George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

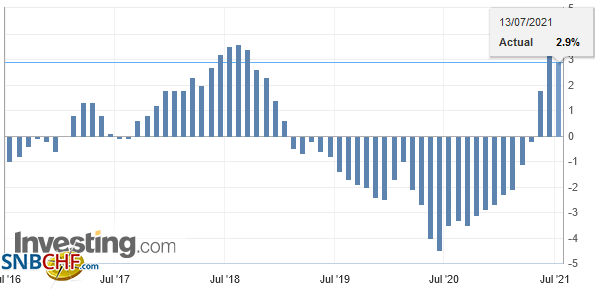

Swiss FrancSpeculators were net short CHF in January 2015, shortly before the end of the peg, with 26.4K contracts. Then again in December 2015, when they expected a Fed rate hike, with 25.5K contracts.The biggest short CHF, however, happened in June 2007, when speculators were net short 80K contracts. Shortly after, the U.S. subprime crisis started. The carry trade against CHF collapsed. The reverse carry trade in form of the Long CHF started and lasted - without some interruptions - until the peg introduction in September 2011. In mid 2011, the long CHF trade became a proper carry trade - and not a reverse carry trade anymore - because investors thought that the SNB would hike rates earlier than the Fed. CHF Speculative PositionsLast data as of August 15: The net speculative CHF position has fallen from 1.4K short to 1.2K contracts short (against USD).

|

Speculative PositionsChoose Currency source: Oanda |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Marc Chandler My articles My offerMy siteAbout meMy videosMy books Follow on:LinkedINTwitterSeeking AlphaAmazon Speculators made several significant position adjustment in the CFTC reporting week ending August 15, that included an escalation of aggressive rhetoric by the US and North Korea. The reporting period also covered a domestic terrorist incident in the US, and the White House response led to the defection of leaders of America’s largest businesses from advisory councils, ultimately forcing the President to end the entire exercise.As one might expect, speculators continued to reduce gross short yen positions. They have done so for four consecutive reporting periods for a total of around 43k contracts. In the most recent period, 14.8k contracts were covered, leaving a gross short position of a still substantial 120.8k contracts.In the context of geopolitical anxiety, and perhaps the start of the new NAFTA negotiations, some speculators thought the peso was a short. The bears added 11.8k peso contracts to the gross short position, lifting by nearly 50% to 36.1k contracts. It is interesting to note that the bulls have note flinched and held gross long position little changed around 131k contracts for the fifth consecutive week.The euro has been consolidating it earlier gains since the start of the month. Some speculators may have been long euros against the yen. The covering of the short yen positions may have been part of unwinding the entire position, which meant selling euros. Speculators trimmed the gross long euro position by 5% or 10.9k contracts to 190.3k. The shorts have not been emboldened. They added a mere 3.5k contracts to lift the gross short position to 111.7k contracts.Speculators turned more bearish sterling, perhaps as the data makes a rate hike seem less likely (the implied yield of the December short-sterling futures contract has fallen 17 bp since the beginning of last month). The bears added nearly 12k contracts to the gross short position so it stands at 95.7k contracts.The pressure on the Canadian dollar began before the flare-up of geopolitical tensions or the latest drama in Washington. The pullback after a sustained rally since early May began in late July. However, through the pullback speculators continued to build the gross long position. They have done this for the past ten reporting periods, but the spree was snapped last week. The gross long position was up by 11.8k contracts to 86.5k. The net long US 10-year Treasury speculative position fell to 200.6k contracts from 229.8k. It is the smallest net long position since May. The bulls liquidated 13.1k contracts, leaving a gross long position of 887.6k contracts. The bears took on another 16.1k contracts to raise the gross short position to 687k contracts. Speculators also turned less bullish oil. The gross long position was trimmed by 8.2k contracts, but it still is substantial–just below 700k contracts (each contract represents 1000 barrels of oil). The gross short position rose by 9k contracts to 235.9k. |

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Full story here Are you the author?

Tags: Commitment of Traders,EUR/CHF,newslettersent,Speculative Positions,USD/CHF