George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

|

Swiss Franc Currency Index

The major information about the Swiss economy since the beginning of the year were:

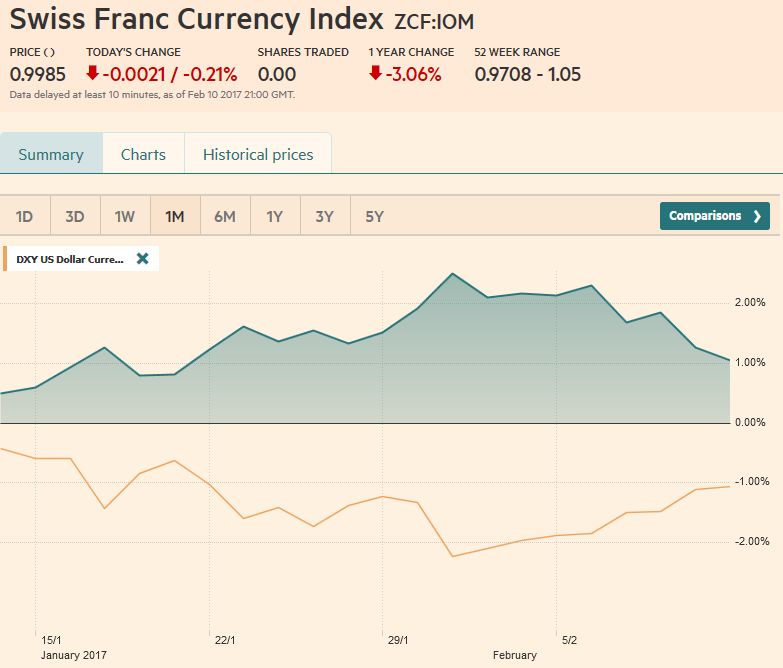

While in 2015, the trade surplus still expanded, we see clear tendencies that in 2017 the Swiss economy will be driven more strongly by internal demand. It could even be a light form of a “boom”, namely when domestic demand rises more strongly than GDP. We are expecting a further strengthening of both dollar and Swiss Franc against the euro over the next 3 months. Reason is the rising Swiss demand the continued dovishness of the ECB, despite rising inflation.

|

Trade-weighted index Swiss Franc, February 11(see more posts on Swiss Franc Index, ) Source: markets.ft.com - Click to enlarge |

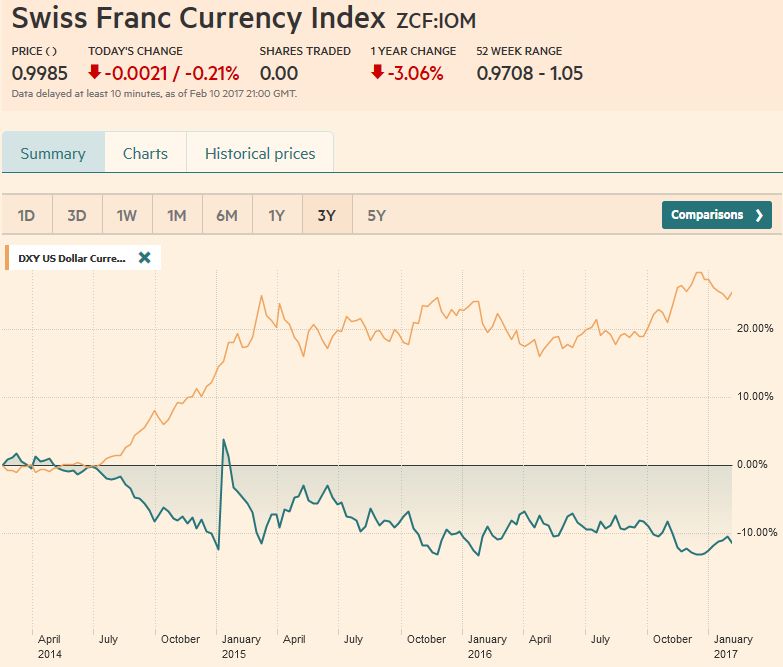

Swiss Franc Currency Index (3 years)The Swiss Franc index is the trade-weighted currency performance (see the currency basket)On a three years interval, the Swiss Franc had a weak performance. The dollar index was far stronger. The dollar makes up 33% of the SNB portfolio and 25% of Swiss exports (incl. countries like China or Arab countries that use the dollar for exchanges). Contrary to popular believe, the CHF index gained only 1.73% in 2015. It lost 9.52% in 2014, when the dollar (and yuan) strongly improved. |

Swiss Franc Currency Index (3 years), February 11(see more posts on Swiss Franc Index, ) Source: markets.ft.com - Click to enlarge |

|

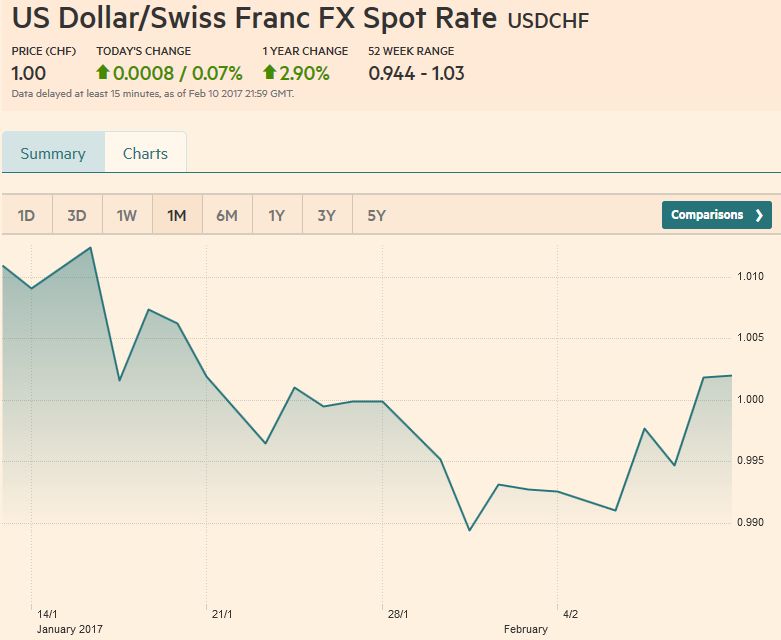

Marc Chandler My articles My offerMy siteAbout meMy videosMy books Follow on:LinkedINTwitterSeeking AlphaAmazon USD/CHFFor the last several weeks, we have been looking for the dollar correction that began around the Fed’s rate hike in the middle of December to be completed and for the uptrend to resume. The precise timing of the turn is difficult to get right, but our view is anchored by our macroeconomic assessment and is understanding of the key drivers. Our technical work suggests the dollar indeed has been carving out a bottom, and we expect the uptrend to resume. Our confidence would be raised if we saw confirmation in other markets. For example, the Fed funds futures imply (slightly) less of a chance of a hike in March and June from a week ago. It would also be helpful if the next string of data (CPI, retail sales, and industrial output) would be stronger than expected, as the median forecasts are all for softer numbers. We suggest a few considerations helped solidify the dollar’s bid. First, regardless of some disappointing data (wage growth, January auto sales, the first estimate of Q4 GDP), the Fed officials that spoke still seemed confident in the economy and the appropriateness of a gradual increase in interest rates. Second, it seems as if Trump’s talking the dollar down was not the start of some campaign but likely his blustering style. He reportedly asked the National Security Adviser about whether it is a weak or stronger dollar that is best for America. He also indicated that the issue of currency manipulation was not high on the agenda as he met with Japan’s Prime Minister Abe. Third, Trump’s tweets and off-hand comments may be losing their sting. We see what happened to the shares of the retailer who dared to discount his daughter’s line of clothes. The Mexican peso had fallen sharply but since January 19 is the strongest currency in the world, gaining 7.8% against the US dollar. Fourth, the President seemed to moderate his whack-a-mole approach to policy last week He signaled that he would honor the US commitment to the one-China policy. He made some overtures toward NATO. He maintained continuity with the US stance toward Greek debt forgiveness. He warned Israel that the construction on the West Bank was not helpful. Finally, Trump reaffirmed the campaign’s commitment to lower taxes. A major proposal is said to be a few weeks away. Trump says it will be “phenomenal.” This is important. Some economists think that lower corporate tax rates will boost investment and the growth potential, and strengthen the dollar. Other economists, including the elder statesmen Martin Feldstein, have argued that a 20% tax on imports will hit most the dollar by 25% automatically. We have expressed skepticism about what appears to us as a naive form of purchasing power parity. We do not think the foreign exchange prices automatically adjust. The market for capital is larger and arguably more important at the beginning of the 21st century than the market for goods in determining the exchange rates of the major currencies. Nevertheless, as talking with various market participants, there seems to be a general reluctance to reduce dollar exposure.

|

US Dollar/Swiss Franc FX Spot Rate, February 11(see more posts on USD/CHF, ) Source: markets.ft.com - Click to enlarge |

US Dollar IndexThe Dollar Index snapped a four-week drop and posted the biggest weekly advance since the Fed hiked two months ago. It closed at the best level of the month, The Dollar Index’s low was recorded on February 3, and with the recent gains, it has not completed a 38.2% retracement of the decline (~101) since the start of the year. The 50% retracement is near 101.50, leaving the 61.8% retracement around 102. The five-day moving average crossed above the 20-day moving average for the first time since January 5. The RSI is trending higher, but both the MACDs and Slow Stochastics have turned higher from over-extended levels. The Dollar Index rose above this year’s downtrend line, came back down to test it and it held. At the same time, a modest uptrend line can be drawn off the lows since February 3. It is found near 100.35 on Monday and rises toward 101 by the end of next week. |

US Dollar Currency Index, February 11(see more posts on Dollar Index, ) Source: markets.ft.com - Click to enlarge |

EUR/USDThe euro lost about 1.25% against the dollar last week to reach its lowest level (~$1.0610) since January 19 low of $1.0585. That low also corresponds to the 50% retracement of the euro’s recovery this year after slipping through the low near $1.0350 seen within a few days of the Fed’s hike in December. The lower Bollinger Band and the 50-day moving average are near $1.06. The 38.2% retracement was found a little below $1.0645, which held on the initial test. The five-day moving average has crossed below the 20-day moving average for the first time since January 5. The MACDs and Slow Stochastics are trending lower, as is the RSI. We recognize that a move above $1.07 would negate this bearish outlook.

|

EUR/USD with Technical Indicators, January 24 - February 11(see more posts on Bollinger Bands, EUR/USD, MACDs Moving Average, RSI Relative Strength, Stochastics, ) EUR/USD Week Ending February 11 with Technical Indicators - Click to enlarge |

USD/JPYThe dollar built a base in the JPY111.60-JPY111.80 area. From there it made a run for the downtrend line from the start of the year near JPY113.85. To do so, it marginally surpassed the 38.2% retracement of that decline that comes in at JPY113.60. The 50% retracement is JPY114.30, and the 61.8% retracement is JPY115.10, which also corresponds with the 50-day moving average. The MACDs are crossing higher, but the Slow Stochastics are lagging. Although the US 10-year premium narrowed a little week, in the last couple of sessions, it widened by 10 bp. Trump’s signal that currency manipulation was on the agenda for the meeting with Abe may have also encouraged some pent-up demand for dollars. |

USD/JPY with Technical Indicators, January 24 - February 11(see more posts on Bollinger Bands, MACDs Moving Average, RSI Relative Strength, Stochastics, USD/JPY, ) USD/JPY Week Ending February 11 with Technical Indicators - Click to enlarge |

GBP/USDSterling was the best performing major currency last week, which entailed rising less than 0.2% against the rising dollar. Prime Minister May is expected to trigger Article 50 at the EU summit in early March. As the details of the radical surgery are negotiated, there may be headline risk from time-to-time, but it may be superseded in the short-term by a macroeconomics, the focus on EMU politics, and the general dollar direction. The US rate premium over the UK has begun growing again, and this may also weigh on sterling. However, sterling is resilient against the dollar, and we suspect it comes from the demand against the euro. Sterling held the 50% retracement level near $1.2345 last Tuesday, and although the upside momentum faded, the underlying tone remains firm. Initial resistance may be near $1.2530, but the $1.2570-$1.2600 may be a stronger cap. Watch the GBP0.8470 area for the euro.It appears to correspond to a neckline of some topping pattern. It valid pattern and the neckline is successfully penetrated, the measuring objective is below GBP0.8100. Moreover, the charts suggest some risk that if/when the break comes, it could accelerate quickly. |

GBP/USD with Technical Indicators, January 24 - February 11(see more posts on Bollinger Bands, GBP/USD, MACDs Moving Average, RSI Relative Strength, Stochastics, ) GBP/USD Week Ending February 11 with Technical Indicators - Click to enlarge |

AUD/USDThe Australian dollar is in a $0.7600-$0.7700 trading range. Demand seems stronger than supply, and the Aussie finished the week near the highs. The technical signals are mixed, but none suggest that the $0.7700 area will hold. We are not convinced it has much farther to go, and consequently, will be particularly attentive to a reversal pattern or some technical indication that the rally is faltering.

|

AUD/USD with Technical Indicators, January 24 - February 11(see more posts on Australian Dollar, Bollinger Bands, MACDs Moving Average, RSI Relative Strength, Stochastics, ) AUD/USD Week Ending February 11 with Technical Indicators - Click to enlarge |

USD/CADA healthy Canadian employment report saw the US dollar break down to test the 61.8% retracement objective (~CAD1.3060) of the rally since the start the end of January when the greenback reached CAD1.2970. The Slow Stochastics are still moving higher. The MACDs may roll back over, and the RSI is trending lower. Even if the US dollar eases at the start of next week, we think the downside is limited. The two-year interest rate differential is flat in the middle of the this year’s narrow range (~42 bp), and the 10-year differential is flat this year in a six basis point range (~70 bp). In a strong US dollar environment, the Canadian dollar often does better on the crosses. |

USD/CAD with Technical Indicators, January 24 - February 11(see more posts on Bollinger Bands, Canadian Dollar, MACDs Moving Average, RSI Relative Strength, Stochastics, ) USD/CAD Week Ending February 11 with Technical Indicators - Click to enlarge |

Crude OilThe March light sweet crude oil futures contract staged an impressive rally starting at midweek. The 5.5% advance took the contract to the upper end of the month-old trading range around $54 a barrel. News that there has been strong compliance of the OPEC (and non-OPEC) agreement helped the contract finish the week on a firm note. The RSI and MACDs are moving higher, while the Slow Stochastics are heavy. Our near-term bias is toward higher prices, and above $54 lies the last two higher a little above $56, which would be the next target. |

Crude Oil, March 2016-Feb 2017(see more posts on Crude Oil, ) Source: Bloomberg.com - Click to enlarge |

U.S. TreasuriesThe US 10-year yield continues to trade heavily. The move down successfully tested last month’s low near 2.30%. Yields recovered toward ahead of the weekend to as high as 2.43% before running out momentum. Essentially, the 10-year is in a 2.30% to 2.50% range. Despite concerns about China and other countries’ sales of Treasuries, the yield was nearly 30 bp lower than when the Fed hiked last December. The March note futures need to be sold below the 124-10 to 124-18 band to be of note. The note futures is capped near 125-16. Should this ceiling be broken, there is scope a leg to 126-15 and possibly toward 127-12. |

Yield US Treasuries 10 years, March 2016-Feb 2017(see more posts on U.S. Treasuries, ) Source: Bloomberg.com - Click to enlarge |

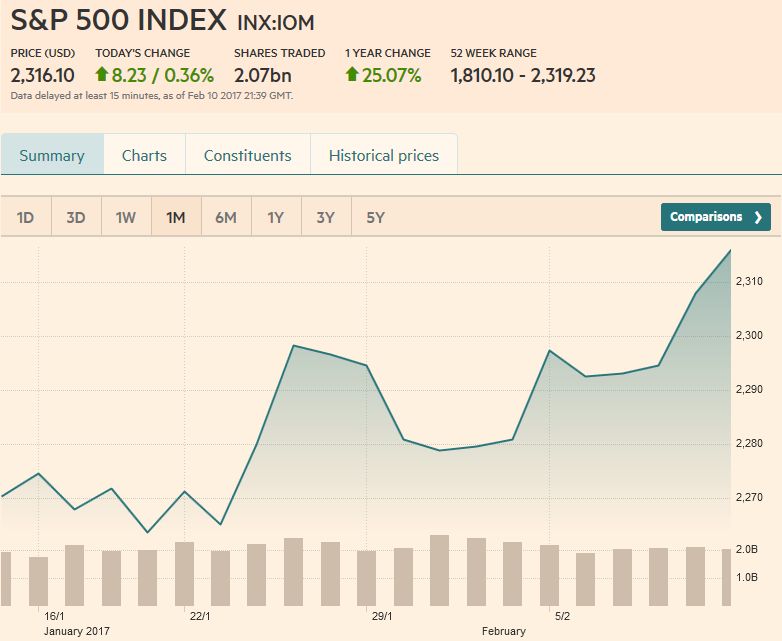

S&P 500 IndexWith promises of tax reform soon and an emphasis on deregulation, equity prices advanced. All three major indices, the S&P 500, the NASDAQ, and the Dow Jones Industrials saw record highs before the weekend. Our reading of the technical condition and psychology suggest a new leg up in the market has begun. Many asset managers have been reluctant to commit more money to the market without a pullback and clear visibility about the policies and priorities of the new Administration. Some investors appear more confident that the institutional constraints, including the judiciary branch, and clear national interests (one-China policy, opposition to Russian aggression, disapproval of Israel undertaking more construction on the West Bank) may neutralize some of the more extreme impulses. However, as we saw with Brexit, the populist-nationalist efforts are made possible by the cooperation of the conservative party, as opposed to continental European experience where the center-right brooks little tolerance of the populist-nationalist parties. Lastly, one element of the tax reform that many are not focusing on is the promise to end tax incentives for debt. This will have far-reaching implications for companies and sectors. Most attention appears to have gone toward the border adjustment (tax on imports, a tax break for exports), which also would be a significant catalyst for change and disruption.

|

S&P 500 Index, February 11(see more posts on S&P 500 Index, ) Source: markets.ft.com - Click to enlarge |

Are you the author?

Tags: Australian Dollar,Bollinger Bands,British Pound,Canadian Dollar,Crude Oil,Dollar Index,EUR/CHF,EUR/USD,Euro,Euro Dollar,Japanese yen,MACDs Moving Average,newslettersent,RSI Relative Strength,S&P 500 Index,Stochastics,Swiss Franc Index,U.S. Treasuries,usd-jpy,USD/CHF,USD/JPY