Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Weekly Market Pulse: A Fatal Conceit

Weekly Market Pulse: A Fatal Conceit24 Jan 2023

Update The Conflict of Interest Rate(s)13 Jun 2022

No Pandemic. Not Rate Hikes. Doesn’t Matter Interest Rates. Just Globally Synchronized.6 Jun 2022

UST 2s & Euro$ Futures *Whites* Both Ask, Landmine At Last?25 May 2022

Looking Back At Chaotic March Through TIC20 May 2022

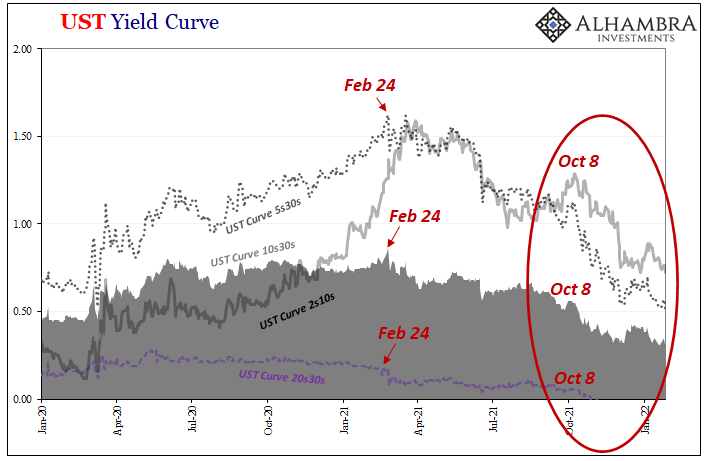

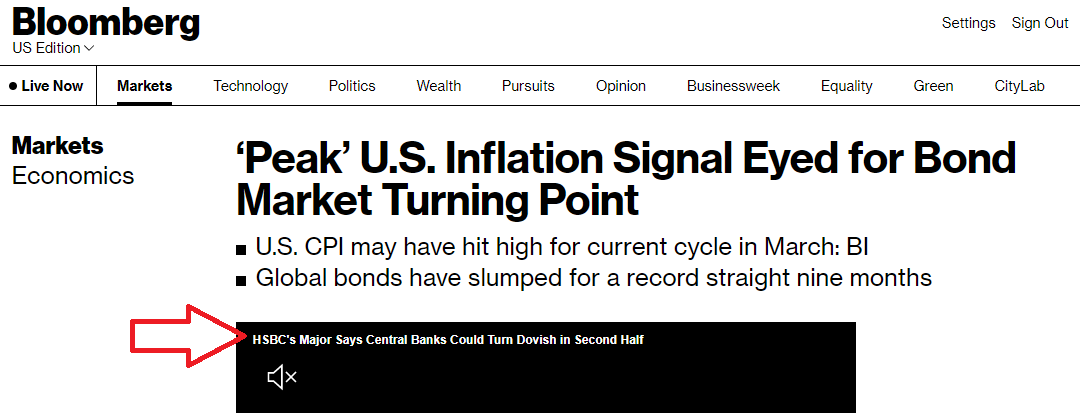

Peak Inflation (not what you think)

Peak Inflation (not what you think)15 May 2022

China, Japan, And The Relative Pre-March Euro$ Calm In February22 Apr 2022

Yield Curve Inversion Was/Is Absolutely All About Collateral18 Apr 2022

The Short, Sweet Income Case For Ugly Inversion(s), Too4 Apr 2022

We Can Only Hope For Another (bond) Massacre30 Mar 2022

Inversion Is The Real March Madness, Just Don’t Take It Literally22 Mar 2022

The Fed Inadvertently Adds To Our Ironclad Collateral Case Which Does Seem To Have Already Included A ‘Collateral Day’ (or days)21 Mar 2022

Media Attention All Over FOMC, Market Attention Totally Elsewhere19 Mar 2022

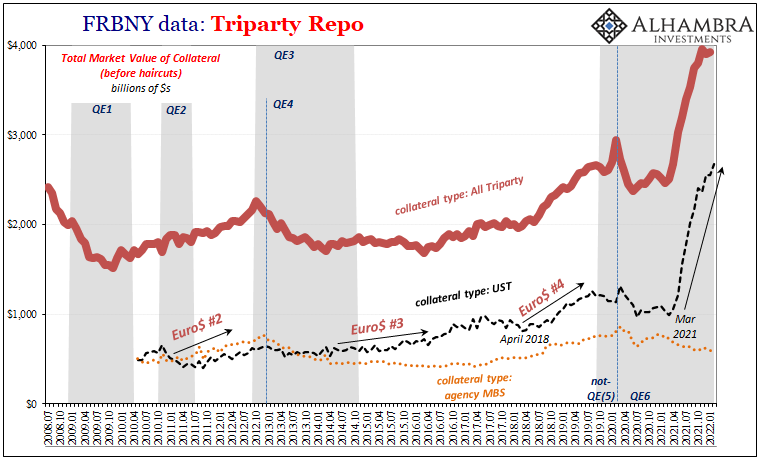

There Is An Absolutely Solid Collateral Case For What’s Driving Curve Inversion(s) [Part 2]18 Mar 2022

There Is An Absolutely Solid Collateral Case For What’s Driving Curve Inversion(s) [Part 1]17 Mar 2022

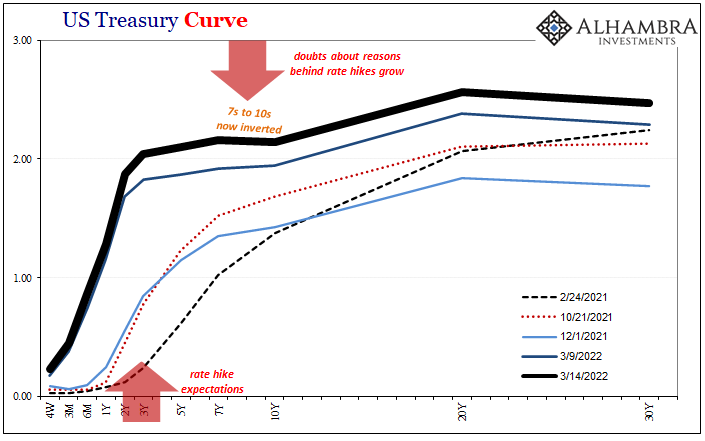

Another One Inverts, The Retching Cat Reaches Treasuries15 Mar 2022

Consumer Prices And The Historical Pain(s)12 Mar 2022

So Much Fragile *Cannot* Be Random Deflationary Coincidences

So Much Fragile *Cannot* Be Random Deflationary Coincidences10 Mar 2022

Houston, We Have An Oil (and inventory) Problem7 Mar 2022

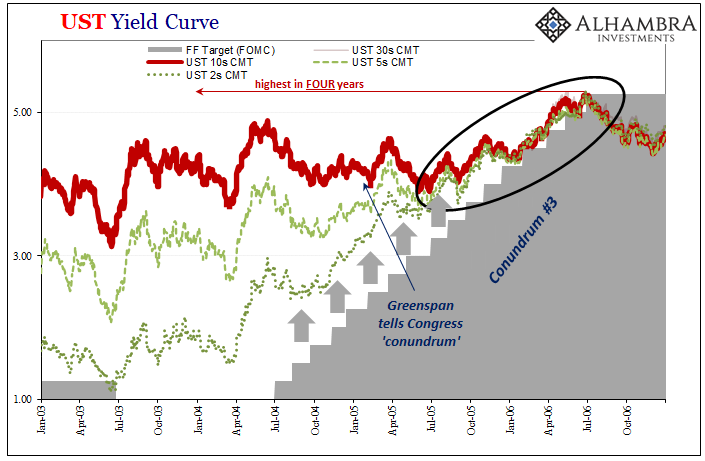

After Today’s FOMC, Yield Curve Is Already As Flat As It Was In Mar ’18 **Without A Single Rate Hike Yet**28 Jan 2022