George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

| The EUR/CHF collapsed after the monetary assessment meeting of the Swiss National Bank. Last week, the EUR/CHF rose when the ECB was less dovish than expected. Now the EUR/CHF went lower again, because the SNB did not fulfill the wishes of currency traders with a more dovish policy, i.e. with lower rates or the thread of stronger interventions.

If the Swiss franc is really overvalued, remains questionable, given that

From the Press Release |

EUR/CHF - Euro Swiss Franc, March 16(see more posts on EUR/CHF, ) Source: Investing.com - Click to enlarge |

|

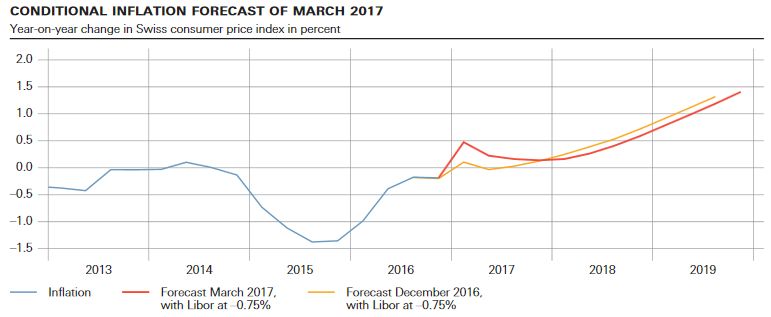

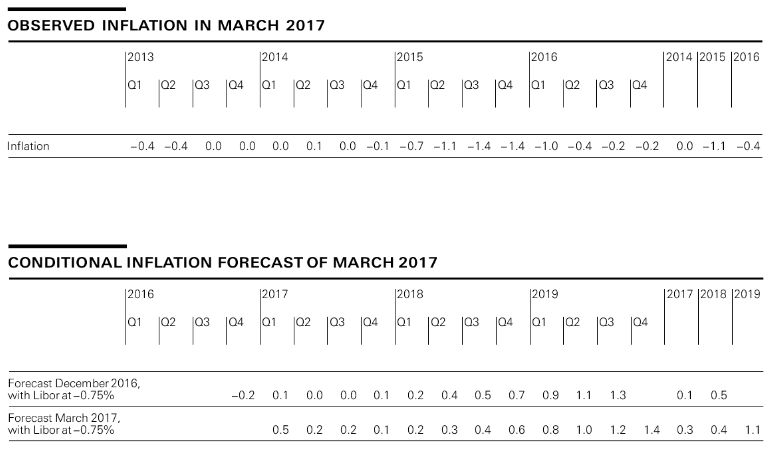

Conditional Inflation Forecast, March 2017 - Click to enlarge |

|

Observed Inflation, March 2017 - Click to enlarge |

George Dorgan (penname) predicted the end of the EUR/CHF peg at the CFA Society and at many occasions on SeekingAlpha.com and on this blog. Several Swiss and international financial advisors support the site. These firms aim to deliver independent advice from the often misleading mainstream of banks and asset managers.

George is FinTech entrepreneur, financial author and alternative economist. He speak seven languages fluently.

Tags: Monetary Policy,newslettersent