George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Richard Koo’s Central Banks in Balance Sheet Recessions: A Search for Correct Response

In the following some extracts:

Koo bashes Quantitative Easing as pure measure to increase asset prices:

About the inability of FX markets to judge the effects of monetary expansion:

Koo: As more and more people began to realize that increases in monetary base via QE during balance sheet recessions do not mean equivalent increases in money supply, the hype over QEs in the FX market is likely to calm down. At the moment, however, that is not yet the case, as the sharp fall of the yen following the announcement of Abenomics with its commitment to monetary easing amply demonstrates….The only way quantitative easing can have a positive impact on economic activity is if the authorities’ purchase of assets from the private sector boosts asset prices, making people feel wealthier and thereby encouraging them to consume more. This is the wealth effect, often referred to by the Fed chairman Bernanke as the portfolio rebalancing effect, but even he has acknowledged that it has a very limitmued impact.

….

In a sense, quantitative easing is meant to benefit the wealthy. After all, it can contribute to GDP only by making those with assets feel wealthier and encouraging them to consume more.

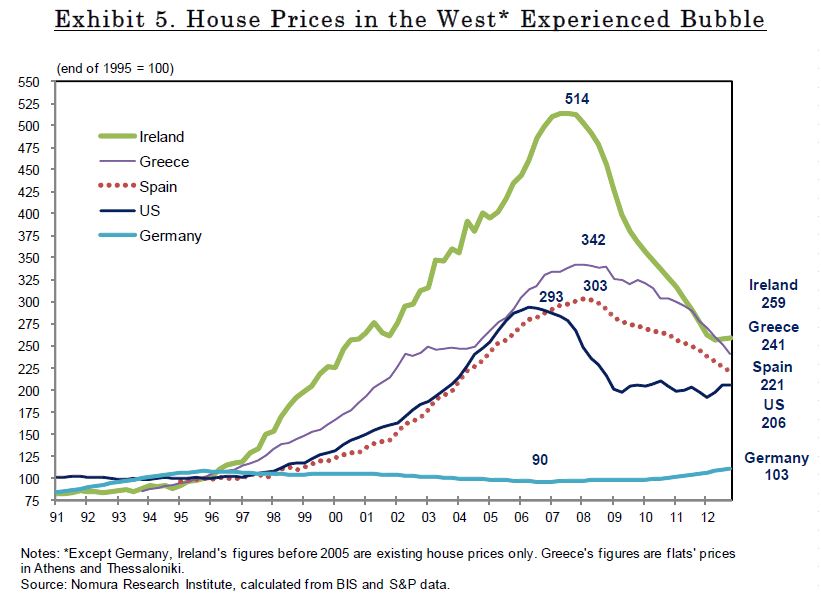

Home prices of countries with trade deficits increased due to unnaturally low interest rates

The following graph suggests that differences in the development of home prices among major nations will need to re-adjust to the mean of 1991, i.e. German prices must rise and/or the ones with current account deficits and a tradition of high rates must fall.

Money supply versus monetary base

Koo: For example, the US monetary base grew from 100 at the time of Lehman Shock to 347 today as mentioned earlier, but the money supply grew only from 100 to 135 during the same period. In the UK where the monetary base now stands at 433, the money supply is stuck at a pitiful 110. In the Eurozone, the monetary base is at 157 while the money supply is at 107. In Japan, the monetary base is at 150 while the money supply is at 113.

For comparison the Swiss National Bank has increased its monetary base from 100 (49.5 billion francs) in 2008 to 689 (i.e. 341.5 billion francs). The money supply in terms of M1 has risen to from level 100 (273 bln. CHF) in 2008 to 197 (538 bln.), far better than the Eurozone, US, UK and Japan. Swiss M3, however, rose only from 100 level (i.e. 626 bln.) to 138 (i.e. 860 bln. CHF). (source Source SNB month bulletin)

Similarly the monetary base compared to credit to private sector:

For comparison the Swiss credit to private sector has increased from 100 in 2008 to total debtors of 110 and to Swiss debtors to 115. (source Source SNB month bulletin, page 44).

FX traders do not understand link between monetary base and money supply

Koo: Instead, foreign exchange dealers and traders, who probably do not have time to think about the complicated link between monetary base and money supply during balance sheet recessions, simply assumed the textbook case where monetary base and money supply are expected to move in tandem (which was indeed true before the bursting of the bubble).

Koo affirms that fiscal spending and not monetary policy saved the US from the Great Depression :

Koo: Unfortunately there was a period in economics profession, from late 1980s to early 2000s, where many noted academics tried to re-write the history by arguing that it was monetary and not fiscal policy that allowed the US economy to recover from the Great Depression. They made this argument based on the fact that the US money supply increased significantly from 1933 to 1936. However, none of these academics bothered to look at what was on the asset side of banks’ balance sheets.

The asset side of banks’ balance sheet clearly indicates that it was lending to the government that grew during this period (Exhibit 10). The lending to the private sector did not grow at all during this period because the sector was still repairing its balance sheets. And the government was borrowing because the Roosevelt Administration needed to finance its New Deal fiscal stimulus. In other words, it was Roosevelt’s fiscal stimulus that increased both the GDP and money supply after 1933.

…Although deficit spending is frequently associated with crowding out and misallocation of resources, during balance sheet recessions, the opposite is true.

Koo delivers an explanation for falling bond yields.

Koo: In most countries, they are not supposed to take too much foreign exchange risk, and they are also not supposed to take too much principle risk, meaning that not all funds can be invested in equities, that a large portion must be invested in fixed income assets, i.e., bonds.When investors with these restrictions are faced with a private sector that is not borrowing money at all, the only asset these investors can invest in would be their own government bonds. This is because the government is the only borrower left in the country. As a result, a large portion of the saved and deleveraged funds end up in government bond market, resulting in ridiculously low bond yield during this type of recessions.

Low bond yield, in turn, is a natural corrective mechanism that helps governments put in necessary fiscal stimulus to support their economies during balance sheet recessions.

About the Euro zone:

Koo: As a result, there has been a huge capital flight out of peripheral countries to Germany, resulting in a ridiculously low Bund yield of 1.5 percent or less at ten years for a country with the lowest unemployment rate in 20 years and the largest-ever industrial production.

…

If the different risk weights manage to keep sufficient domestic savings at home, bond yields [in the periphery] will come down.

…

The OMT by the ECB announced last year may be viewed as an effort to return the savings back to the countries that generated them. However, the conditions attached to the OMT, that receiving countries engage in fiscal consolidation, are totally counter-productive when the countries are facing balance sheet recessions.

..

In other words, they are apparently aware that Europe is in a balance sheet recession. And yet Mr. Draghi is still insisting that these countries continue with their fiscal austerity which not only does not follow from his own diagnosis that these economies are in balance sheet recessions, but is also making recessions in these countries much worse.

..

The booming economies of the periphery also allowed the Germans to export their way out of balance sheet recessions by 2007-8.

..

Spain is already in a deflationary spiral and others are not too far behind.This crazy cycle of bubbles and balance sheet recessions in the Eurozone could have been avoided if the German government implemented necessary fiscal stimulus starting in 2000.

…

The 3 percent deficit rule is appropriate when the economy is not in balance sheet recession, but is highly disruptive if the economy is suffering from this disease.

While we are mostly in line with Koo’s arguments. But excessive fiscal spending for the German reunification let German public debt increase between 5% and 16% per year between 1991 and 1996. Running deficits at 5-6 % interest rates for 10 year bonds between 1996 and 2002 was for Germany too costly, given that real GDP rose around 0.5% per year (see details).

For us it wasn’t the dot com bubble, but the costs of the reunification and increased labor and housing supply from Eastern Germany that exercised downwards pressure on German wages and home prices. I well remember a story still in 2010: Some Poles work in Gdansk, Poland, but they live in Eastern Germany, where home prices were far cheaper than in that Polish town.

We judge that, given the restrictions of the euro zone, a balance sheet recession combined with a contraction of overvalued home prices and a correction of excessive wage increases in the periphery is healthy, as long as it does not end up in a deflationary spiral and ever-increasing unemployment.

Similarly to the German balance sheet recession from 1996 to 2005, countries like Italy that have a good local financial basis and not too much foreign debt, could recover after a couple of years. The story might be different for Greece and Spain that depend more on foreign capital. Still it is paramount that consumers in Germany enhance spending, given that they have received good pay rises in the last two years.

About Japan’s Abeconomics:

In Japan, the new governor of Bank of Japan Mr. Kuroda, who has no prior experience with monetary policy, is still clinging to the obsolete idea that additional bond purchases will somehow get the economic activity and inflation rates to pick up.

About the withdrawal of liquidity by central banks:

But once the private sector finishes repairing balance sheets and regains its appetite for borrowings, the central bank will be forced to remove the massive reserves in the banking system before both money supply and inflation go through the roof. The benefit of implementation QE and the cost of its removal are

not symmetrical because the two take place at different phases of the economy. At this juncture, a QE

of $200 billion or $2 trillion really does not make much difference because the money multiplier is dead in the water.

..

This time, however, the US and UK central banks are in the long end of the market. This means the removal of QE will have much larger effect at the long end of the yield curve, with equally larger impact on the economy just when the economy is regaining its health and willingness to borrow

[gview file=”https://snbchf.com/wp-content/uploads/2013/04/Koo-Ineffectiveness-Monetary-Expansion.pdf”]

(if the file does not show up in the PDF viewer, here the direct link)