-07-30

The Swiss franc was the only major foreign currency that fell against the dollar last week. The 2.6% decline was the largest in two years.

Read More »2017-07-24

The net speculative CHF position has changed from -0.2K long to 3.7K contracts short (against USD). Since the beginning of May the Canadian dollar has been the strongest of the major currencies. However, until the most recent CFTC reporting week ending July 18, speculators in the futures market were net short.

Read More »2017-07-23

Both Swiss Franc and Euro were moving upwards against the dollar. So CHF gained 3% versus the dollar in the last month. CHF losses against the euro are smaller, around 1.3%.

Read More »2017-07-20

In the first half of 2017, both exports (+ 4.4%) and imports (+ 4.8%) were dynamic. While the former scored a record result, the latter scored a higher in eight years. In both directions of traffic, chemicals and pharmaceuticals contributed decisively to growth. The trade balance loops with a surplus of 19 billion francs.

Read More »2017-07-17

Hawkish comments by Mario Draghi boosted the EUR against both USD and CHF. It also reduced the need for SNB interventions. The question is how long Draghi will remain hawkish, especially next winter, when headline inflation in the euro zone may fall under 1%.

Read More »

The net long CHF position has risen from 0.1K short to 0.2K contracts short (against USD). Speculators are long EUR against both USD and CHF. We wonder how long this will be the case, given that we expect Euro zone inflation to fall under 1% from December 2017 onward.

Read More »2017-07-16

The Euro remained the strongest among EUR, CHF and USD during the last month.

The Swiss lost against EUR 1.5%, while it gained versus the dollar 0.75%.

2017-07-13

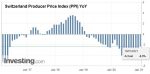

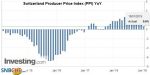

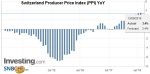

The Producer Price Index (PPI) or officially named “Producer and Import Price Index” describes the changes in prices for producers and importers. For us it is interesting because it is used in the formula for the Real Effective Exchange Rate. When producers and importers profit on lower price changes when compared to other countries, then the Swiss Franc reduces its overvaluation.

Read More »2017-07-10

The net short CHF position has fallen from 4.7k short to 0.1k contracts short (against USD). Speculators in the futures market made several significant position adjustments in the CFTC reporting week ending July 4, despite it being a holiday-shortened week.

Read More »2017-07-09

The ECB appears to be preparing investors for a further adjustment of its risk assessment and a reduction of its asset purchases as they are extended into next year.

This assessment has marked a new phase of an appreciating EUR/CHF rate. It followed the previous phase, the one with and after the French elections.

2017-07-04

Turnover in the retail sector fell by 0.3% in nominal terms in May 2017 compared with the previous year. Seasonally adjusted, nominal turnover rose by 0.3% compared with the previous month. Real turnover in the retail sector also adjusted for sales days and holidays fell by 0.3% in May 2017 compared with the previous year. Real growth takes inflation into consideration. Compared with the previous month, real, seasonally adjusted retail trade turnover registered an increase of 0.3%.

Read More »2017-07-03

The net short CHF position has risen from 3k short to 4.7k contracts short (against USD). Speculators bought back previously sold Canadian dollar and Mexican peso futures positions in dramatic fashion in the CFTC reporting week ending June 27.

Read More »

A virus has spread across the markets as the first half drew to a close. Many investors have become giddy. The low vol environment was punctuated by ideas that peak in monetary accommodation is past and that the gradual process of normalization is beginning.

Read More »2017-06-26

Key Figures, Current Account: +39% against Q1/2016, now +11.1 bn. CHF, Trade Balance: +78% to 10.5 bn, Services Balance: +21% to 5.5 bn, Investment Income: -50% to +2.9 bn.

Read More »

The net short CHF position has fallen from 14.5 short to 3K contracts short (against USD). The expiration of the June contracts and the roll into September positions appears to have boosted activity in the currency futures, and may obscure the signaling effect. Of the 16 gross positions we track, speculators add to exposure in all but four positions. There speculators covered gross short Swiss franc, Canadian, Australian, and New Zealand dollar positions.

Read More »2017-06-25

Over the last month, the Swiss franc outpaced both EUR and USD. But the change is only little, the EUR fell by 0.60% and the dollar by 0.40%. The main reason for the stronger CHF is the fading enthusiasm after Macron’s victory in the French elections and hence a weaker euro. Consequently SNB interventions are rising again.

Read More »2017-06-22

In May 2017, Swiss foreign trade was dynamic. Adjusted for working days, exports increased by 7.5% and imports by 8.7%. Chemicals and pharma boosted growth in both directions. The balance of trade closed with an impressive surplus of 3.4 billion francs.

Read More »2017-06-19

The pro-European politician Macron has won the French elections. His success moved the EUR/CHF up to 1.0980, mostly caused by FX speculators. But “serious” investors (not FX speculators) did not follow the political event, but focus on monetary policy. A ECB rate hike is very, very far, see why….

Read More »

The net short CHF position has fallen from 16.5 short to 14.5K contracts short (against USD). We wonder how long this will be the case, given that we expect Euro zone inflation to fall under 1% from December 2017 onward.

Read More »

Swiss Franc vs USD and EUR Rarely in the foreign exchange market is there a V-shaped extreme. Most of the time, the high or low is a process that is carved over time. Although the explanation of the dollar’s weakness here in H1 vary, we continue to believe that the longer-term cyclical rally, the third since … Continue reading »

Read More »2017-06-15

The Producer Price Index (PPI) or officially named “Producer and Import Price Index” describes the changes in prices for producers and importers. For us it is interesting because it is used in the formula for the Real Effective Exchange Rate. When producers and importers profit on lower price changes when compared to other countries, then the Swiss Franc reduces its overvaluation.

Read More »2017-06-12

The net short CHF position has fallen from 18.5 short to 16.5K contracts short (against USD). But the major movement was that speculators are net long the euro now and not the dollar any more. This implies that they are also long Euro against CHF. In the CFTC reporting week that covered the US employment data and the run-up to Super Thursday that featured an ECB meeting, former FBI Director Comey’s testimony before the Senate Intelligence Committee, the UK election, speculators mostly reduced exposure in the foreign exchange futures market.

Read More »2017-06-11

The US Dollar has lost 4% against the franc since the beginning of May, while the euro is down only 1%. Most important events in this week were the ECB meeting and the UK elections. The inability of the Tory Party to secure a parliamentary majority spurred a sharp decline in sterling.

Read More »2017-06-05

The net short CHF position has fallen from 19.8 short to 18.5K contracts short (against USD). But the major movement was that speculators are net long the euro now and not the dollar any more. This implies that they are also long Euro against CHF. Speculators in the future market made mostly minor adjustment in the gross positioning in the currencies.

Read More »2017-06-04

While the Euro traded in the range between 1.08 and 1.09, the dollar declined by nearly 3%. The technical indicators warn that the US dollar is stretched, but the combination of disappointing auto sales and jobs report may deny it the interest rate support needed to facilitate a resumption of the bull market.

Read More »2017-06-01

Switzerland’s real gross domestic product (GDP) grew by 0.3 % in the first quarter of 2017*. Private consumption growth expanded only slightly, while government consumption rose moderately. Following the previous quarter’s fall, investment in construction and equipment increased.

Read More »

Real turnover in the retail sector also adjusted for sales days and holidays fell by 1.2% in April 2017 compared with the previous year. Real growth takes inflation into consideration. Compared with the previous month, real, seasonally adjusted retail trade turnover registered a decline of 2.4%.

Read More »2017-05-29

The net short CHF position has fallen from 21.1 short to 19.8K contracts short (against USD). But the major movement was that speculators are net long the euro now and not the dollar any more. This implies that they are also long Euro against CHF. In the CFTC reporting week ending May 23 speculators in the futures market continued to largely position themselves for further dollar weakness.

Read More »

The Swiss Franc recovered a lot of the losses that came with the French elections. That political event was mostly driven by speculators that will close their positions. We expected the EUR to trade around 1.07 to 1.0750 CHF in some time.

Read More »2017-05-23

In April 2017, adjusted exports of working days shrank as imports strengthened by 2.3%. Changes in sales were marked by the reluctance of the chemical and pharmaceutical sector. The trade balance has closed with the smallest surplus in the last two years.

Read More »2017-05-22

The net short CHF position has risen from 15.2 short to 21.1K contracts short (against USD). But the major movement was that speculators are net long the euro now and not the dollar any more. This implies that they are also long Euro against CHF. In the Commitment of Traders reporting week ending May 16, speculators in the futures market made three significant adjustments in the currency futures.

Read More »2017-05-21

The Swiss Franc recovered a lot of the losses that came with the French elections. That political event was mostly driven by speculators that will close their positions. We expected the EUR to trade around 1.07 to 1.0750 CHF in some time.

Read More »2017-05-16

The pro-European politician Macron has won the French elections. His success moved the EUR/CHF up to 1.0980, mostly caused by FX speculators. But “serious” investors (not FX speculators) did not follow the political event, but focus on monetary policy. A ECB rate hike is very, very far, see why….

Read More »2017-05-15

The Producer and Import Price Index fell in April 2017 by 0.2% compared with the previous month, reaching 100.1 points (base December 2015 = 100). This decline is due in particular to lower prices for petroleum products and machinery. Compared with April 2016, the price level of the whole range of domestic and imported products rose by 0.8%.

Read More »

The net short CHF position has fallen from 17.7 short to 15,2K contracts short (against USD).

But the major movement was that speculators are net long the euro now and not the dollar any more. This implies that they are also long Euro against CHF.

2017-05-13

The euro rose up to 1.0980. How long this momentum will last is still the question, given that it is driven by this political event and sustained by SNB interventions.

Read More »2017-05-10

The centre-left politician Macron has won the French elections. His success moved the EUR/CHF up to 1.0960, mostly caused by FX speculators. But serious investors – i.e. not FX speculators – did not follow the political event. The SNB had to intervene for 1.6 bn francs.

Read More »2017-05-08

The net short CHF position has risen to 17K contracts (against USD). It was feast or famine in the adjustment of speculative positions in the currency futures market during the CFTC reporting period ending May 2. Speculators either made large adjustments or very small adjustments, and little in between.

Read More »2017-05-07

The Swiss Franc index gained 1.5% in the last month, the biggest part of it is from the last week. The trade-weighted indices the Fed tracks are updated monthly. The Bank of England calculates the effective exchange rate on a daily basis. It has not fallen since April 24.

Read More »2017-05-03

The centre-left politician Macron has won the French elections. He is a politician that – similar to Hollande four years ago – promises economic improvements, move investment, more jobs. Mostly probably he will fail similar to Hollande. His success moved the EUR/CHF up to 1.0865, mostly caused by FX speculators, but the SNB had to intervene.

Read More »2017-05-01

The net short CHF position has risen to 17K contracts (against USD). The striking development among speculators in the futures market is the reversal of the record gross (and net) short Treasury note position two months ago.

Read More »

Turnover in the retail sector rose by 1.8% in nominal terms in March 2017 compared with the previous year. This is the sharpest increase since June 2014. Seasonally adjusted, nominal turnover rose by 0.6% compared with the previous month. These are provisional findings from the Federal Statistical Office (FSO).

Read More »

Often the US dollar, as the numeraire, seems to be the main actor in the foreign exchange market. Other times, the dollar appears to be at the fulcrum between European currencies on one hand, and the dollar-bloc currencies on the other hand. Another way expressing this is whether there is a dollar-move underway or is it really more about the crosses.

Read More »2017-04-27

The SNB reports a profit of 7.9 bn CHF, of which 2.2 bn come from the gold holdings. Given that the bank has introduced a “minimum euro rate” around 1.06-1.07, this is not very difficult. It comes at the price of continuing interventions.

Read More »

Swiss exports are moving more and more toward higher value sectors: away from watches, jewelry and manufacturing towards chemicals and pharmaceuticals. With currency interventions, the SNB is trying to keep sectors alive, that would not survive without interventions.

Read More »2017-04-25