George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Via Zerohedge

The conflict between labor and capital is a long and illustrious one, and one in which ideology and politics have played a far greater role than simple economics and math.

And while labor enjoyed a brief period of growth in the the past 100 years first due to the anti-trust and anti-monopoly, and pro-union laws and regulations taking place in the early 20th century US, and subsequently due to the era of “Great Moderation”-driven “trickling down” abnormal growth in the developed world, it is precisely the unwind of this latest period of prosperity, loosely known as “The New Normal”, and in which economic growth will persist at well sub-optimal (<2%) rates for the foreseeable future, that is pushing the precarious balance between labor and capital costs – in their purest economic sense, and stripped of all ethics and ideology – to a point in which labor will likely find itself at a persistent disadvantage, leading to the same social upheaval that ushered in pure Marxist ideology in the late 19th century.

Only this time there will be a peculiar twist, because while in relative terms labor costs as a percentage of all operating expenses are declining around the world, when accounting for benefits, and entitlement funding, labor costs are rising in absolute terms if at uneven rates (a particularly touchy topic in the Eurozone where lack of labor competitiveness for the periphery is probably the single thorniest issue for the European Disunion) and are now at record highs.

Which sets the stage for what may probably be the biggest push-pull tension of the 21st century for the simple worker: declining relative wages, which however are increasing in absolute terms when factoring in the self-funded components paid into an insolvent welfare system.

But the rub comes when one considers the biggest disequilibrium creator of all: central bank predicated cost of capital “planning”, whereby Fed policies may be the most insidious and stealth destroyer of all of labor’s hard won gains over the past century.

First, observe the declining labor costs as a percentage of total corporate operating expenses…

Which however is cold comfort to firms which report earnings on a nominal basis, and for which the absolute increase in blended all in labor compensation is now the highest in history…

… a variable cost “discontinuity” driven by a key fixed cost: social insurance expenditures and labor-related taxes. In other words workers are increasingly forced to prefund their own “entitlements”…

… Which finally means that increasingly the simplest solution will likely be the correct one: places in which the cost of labor is higher than that of capital will increasingly shed labor until there is once again an equilibrium between labor and capital. An approximate breakdown between these two primary drivers is shown in the chart below.

Before we present some of the startling conclusions from the above, here are some thoughts on the basis of labor costs as we enter the New Normal from Goldman Sachs:

The ability to cut these depends very much on the nature of the business (labour-intensive versus capital-intensive), the scale and balance sheet strength of the company, the flexibility to move operations, domicile regulations and political pressures, and the clarity of management foresight. One option CEOs have is to become more efficient through automation, i.e., substituting labour with capital. We expect to see a lot more of this type of restructuring in the developing economies, as real wages rise and the difference in the relative cost of capital versus developed economies shrinks.

The balance between labour and capital reflects a tension between maintaining flexibility and achieving efficiency. Remaining labour-intensive can allow companies to react in a more agile manner to structural shifts or prolonged cyclical softness, giving them the option to increase or decrease headcount (albeit at a price) or re-train personnel in the case of obsolescence, which is particularly important in fast-moving industries. On the other hand, automation increases production efficiency, speed and quality, often at a lower operational cost, at the expense of having a larger chunk of capital tied to fixed assets.

Over the last decade, cheap labour was perhaps the primary motivation for location-based restructuring. But looking forward, greater EM competition, IP risks, regulation, energy cost disparity, supply chain complexity and the need to be closer to the end consumer should also force companies to reconsider where they are based. But we shouldn’t forget that prescribing change is not the same as achieving it, especially for companies that employ a large number of people in domestic Europe. These companies are likely to encounter greater political pressure, while the fear of losing skills also make companies reluctant to cut their headcount. Capital intensity could also be an exit barrier; e.g., its difficult for physical retailers to exit real estate quickly. And finally, there is the zero sum game argument, or at best a fleeting competitive advantage, which can be observed in the very short periods of returns leadership in many industries.

And while superficially all of the above is correct, the one increasingly dominant factor is that of pure cost of capital, from a simple ROE basis, when corporate executives make a decision whether to invest in wages and workers or efficiency improvements, i.e., capital. It is here that one needs to appreciate that cost of capital is increasingly synonymous with simple cost of borrowing as shown on the last chart above.

What needs no explanation is that in “the New Normal”, the cost of borrowing is declining progressively and in more and more parts of the world is approaching zero: a standard byproduct of ZIRP, or a paradigm in which virtually all credit risk (and soon – equity risk as well as the Japan Model is adopted by all) is borne by the money printers themselves, or in the case of the US: the Federal Reserve.

And with cost of debt and thus capital virtually non-existent, the decision of where to allocated increasingly scarcer cash flows will become a very simple one, and the outcome will be one which will infuriate more and more workers around the world.

What does all of the above mean practically? Two things:

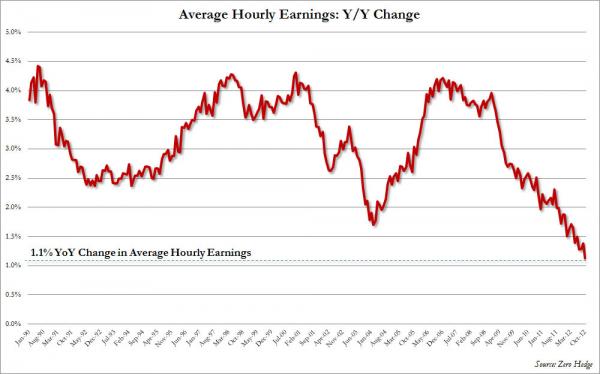

- The ever more insolvent “welfare state” world is seeing increasingly more of the fixed cost contribution to pre-funding entitlements fall on the shoulders of the same workers whose wages are increasingly declining on a relative basis (best seen when looking at the year over year change in average hourly earnings, which just posted the smallest nominal rise on record.

The problem with this is that laborer intuitively realize that the “welfare state” model no longer works, and is broken: there are simply too many unfunded liabilities that current and future generations of workers have to fund concurrently for there to be anything left over in the sinking fund to prepay their own pension, retirement and welfare benefits. As a result more and more workers will demand instant gratification in the form of upfront cash now, and will no longer accept the excuse that their employers are making up the difference in declining earnings by funding future welfare costs, as extracted in turn by ever more insolvent governments. - The Fed, in its attempts to rekindle the credit bubble with its ZIRP policy, which will last at least through the end of 2015 (but likely, in perpetuity, or at least until hyperinflation force Bernanke to prove if his bluff that he can end any inflationary episode in 15 minutes or less), has stumbled upon yet another unintended consequence- it is making the balance between labor and capital progressively more distressing for current workers, as the Fed is effectively funding – thanks to no cost borrowings – corporate improvements in productivity and capital replacement, which in turn make layoffs and wage cuts the default decision by most corporate treasurers and CFOs.

These two bullet points will garner increasingly more attention in the coming months as more and more people are laid off, if for no reason of the underlying economy which may or may not be getting stronger (or certainly weaker), but simply as as the cost of corporate debt, especially for Investment Grade quality corporations, plummets to zero when used to fund capital improvements, and thus increased profitability when coupled with labor “efficiency.”

Because what few appreciate is that Marxism in the New Normal will not be a carbon copy of that from 150 years ago: instead the primary driver paradoxically of the next labor movement will be in response to the destructive policies (at least for workers, if not for corporate profitability and shareholders) of the central planners. That, and the fact that the entire Welfare state ponzi, now pervasive to all developed world countries, is on its last breath: a conclusion which even the simple workers of the world can appreciate.

Or not: because as the recent example of the outright Hostess liquidation demonstrated, when negotiating labor equivalency outcomes from a Game Theoretical perspective in the New Normal, labor no longer has the upper hand, especially when the opportunity cost of wiping out future (fully or partially) prepaid entitlement benefits are to be considered – a lesson which the Twinkie baking union learned the very hard way.

It also means that as more instances of labor unions vs corporations come to the fore in bankruptcy court, and as labor losses mount, it will once again be the evil corporations that are scapegoated by virtually everyone involved.

Yet the truth is far more complicated, and as the above shows, while workers of the world may, indeed, soon be uniting once more, don’t forget to reserve some of that righteous indignation not only for executive corner office dwellers, but for those in charge of government and of various central banks, whose actions over the past century (now that we are just 31 days away from the 100 year anniversary of the Fed) have led to a world in which there are hundreds of trillions in unfunded, insolvent entitlements, as well as a central planner policy response aimed squarely at obliterating any residual negotiating position labor may have had.

To summarize: as fury at corporate CEOs rises, don’t forget to save some where it also most certainly belongs: the Federal Government and the Chairman.