George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

The yen overshot during and after the financial crisis. The USD/JPY fell from 120 in 2008 to lowest levels of 74, by 62%, clearly into overvalued JPY territory, but recently it has risen to 102 again. What are the reasons?

UPDATE November 2013:

The weak performance of the Japanese currency is not explained only by the current risk-off environment or by Abenomics. For us, the Japanese oil trade deficit is paramount.

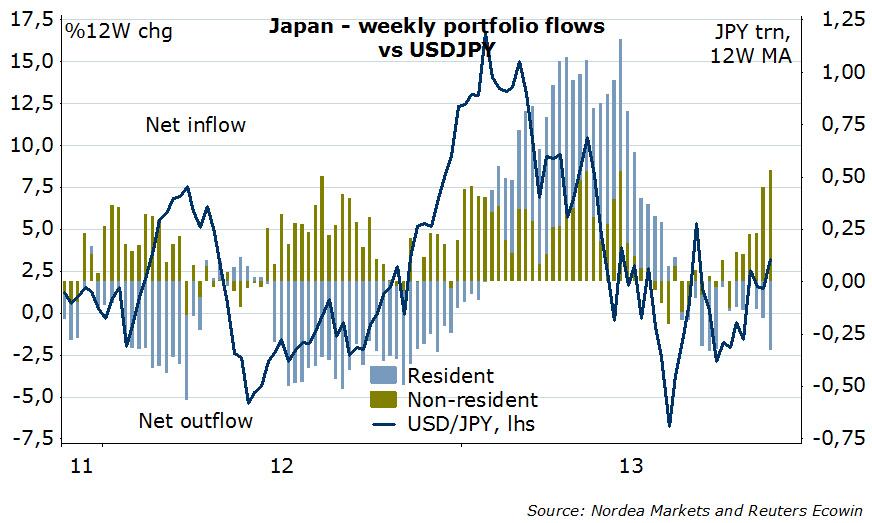

Currently foreign investors drive the Nikkei higher, while some residents leave Japan. In total portfolio investments are rather inflows.

The Yen’s overshooting in the financial crisis

The yen overshot during and after the financial crisis. The USD/JPY fell from 120 in 2008 to lowest levels of 74, by 62%.

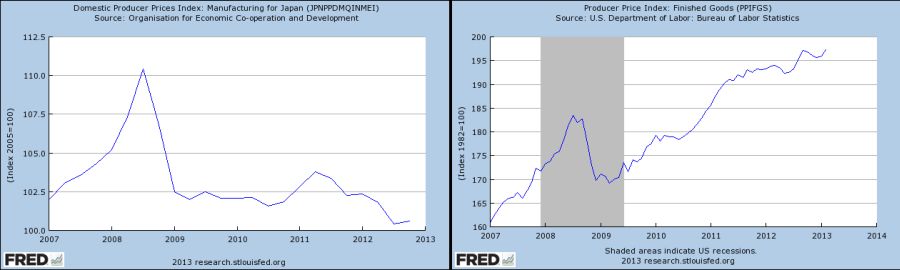

For the purchasing power parity, usually the producer price index is used. In terms of producer prices the yen should have appreciated by 22% = 197/160 between January 2007 and March 2013. The US producer price index rose from 160 to 197, American production is 22% more expensive. Thanks to deflation or low inflation, the Japanese price index, however, remained nearly unchanged.

By March 2013, this tendency was reversed and the yen came back to “real mean reversion”: USD/JPY went from 120 in January 2007 to 96 in March 2013 and fell by exactly 25%.

Consequently IMF’s Schiff said in March 2013:

IMF Schiff “In our previous assessment in the External Sector Report, which was published last summer, our various methodologies had shown moderate overvaluation of the yen,” Jerald Schiff, deputy director of the IMF’s Asia and Pacific Department, said through email exchanges with MNI. “Since then, the currency has depreciated by over 15% to 20% in trade weighted terms, bringing the yen back to its long-run average,” said Schiff. “At least a temporary weakening of the yen could be expected to result from a successful reflation,” he said, referring to Abe’s policy to stimulate the economy by boosting money supply. But he warned that such weakness without reform would create issues. In June last year, the IMF said in its 2012 Article IV Consultation Discussion with Japan that “the yen is moderately overvalued from a medium-term perspective.“

The yen appreciates typically in the months between January and the beginning of May, when the effect of weaker oil prices in Q4 and stronger US demand in Q1 lead to the “Sell in May, Come Back in October effect.”

Between October 2012 and March 2013 six factors let to a very strong risk-on momentum against the yen:

- The Fed’s “unlimited” quantitative easing helped to increase house prices.

- The perceived end of the euro crisis with the promise of unlimited interventions by the ECB

- A slowing in the emerging markets combined with rows between China and Japan

- Weaker oil prices in the US: gas prices rose only modestly in February and March 2013 when compared to normal seasonality

- Outflows of Foreign Direct Investments from China and other emerging markets sustained investments in US dollar.

- Verbal intervention by the Japanese officials additionally suppressed the currency claiming that they wanted to end Japanese deflation. With the upcoming higher VAT, currency depreciation, positive consumer and business climate, the CPI could effectively rise to 2%.

The Japanese oil trade deficit

The new oil trade deficit, however, is paramount. Since summer 2012 the last reactors

On May 5, 2012, the reactor Number 3 was shut down for regular inspections, meaning of all 50 reactors in Japan, none were producing energy, which has only occurred once before, between 30 April and 4 May 1970 (when there were only 22? reactors available), since the start of Japanese commercial nuclear power generation in 1966. After the nuclear disaster in Fukushima in March 2011, Japanese public opinion shifted away from nuclear power generation.The shutdown of the last active nuclear powerplant caused a demonstration of thousands in Tokyo. These people celebrated a “nuclear free” Japan, according to them Japan can do perfectly without. from Wikipedia

source