George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

We do not like Purchasing Power or Real Effective Exchange Rate (REER) as measurement for currencies. For us, the trade balance decides if a currency is overvalued. Only the trade balance can express productivity gains, while the REER assumes constant productivity in comparison to trade partners.

Who has read Michael Pettis, knows that a rising trade surplus may also be caused by a higher savings rate while the trade partners decided to spend more. This is partially true.

Recently Europeans started to increase their savings rate, while Americans reduced it. This has led to a rising trade and current surplus for the Europeans.

But also to a massive Swiss trade surplus with the United States, that lifted Switzerland on the U.S. currency manipulation watch list.

To control the trade balance against this “savings effect”, economists may look at imports. When imports are rising at the same pace as GDP or consumption, then there is no such “savings effect”.

After the record trade surpluses, the Swiss economy may have turned around: consumption and imports are finally rising more than in 2015 and early 2016. In March the trade surplus got bigger again, still shy of the records in 2016.

Swiss National Bank wants to keep non-profitable sectors alive

Swiss exports are moving more and more toward higher value sectors: away from watches, jewelry and manufacturing towards chemicals and pharmaceuticals. With currency interventions, the SNB is trying to keep sectors alive, that would not survive without interventions.

At the same time, importers keep the currency gains of imported goods and return little to the consumer. This tendency is accentuated by the SNB, that makes the franc weaker.

Texts and Charts from the Swiss customs data release (translated from French).

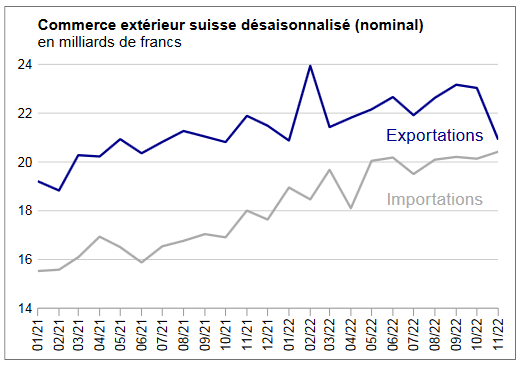

Exports and Imports YoY DevelopmentIn August 2017, Swiss foreign trade grew stronger both at entry and exit. With growth of 9.9%, imports were much more dynamic than exports (+ 3.9%). The balance of trade closed with a surplus of 2.2 billion francs. In short |

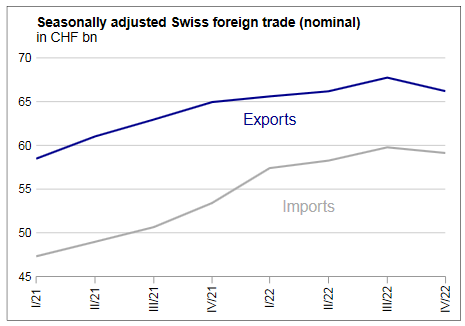

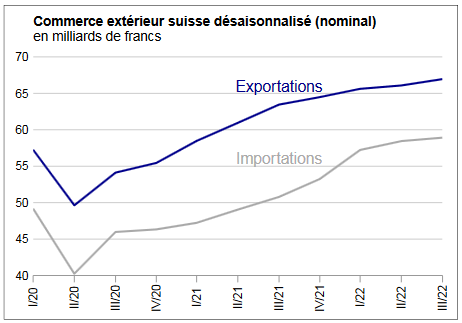

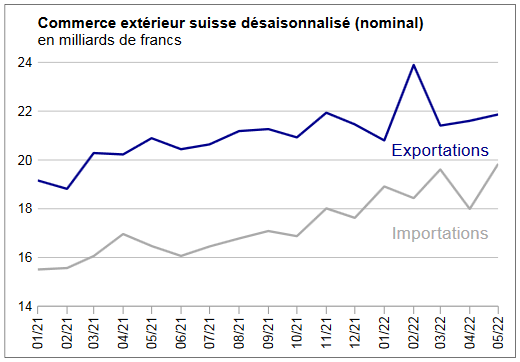

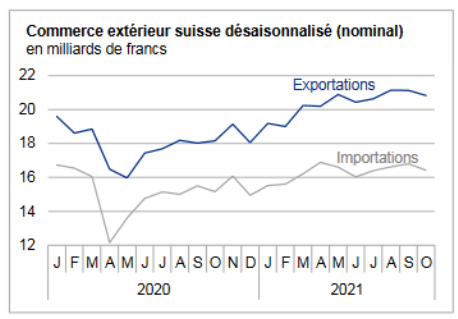

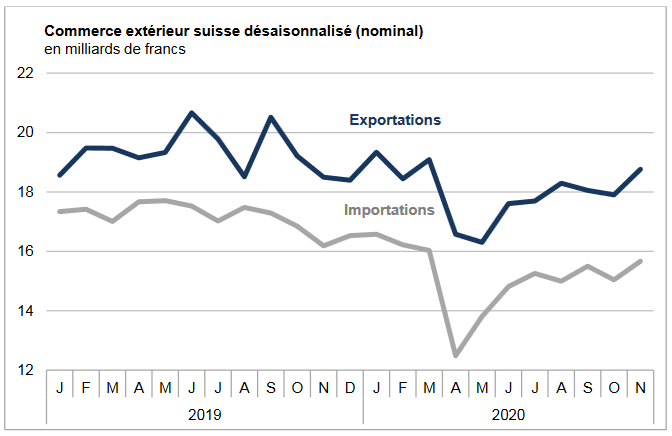

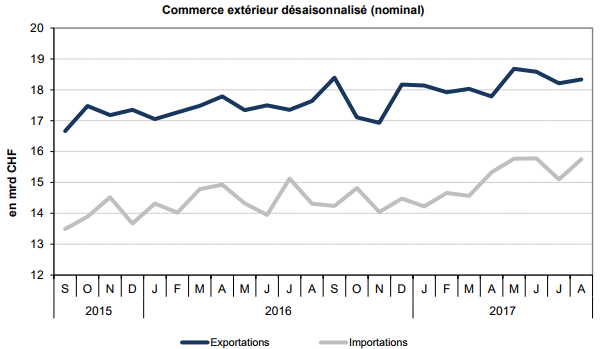

Swiss exports and imports, seasonally adjusted (in bn CHF), August 2017(see more posts on Switzerland Exports, Switzerland Imports, ) Source: Swiss Customs - Click to enlarge |

Overall EvolutionIn August 2017, exports adjusted for working days increased by 3.9% (actual: + 6.1%) over one year. Compared to July (seasonally adjusted), they increased by 0.7%, confirming the positive trend recorded so far. Imports jumped 9.9% year on year (real: + 6.5%) and 4.3% on the previous month. The upward trend since the beginning of the year has thus been strengthened. |

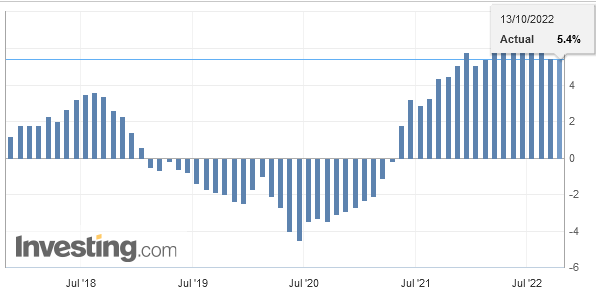

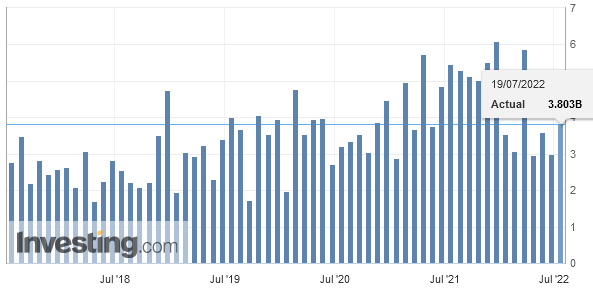

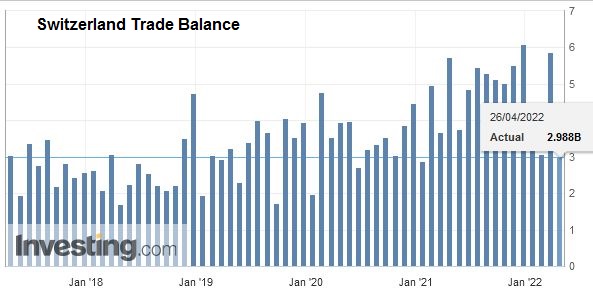

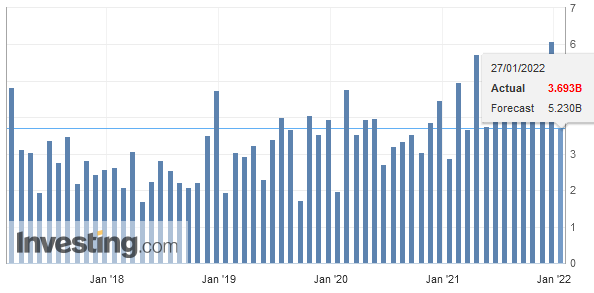

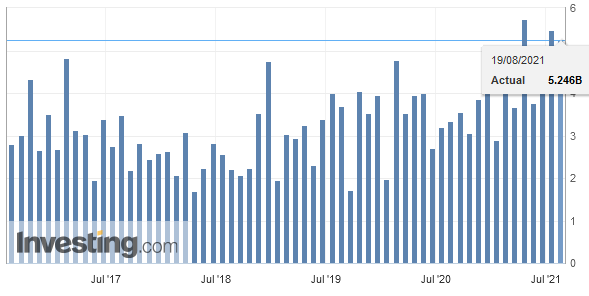

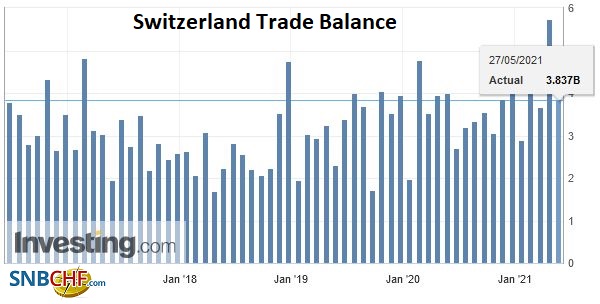

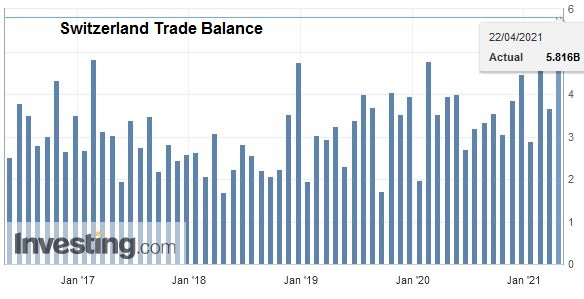

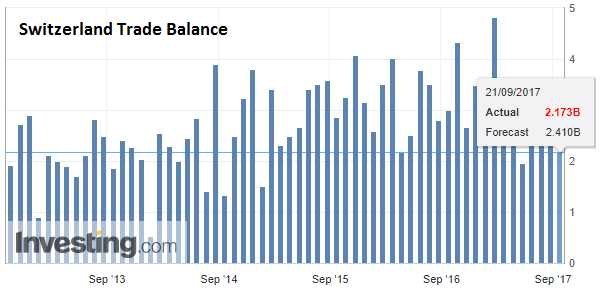

Switzerland Trade Balance, August 2017(see more posts on Switzerland Trade Balance, ) Source: Investing.com - Click to enlarge |

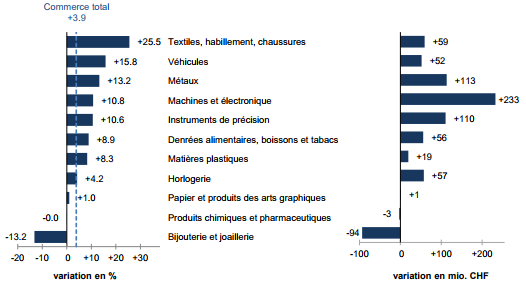

ExportsThree-quarters of growth on the MEM industry products accountExports of all commodity groups increased, with the exception of jewellery (-13%) and chemicals and pharmaceuticals (-0%). The machinery and electronics sector (+233 million francs) alone accounted for two-fifths of exit growth. In addition to textiles, clothing and footwear, vehicles (+ 16%, aeronautics) also showed up. MEM products – metals, machinery and electronics as well as precision instruments – grew by 11 to 13% (+ CHF 456 million in total). The dynamism of machinery was mainly driven by machinery (+ 43%) and machine tools (+ 17%). Watch sales were up 4%. In chemistry-pharma, the decline in drugs and active ingredients led to the group’s result. Swiss exports gained ground on all continents, with Oceania heading (+ 64%). Among the main markets, Asia (+ 8%) was the most dynamic, stimulated by China (+263 million francs). The North American increase (+ 2%) has, once is not customary, based on Canada (+ 35%) and not on the USA (-1%). European demand (EU: -0%) increased by 1%. This has mainly taken root in Russia (+ 84%) and Germany (+ 7%). France (-19%) and the United Kingdom (-13%), for their part, plunged. For all the countries mentioned, the chemical and pharmaceutical products have marked the result of their imprint. |

Swiss Exports per Sector August 2017 vs. 2016(see more posts on Switzerland Exports, Switzerland Exports by Sector, ) Exports by commodity group: Nominal changes adjusted for working days compared with August 2016 Source: Swiss Customs - Click to enlarge |

ImportsThe rise of imports is concentrated on neighboring countriesThe 10% jump in imports was largely sustained, although the two main commodity groups, machinery and electronics and pharmaceuticals generated half of the growth. Jewellery (+ 51%) played the spearheads. Products Geographically, Asia (+ 14%) and Europe (+ 12%) were the engine of growth. On the Asian continent, the United Arab Emirates (+107 million francs, jewellery), Japan (+ 33%) and China (+ 6%) were at the forefront. The rise of the Old Continent mainly came from neighboring countries Germany, France and Italy. This trio contributed 800 million francs to the positive development of imports. Note also the dynamism of Ireland (+ 27%). North American arrivals, on the other hand, fell by 5% (USA: -9%). |

Swiss Imports per Sector August 2017 vs. 2016(see more posts on Switzerland Imports, Switzerland Imports by Sector, ) Exports by commodity group: Nominal changes adjusted for working days compared with August 2016 Source: Swiss Customs - Click to enlarge |

Full story here Are you the author?

Tags: newslettersent,Switzerland Exports,Switzerland Exports by Sector,Switzerland Imports,Switzerland Imports by Sector,Switzerland Trade Balance