George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

We do not like Purchasing Power or Real Effective Exchange Rate (REER) as measurement for currencies. For us, the trade balance decides if a currency is overvalued. Only the trade balance can express productivity gains, while the REER assumes constant productivity in comparison to trade partners.

Who has read Michael Pettis, knows that a rising trade surplus may also be caused by a higher savings rate while the trade partners decided to spend more. This is partially true. Recently Europeans started to increase their savings rate, while Americans reduced it. This has led to a rising trade and current surplus for the Europeans. But also to a massive Swiss trade surplus with the United States, that lifted Switzerland on the U.S. currency manipulation watch list.

To control the trade balance against this “savings effect”, economists may look at imports. When imports are rising at the same pace as GDP or consumption, then there is no such “savings effect”.

After the record trade surpluses, the Swiss economy may have turned around: consumption and imports are finally rising more than in 2015 and early 2016. In March the trade surplus got bigger again, still shy of the records in 2016.

Swiss National Bank wants to keep non-profitable sectors alive

Swiss exports are moving more and more toward higher value sectors: away from watches, jewelry and manufacturing towards chemicals and pharmaceuticals. With currency interventions, the SNB is trying to keep sectors alive, that would not survive without interventions.

At the same time, importers keep the currency gains of imported goods and return little to the consumer. This tendency is accentuated by the SNB, that makes the franc weaker.

| 19.08.2021 – Secondary sector production rose by 14.2% in 2nd quarter 2021 in comparison with the same quarter a year earlier. Turnover rose by 15.5%. These sharp increases can largely be explained by the weak 2nd quarter of 2020, during which measures against the COVID-19 pandemic came into effect. This is shown by provisional results from the Federal Statistical Office (FSO).

Compared with the previous year, production in the industrial sector rose in April (+16.1%), in May (+17.4%) and in June (+13.1%). For the whole of 2nd quarter 2021 production increased by 15.7% in comparison with the same quarter a year earlier. Construction production increased by 6.5% in 2nd quarter 2021 in comparison with the same quarter a year earlier. Production rose by 4.9% in building, civil engineering in contrast registered a decline (–2.1%). Lastly, specialised construction activities registered an increase of 8.8% in their production. Turnover Turnover in the industrial sector rose in April (+18.5%), in May (+19.6%) and in June (+14.1%) compared with the previous year. For the whole of 2nd quarter 2021 in comparison with the same quarter a year earlier, turnover registered an increase of 17.4%. Construction turnover rose by 8.1% in 2nd quarter 2021 in comparison with the same quarter a year earlier. Turnover rose by 7.5% in building, Civil engineering registered a decline of 1.0%, specialised construction activities an increase of 9.4%. Comparison with pre-pandemic period If the results of the indices are compared with the results of the 2nd quarter 2019, i.e. the last comparable period prior to the outbreak of the pandemic, different rates of change emerge: The two-year comparison shows a 5.0% increase in production in industry when the 2nd quarter 2021 is compared with the 2nd quarter 2019 (turnover: +2.4%). Similar comparison in construction production shows an increase of 1.2% (turnover: +2.9%). Lastly, the same comparison applied to the secondary sector shows an increase in production of 4.4% (turnover: +2.5%). |

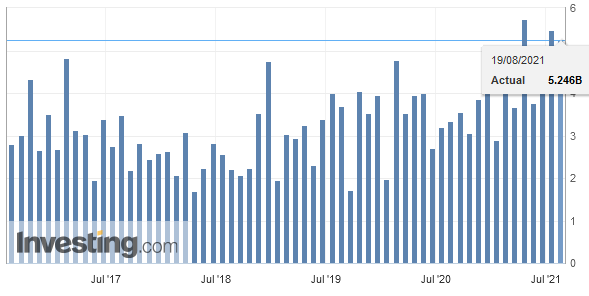

Switzerland Trade Balance, July 2021(see more posts on Switzerland Trade Balance, ) - Click to enlarge |

Download press release: Production and turnover in Switzerland’s secondary sector rose sharply in 2nd quarter 2021

Full story here Are you the author?Tags: Featured,newsletter,Switzerland Exports,Switzerland Exports by Sector,Switzerland Imports,Switzerland Imports by Sector,Switzerland Trade Balance