George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

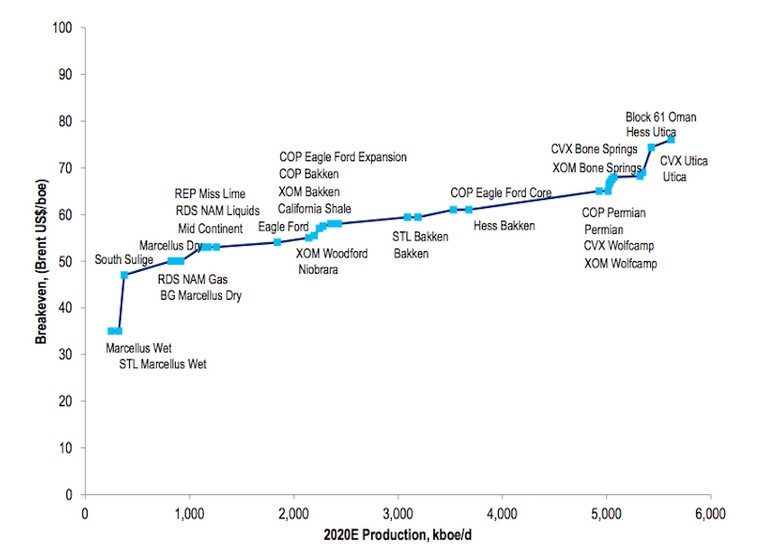

In this post we give a comparison of break-even prices for different shale oil fields given in the year 2014. They are only some fields, e.g. Marcellus, Utica, Missippian Horizontal, Eagle Ford – Liquids Rich, Niobrara – Wattenberg, Wolfcamp – N. Midland, Eagle Ford – Oil Window

where break-even prices are lower than 55$.

Global aspects:

We compared production costs for all global producers. It gives indications why 55$ for WTI and 60$ is the equilibrium price at a global scale.

Update January 06, 2015: As opposed to prices of 55$ for WTI and 60$ for Brent, current WTI prices under 50$ and Brent prices of 53$ are not sustainable because much of the shale oil will drop out of the market in some years. Less supply, however, will again translate in higher prices.

The consequence is here:

2014 Estimates for break-even price for the Shale Oil Industry

KLR GROUP (Oct. 22, 2014)

"The U.S. E&P industry needs (more than) $90 NYMEX, about $100 Brent, oil prices to maintain the current oil rig count of 1,500-1,600 rigs, which is intrinsic to our U.S. oil production outlook. A comparable NYMEX oil price is needed to maintain the projected pace of Canadian oil sands development."

MORNINGSTAR INC (Oct. 21, 2014)

"Our analysis suggests that the average breakeven for our

E&P coverage is $70 per barrel, well below our $90 per barrel

marginal cost and below today's $80 per barrel WTI (West Texas

Intermediate) oil price."

"Our estimate of the marginal cost for oil remains $90 per

barrel WTI and $100 per barrel Brent."

BERNSTEIN RESEARCH (Oct. 20, 2014)

“We estimate that about a third of U.S. shale oil production is uneconomic at $80 per barrel WTI. We disagree with other estimates, including those cited by the IEA, which suggest the vast majority of shale oil production is robust at such prices. Our expectation is that (the) oil price will revert back to a level where a much smaller portion of production is uneconomic.”

MORGAN STANLEY (Oct. 14, 2014)

UBS INVESTMENT RESEARCH (Oct. 14, 2014)

- BASIN BREAKEVEN OIL PRICE PER BARREL

- EAGLE FORD $43.34

- MIDLAND NORTH

- WOLFCAMP $52.56

- MIDLAND SOUTH WOLFCAMP $62.74

- DELAWARE BONE SPRING $64.67

- BAKKEN $65.06

- NIOBRARA $72.75

- DELAWARE WOLFCAMP $74.86

- UINTA-VERTICAL $78.16

- MISSISSIPIAN LIME $85.54

- DELAWARE AVALON $85.87

- ANADARKO BASIN $88.83

UTICA-HORIZONTAL $111.48

STIFEL, NICOLAUS & CO INC (Oct. 13, 2014)

“The weaker portions of several U.S. shale plays, or newer areas that are in the delineation phase and have not benefited from development drilling, require oil prices above $80 per barrel in order to generate a pretax internal rate of return of 20 percent, which is a reasonable threshold for most companies.”

WELLS FARGO SECURITIES (Oct. 13, 2014)

“If the crude oil market believes a price-driven market share war is under way and 2015 demand growth will be meaningfully lower than prior expectations, then our updated view is that U.S. onshore 2015 E&P budgets would need to be trimmed so as to moderate production growth relative to lower demand expectations. “In such an environment we estimate that WTI prices of $85-90 per barrel versus our current estimate of $96 per barrel would be required.”

GOLDMAN SACHS (Oct. 10, 2014)

BASINS BREAKEVEN OIL PRICE PER BARREL

BAKKEN CORE, $70-$80

PERMIAN DELAWARE, UTICA, EAGLE FORD OIL & $80-$90

WET GAS BAKKEN NON-CORE $90-$110

CREDIT SUISSE (Sept. 30)

- BASIN BREAKEVEN OIL PRICE PER BARREL

- Marcellus Shale – SW liquids rich $24.23

- Marcellus Shale – Super Rich $25.63

- Utica – Wet gas $32.39 Mississippian Horizontal –

- East $42.15

- Utica – Liquids Rich $44.04

- Eagle Ford – Liquids Rich $46.05

- Niobrara – Wattenberg $46.10

- Wolfcamp – N. Midland (Horizontal) $53.92

- Eagle Ford – Oil Window $55.29

- Wolfcamp – S. Midland (Horizontal) $61.57

- Mississippian Horizontal – West $64.05

- Wolfberry $64.63 Bakken Shale $64.74

- Wolfcamp – N. Delaware (Horizontal) $68.54

- Uinta – Green River $68.77

- Uinta – Wasatch (H) $72.15

- Granite Wash – Liquids Rich $73.10

- Horizontal Uinta – Wasatch (V) $74.95

- Barnett Shale – Southern Liquids $84.45

Shale Oil: Market Price Compared to Production Costs

Nov 28, 2014: Citi comes with the following break-even overview for US shale oil. The question remains if this data reflects “marginal costs”, the costs for additional supply and the depletion of existing fields. Our table based on Natixis above was more concentrated on “marginal costs”. Citi thinks that the US shale production may be sustainable at 70$, and on a shorter term basis at even lower prices (via business insider). If however the price remains around 55$ for longer, then all those shale companies will go bankrupt.

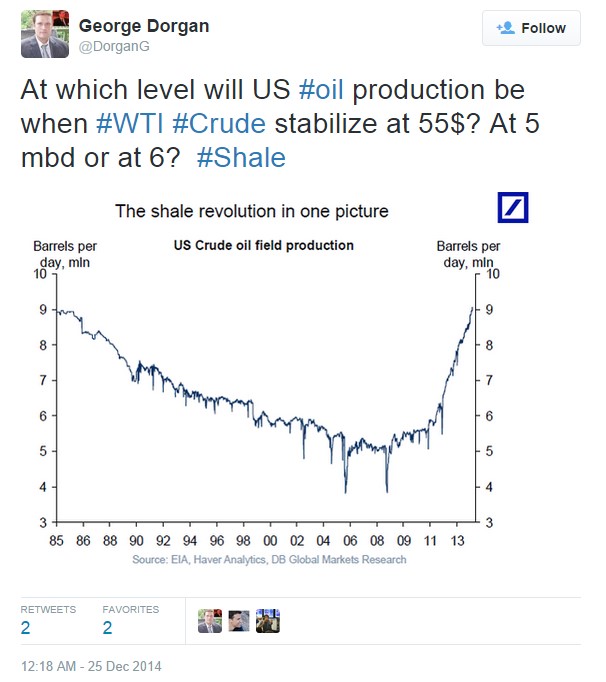

Economic #monopoly and #oligopoly theory sees #crude oil at 55$-60$ for years or even a decade #OPEC #genius #shale pic.twitter.com/2JXxlcbDmE

— George Dorgan (@DorganG) December 23, 2014 Further discussion on shale oil break-evens that includes different sources on the bottom

Further discussion on shale oil break-evens that includes different sources on the bottom

On the profitability of Shale oil companies

Again via Seeking Alpha

Transport costs, Keystone XL pipeline and Canadian Sand/Tar Oil

Oil production costs based on oil sands on Canada’s Alberta seem to be higher than market prices. One major issue is the high transport cost to refineries, even if the Keystone XL pipeline is built, 18$ per barrel to convert the heavy oil and to reach the not yet existing pipeline and about 30$ total transport costs by train.

Reducing the Brent-WTI spread seems to be an obvious idea via oil arbitrage, still it seems to be difficult.

TransCanada Corp. (TRP) said it will start a pipeline to Texas from Oklahoma next month, therefore the spread between WTI and Brent could tighten. (Source Bloomberg)

Update November 2013

A new study (PDF) examining the economics of Western Canada’s oil sands finds that even if the Keystone XL pipeline gets built, it’s unlikely that extracting the heavy, tar-like oil around Alberta will remain commercially viable over the next decade.

The report, written by two former Deutsche Bank (DB) analysts and titled Keystone XL Pipeline: A Potential Mirage for Oil-Sands Investors, calculates that producers in Western Canada will need to fetch at least $65 a barrel to attract new investments and ensure that current projects remain profitable. During the past month a barrel of Western Canadian Select (WCS), the main benchmark used to price Canada’s heavy oil, has averaged just $58.

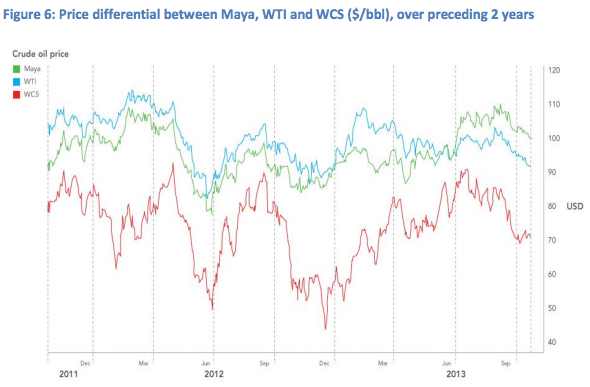

Data compiled by Bloomberg. Western Canadian Select is trading at a huge discount to its Mexican Maya rival (source)

New data for Canadian sands oil production costs come from Christoph Aublinger on Seeking Alpha.

Transport costs for Canada’s oil sands:

A few forces are at play. Canada’s heavy crude is already among the most expensive to produce in the world. But it’s also stuck. While that’s partly a function of the crude’s physical attributes (it’s heavy and thick and hard to move), the biggest problem is that there are simply not enough pipelines to transport it thousands of miles out of Western Canada and down to U.S. refiners. As a result, much of the oil is finding its way out of Alberta on trains and even trucks, which can be two or three times more expensive than sticking it into a pipeline. Those extra transportation costs push down the price at the well.

The real value of the Keystone XL is that it would deliver oil-sands crude down to the Gulf Coast, where it could compete with Mexican crude priced against the Maya benchmark. Heavy Mexican oil enjoys a $20 premium over its Canadian rival and is trading at about $87 a barrel. Even if the Keystone XL gets approved, just getting Canada’s crude down to the Gulf is barely enough to make it worthwhile. Mark Lewis, one of the new Keystone report’s co-authors, estimates that between the transport costs and the extra lubricants needed to coax the oil through thousands of miles of pipeline, it would cost about $18 a barrel to get that tar-sand crude from Western Canada down to the Gulf Coast on the Keystone XL.

(source)

Transport costs for Shale Oil, North Dakota

Prices at the Clearbrook, a junction for pipelines heading to the Midwest and Gulf Coast, offer a rough gauge, but do not always reflect producers’ financial reality.

Some can fetch $10 a barrel more by shipping it by rail, a costlier mode of transportation but one that avoids the glut at Clearbrook and delivers oil to premium markets on the East and West coasts, where crude prices tend to be based on the Brent benchmark, some $25 a barrel dearer at current prices.

Over 60 percent of Bakken crude, some 560,000 bpd, is shipped by rail. While narrowing U.S. crude spreads have made such trades less profitable in recent months, producers can still get a higher price by simply avoiding Clearbrook. (source)

Depletion and technological barrels

Shale’s Effect on Oil Supply Is Forecast to End in 2020

“There is a huge growth in light tight oil, that it will peak around 2020, and then it will plateau,” said Maria van der Hoeven, executive director of the International Energy Agency. (source)

About Net Energy and Energy Returns

Pennsylvania oil 19th century : 1000 :1

West Texas 1960s: 100:1

Saudi-Arabia Today: 30:1

Oil Sands Canada: 4:1

by ian807 » Fri 28 Sep 2012, 17:01:15

The fact of the matter is that oil shale or not, we’re in a position of running as hard as we can just to stay in place. Remember, it’s all about net energy. If you’re not getting more energy from the oil, than it takes to extract the oil, what’s the point? And you have to get a lot more. It has to be enough to support extraction, refining and distribution PLUS the economic activities for which it’s intended, mostly transportation.The first Pennsylvania oil wells were getting estimated energy returns of 1000:1. In West Texas in the 1960s, estimates ran to 100:1. These days, even the Saudi’s are only getting estimates of 30:1 and oil sands in Canada have nice low returns of 4:1. Bottom line?The total net energy in first half of the conventional oil (energy return x quantity) was much greater than the total net energy remaining in the second half of the conventional oil. Imagine a battery that lasted 10 hours, but on the first hour, you got 1000 watts, the 5th hour, you got 100 watts, and at the 10th hour, you’re pulling barely a watt. That’s roughly analogous to our situation with oil. The oil is there, for sure, but we got the high net energy stuff first (i.e. light sweet crude, close to the surface). What’s left is, for lack of a better word, crud. Yes, we can get it. Yes, it’ll work, but it just takes more energy to get it out and refined than it used to, increasing the price and decreasing the utility forevermore. There will be price fluctuations as with any commodity, but the long term price trend-line goes up from here on out.

Depletion: Bakken region in Montana 40% dropped in production, will in Bakken- North Dakota happen the same?

ODAC newsletter wrote:

Worse could be yet to come as meaningful historical drilling data begins to emerge from more mature regions. According to Bob Brackett, an analyst with Bernstein Research, production from shale oil in the Bakken region of Montana has seen a 40% drop in production since 2006, this despite increased investment and technological improvements. He puts the decrease down to the fact that not all shale oil plays are equal — inevitably the best areas are drilled first — and anticipates the same curve will occur in the much vaunted Bakken play in North Dakota. There have of course been warnings, not least by Art Berman, and Ian Urbina at the NYT, but the popular narrative remains one of abundance.

Shale gas: ‘The dotcom bubble of our times’

We now have more than enough data to know what has really happened in America. Shale has been hyped (“Saudi America”) and investors have poured hundreds of billions of dollars into the shale sector. If you invest this much, you get a lot of wells, even though shale wells cost about twice as much as ordinary ones.

If a huge number of wells come on stream in a short time, you get a lot of initial production. This is exactly what has happened in the US.

The key word here, though, is “initial”. The big snag with shale wells is that output falls away very quickly indeed after production begins. Compared with “normal” oil and gas wells, where output typically decreases by 7pc-10pc annually, rates of decline for shale wells are dramatically worse. It is by no means unusual for production from each well to fall by 60pc or more in the first 12 months of operations alone.

Faced with such rates of decline, the only way to keep production rates up (and to keep investors on side) is to drill yet more wells. This puts operators on a “drilling treadmill”, which should worry local residents just as much as investors. Net cash flow from US shale has been negative year after year, and some of the industry’s biggest names have already walked away.

Costs rise for ‘technological barrels’ of oil

Sanford C. Bernstein, the Wall Street research company, calls the rapid increase in production costs “the dark side of the golden age of shale”. In a recent analysis, it estimates that non-Opec marginal cost of production rose last year to $104.5 a barrel, up more than 13 per cent from $92.3 a barrel in 2011.

The big increase will have implications both for the market and oil companies, helping to put a floor to energy prices but also capping the profitability of the sector.

At the epicentre of the shale revolution is the US, and it represents a paradigm of the cost of technology. Sanford C. Bernstein found an “unprecedented” spike in the US oil marginal cost last year, jumping to $114 a barrel, up from $89 in 2011. via FT

Via Bloomberg and Peakoil.

Dream of U.S. Oil Independence Slams Against Shale Costs

Just a few of the roadblocks: Independent producers will spend $1.50 drilling this year for every dollar they get back.

Even with crude prices above $100 a barrel, U.S. independent producers will spend $1.50 drilling this year for every dollar they get back from selling oil and gas and will carry debt that is twice as much as annual earnings.

By contrast, the net debt of Exxon Mobil Corp., the world’s largest energy explorer by market value, is less than half of the cash earned from operations last year. The company will spend 68 cents for every dollar it gets back this year.

“There is a point at which investors become worried about debt levels and how that spending is going to be financed,” Oatman said. “How do you accelerate and drill without making investors worried about the balance sheet? That’s the key tension in this industry.”

More Sources on Shale Oil Prices and Hedging against Falling Prices

“The author also predicted a maximum level of production of US shale oil of around 0.7 Mb/d.”

In the following some about price and daily capacity for Shale oil from a forum discussion. Original source

Pressure pumping prices, which cover a range of costs associated with fracking a well, have already dipped by up to 25 percent in natural gas-rich basins, with signs of a knock-on effect emerging in the Bakken, according to Barclays analysts. Within the next six months, these costs could fall by as much as 10 percent in the Bakken shale, analysts at Bernstein Research estimate. Efficient forms of fracking are also helping companies extract more oil from each well, lowering the break-even cost of production, now estimated between $55 and $70 a barrel. (source)

Wood Mackenzie has an overall Bakken break-even price of $62 a barrel at current well costs, Garrett said. But for high-quality parts of the formation such as the Parshall and Sanish fields, that number goes down to the $38-$40 range. (source)

Bakken Capacity 0.7 Mb/d.: The Bakken Shale Oil would just enough to Cover the Additional Chinese Demand in 2013 compared to 2012

November 2013:

North Dakota crude oil prices tumbled this month to below the $80-a-barrel “sweet spot” that helps drillers attract capital from other shale areas, yet the Bakken boom shows no signs of slowing.Even though prices have slumped to their lowest in more than a year, output keeps marching ahead thanks to falling operational costs, increasingly efficient well technology, rising reserve estimates and aggressive forward hedging programs. Experts say the 1 million barrel per day (bpd) mark will probably be reached by early next year.Local cash prices, which have fallen some $25 a barrel in the past two months, would have to suffer a sustained decline to $70 a barrel or lower to jeopardize near-term spending, analysts said, a prospect most deem unlikely for the moment….

Hedging

For example, Kodiak Oil and Gas Corp (KOG.N) has hedged about half of its 2014 production at about $93 per barrel, far above current prices. Executives said they expect to add to the hedging position going into the new year.

BAKKEN BREAK-EVEN

With savings, improved production rates and hedging, the break-even point is still a way off by most accounts.

But formulating a break-even price is no simple matter and analysts differ in their calculations as the more than 100 operators in the Bakken have different costs, access to acreage of varying quality and distinct success rates in producing oil.

“We’ve seen tremendous variability in cost and well performance between operators as each tests different methods of well completion,” said Jonathan Garrett, analyst at Wood Mackenzie.

(source)

Bakken crude for June delivery at the Clearbrook, Minnesota hub was bid as low as $85.24 a barrel on Wednesday and offered at $93.69, down 6.5 percent from October levels, according to traders. For now, prices are comfortably above the $68 a barrel breakeven point for a 15 percent rate of return, according to Credit Suisse analysis.

Further sources

The wells here, which use the hydraulic fracturing or “hydro-fracking” technology, cost about $8.5 million on average to drill and complete, with break-even pricing linked to market prices at $55 to $70 per barrel. (source)

Of the 20 shale oil plays Freeman looked at (he excluded the Utica and the Tuscaloosa Marine Shale for lack of data), only Oklahoma’s Cana Woodford rich gas shale and the Cleveland-Tonkowa in the Texas Panhandle and Oklahoma don’t break even at $65/b WTI, although they do at current prices.The other 18 earn even some minimal return at $65/b WTI, and some, notably South Texas’ Eagle Ford oil and condensate shales, earn quite a bit, breaking even at under $50/b WTI. (source Platts Oil)

“Our Bakken shale portfolio” a representative for Statoil says, “competes very well with the average of projects across the [onshore North America] group, which would have a breakeven price of about $50-$60 per barrel.” (source)

Rock, you constantly put down Art Berman, the OilDrum and even little ole’ me. It gets tiring. I am not a geologist, never claim to be, and have in fact learned a great deal from professionals like you, but especially over at the oildrum. Why don’t you take you virulent attacks over there and instead lighten up on the amateurs here. It is not attractive of you.

Perhaps if you quit making claims that are completely wrong with an air of authority? If you’re an amateur then don’t pretend to have knowledge you don’t. I do not “put down” Art Berman (I’ve actually met him and listened to his arguments with a few executive at a small table), what I do point out is his database isn’t anywhere near what the industry works with which limits the veracity of his claims.

1 comments

tom notaspeculator

2015-09-12 at 23:35 (UTC 2) Link to this comment

hello:

i am having a very difficult time trying to determine what is the breKeven PRICE FOR THE OIL DRILLER IN BAKEEN WLL , EOG, l especially small caps eox,HK,and in permian basin like fang pe etc , EAGLE FORD AND THE NAT GAS PLAYS IA WITH SUCH MHR, chk etc.

i know most have cut their capex but i don’t how to use the income statement and the cashlow statements to find the profit or loss these compies are incurring in each of the plays to get to profitabilty when oil was say at 80 THEN AS IT HAS FALLEN TO 70 ETC AND NOW AT 45. ALSO WHEN NAT GAS WAS $4 AND IS NOW 2.70 OR SO

THERE MUST BE A SIMPLE WAS to do this and there must be examples on how to do but how you did this using the numbers and the formulas if any.

‘ i have searched the net and can’t find any examples that show how it is done. i kow cutting cPEX OR JUST CAPEX SPENDING IS ONE KEY BUT I DON’T KNOW HOW TO USE IT AS I AM ONLY INFORMED ABOUT ABOUT PE’S AND DON’T USING CFLO HOW TO DETerMINE WHICH ARE PROFITABLE AS Well which are more expensive than its rivals.

rganks for your help

i have seen huge cuts in capex but can’t use it .

i have a hand injury so i apologize for my typing as i can not make corrections as i have severe limitations and typing this is very difficult.

if you have examples about how this is done or can reer me to sites where it shows how it is done sorta step by step i would be greatly appreciative

if there are web sites that are helpful to me please include those as well but i am almost ertain that your re[rentations ND examples will do the job well.

thanks

tom

simply i would like to determine profititability as you have done so well in your article

i have included what i think are profitable com[panies and small companies which i think are struggling in each of the oil areas thinking that texas has fa tors that bakeen does not and small caps have financial issues that are different from those small cap in the same play

would you send me a few examples how you arrived at the breakeven prices ..sorta like a step by step where you plug in the figures in eCH [LAY FOR

Simply what i would like to do is your figures and reach the the breakeven price points as the gas and oil price changes in each of the 3 plays and for the large cap vs the smALL CAP IN EACH PLAY AS I THINK THE COMPANIES IN THE SAME PLAY HAVE DIFFERENT FACTORS SMALL CAP VS LARGECAP.I

thanks for your help

tom