George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

We think that Italy, other peripheral economies and also France will follow Japan for a decade or more of balance sheet recession: stagnant wages, falling real estate prices and a reduction of private debt. On one side, we reckon that this might not be so bad because it will help exports and competitiveness, but still it will be a very hard time. On the other side, we suggest that the weak member states should use the current dis- and deflationary environment and high risk appetite to exit the euro zone. This time financial markets could even welcome the end of the euro zone in its current form.

Traders were happy on Thursday with the ECB rate cut until Draghi spoke about negative rates. What does it mean? Markets simply love monetary expansion and rate cuts, just not for too long!

European Leaders Want the Balance Sheet Recession. Is it really so Bad? Do Markets like it?

Our readers might have realized that our opinion is somewhere in between Richard Koo’s balance sheet recession – and the libertarian “let the bubble deflate” theory (see also Steve Keen’s debt deflation), as long as countries are not heading for a deflationary spiral.

We judge that the Western hemisphere will go for further years of balance sheet recession. On the other side, the Fed does everything to inflate another bubble so that markets do forget and people might forget the crisis. They want rational expectations to change with time. In a recent post Tim Duy explained that the Fed is right – for now.

We reckon that Italy and France will possibly go the Japanese way of a balance sheet recession, while a deflationary spiral is threatening Spain.

The reasons:

Due to the strong German economy and the limitations of the euro zone, European leaders want lower wages, higher exports and more competitiveness. This, however, implies disinflation and even deflation.

We call the policy of European leaders a deliberate balance sheet recession: Southern European real estate prices are falling ; lower wages and high unemployment will induce further price weakness combined with a reduction of debt. Lower rents and real asset write-downs on company balance sheets might end up in even more deflation.

The following graph from Richard Koo shows that the price contraction in Spain, Greece and Ireland is far from over.

Price contraction is not finished in Italy either, whereas in the 1980s and 1990s families protected themselves against high Italian inflation with their own home(s). Furthermore, purchasing a home helped to bring undeclared funds into a safe haven. Last but not least, it helped against strange rental contract laws in the middle between over-regulation and weak protection for tenants. This caused a real estate bubble and a housing oversupply, especially outside of Italian city centers; the situation in Spain is notably far worse. With low inflation expectations and years of weak inflation or even deflation ahead, things will change, housing will lose its inflation protection function, just like in Japan.

Price contraction is not finished in Italy either, whereas in the 1980s and 1990s families protected themselves against high Italian inflation with their own home(s). Furthermore, purchasing a home helped to bring undeclared funds into a safe haven. Last but not least, it helped against strange rental contract laws in the middle between over-regulation and weak protection for tenants. This caused a real estate bubble and a housing oversupply, especially outside of Italian city centers; the situation in Spain is notably far worse. With low inflation expectations and years of weak inflation or even deflation ahead, things will change, housing will lose its inflation protection function, just like in Japan.

And what we have learned from Richard Koo: only fiscal spending helps against a balance sheet recession, therefore all fiscal targets of France, Italy , Spain, etc. will get postponed year for year, for at least a decade.

Lower growth in emerging markets has weakened oil prices and inflation considerably, while the Fed “printed” higher risk appetite and consumer spending. These two developments helped to lower Italian and Spanish government bond yields. Stock prices went up, especially for Italian banks. [By the way, forget what Draghi is telling you: if the Fed didn’t print in September, Europe would be in a big mess.]

Italy will follow Japan for decade(s) of balance sheet recession. There is one mean to avoid it. The periphery should use current positive market sentiments and low inflation to exit the euro zone. - Click to enlarge

As seen above, markets do not like balance sheet recessions and deflation, they love monetary expansion, they want to realize steroid profits.

Markets hate long-lasting balance sheet recessions, they love monetary expansion

The alternative to a balance sheet recession could be the creation of a Northern Euro or a euro exit of weak member states. In the coming winter months seasonal risk aversion – the “sell in May effect” – will have vanished. Then it will be time for Italy or Spain to say good-bye to the euro zone.

We hope that by then Berlusconi and the Grillini will have taken over power; no issue: in Italy governments change every six months.

After some initial fears, markets will hail the euro exit. An Italian exit opens the way for Italian monetary expansion and the end of the balance sheet recession.

The Italian euro exit is the ultimate monetary/fiscal expansion, markets will love it

The main reason for Italy, Spain or Greece to join the euro was to avoid excessive inflation or even hyperinflation. In the inflationary environment of Summer/Autumn 2011, European leaders and the banking oligarchy removed the elected prime minister Berlusconi and replaced him with the ECB puppet Mario Monti who then implemented strong austerity.

In times of global disinflation combined with risk appetite, however, potential hyperinflation and even high debt is never an issue for markets.

We judge that UBS’s Paul Donevan’s claim that the Euro zone is a hotel California, is only valid during inflationary periods, effectively he wrote this paper in September 2011. His opinion was that a weak country is never able to leave; otherwise there would be a bank run, a collapse of the banking system, a default on euro-denominated debt, tariffs, protectionism and civil disorder.

But during dis- and deflationary periods that are combined with high risk appetite just like now, the euro zone might be a “hot-sheet hotel”, where central bankers do what they like: printing money and distributing it. For markets it does not matter if these monies are called “euros” , “New Peseta” or “New Lira” ; countries are able to join and leave the euro zone as they like.

Similarly as in Cyrus, capital controls could insure a relatively unexpected re-denomination of bank accounts and potentially government debt into these new national currencies and prevent a bank run. Markets might get very nervous but losses will be limited. We do not want into technical details which are beyond the scope of this article. Just to give one detail: Anybody from Italy, Spain, …. that possesses a bank account in a euro country like Germany, will be forced to re-denominate the account into his home currency at the exchange rate when the euro was created. This should eliminate the tail risk on Target2 balances, the capital flight.

In times of weak inflation even a euro exit would not end in sky-rocketing yields for the concerned government bonds.

In times of balance sheet recessions, markets love inflationary shocks, a thing that Wolfson price winners Jens Nordvig and Nick Firoozye still described as one of the highest risks during a euro exit. Market monetarists like Lars Christensen will hail the euro exit and Italian and Spanish Nominal GDP targeting and even better, strong NGDP expansion – computed in Lira and Peseta.

Yes, Berlusconi must obtain his printing press!

And markets will shout: “Yes yes, Silvio, we want fiscal spending too, please show us the helicopter money (the combination of fiscal and monetary expansion).

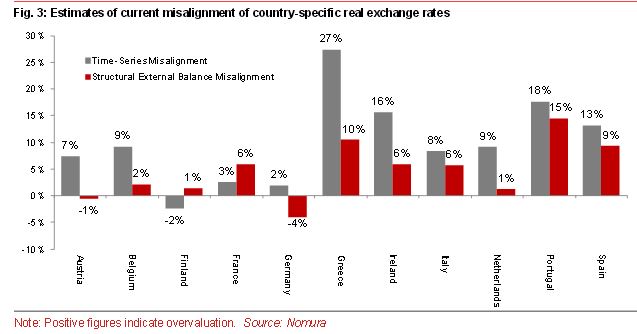

In a deflationary environment, new national currencies would not strongly devalue. The might adjust the fundamental misalignment, like e.g.

source Nomura’s Jens Nordvig and Nick Firoozye

We reckon that some time after the euro exit, inflation-adjusted Italian bond yields might be even lower than today. And Italian debt will be written off by inflation and not inflated by deflation.

The ECB has recently proven that especially Italian investors and households have deep pockets. As long as the euro exists, many of these Italians prefer to invest in Germany. When Italy leaves the euro zone, however, Italian exporters and stocks will become interesting and finally Germans will buy more Italian products.

Thanks to inflation, Italian and Spanish home prices will rise again – denominated in New Lira and New Peseta. Italians will use houses again to protect themselves against inflation. Germans will buy sunny housing bargains converting their expensive (German/Northern) euros into cheap New Lira and New Peseta.

In their hunt of high yields, markets might even love the relatively high Italian interest rates and they might buy the New Lira bonds, similarly as they purchase Australian or New Zealand dollars and certainly Rwanda debt now.

Last week it was Rwanda issuing USD-denominated debt at 7% (lower than Spain yields less than a year ago) just as bond yields of 90% of global sovereign bonds are at or near all time lows. And now, moments ago, we just learned that Ghana (nominal 2013 GDP: $42.8 billion) has just upsized its dollar-denominated $750MM bond issue to $1 billion.

We can only assume that this is due to unprecedented demand for yield. Any yield.

From Bloomberg:

“Ghana is inviting bids for advisers on transaction, according to information from two people with knowledge of the plans, who asked not to be identified because details aren’t yet public.

Govt plans to sell debt by end of yr: Albert Kofi Asamoa-Baah, an adviser at finance ministry, says by phone, declining to comment on size of offering.”

All will be happy: markets, Italians, Spaniards, Greeks because the troika and austerity will be gone; German consumers, because they will not need to finance the “lazy South” any more; and certainly the Bundesbank: the stronger (Northern/German) euro will remove all German inflation fears. And the Swiss SNB will make a huge bargain with all her German bond holdings.

With the end of the euro zone in its current form, all risk aversion will be finished!

After a while US private equity funds and rich investors will no longer artificially sustain the US version of the balance sheet recession assisted by cheap Federal reserve credits. The investor caravan will move on, this time to Europe and profit on the sharp rise of consumer confidence and strong spending. Just some German exporters and their protector protectionist Mrs Merkel will not really like the (German/Northern) euro increase to US$1.80. According to her and her studies, the German GDP can only rise with high German savings and ever rising exports, but not with consumption. According to her, French and other Southern countries must remain in the balance sheet recession while Germans firms continue to take profit on the for them strongly undervalued euro with German surpluses again the US and even China.

With a euro at US$ 1.80, however, the US trade deficit will weaken considerably and the German surplus will shrink.

But then, excuse me, @beppegrillo :

:

With all that printed money, and some years passed, China and their German engineers and exporters will strongly expand again. German exporters will finally realize that not price but quality is their argument.

Oil prices and inflation will be sharply higher……. the US trade deficit will come back and…..

……hyperinflation for Italy and Spain.

.

1 comments

Joe

2013-05-04 at 20:28 (UTC 2) Link to this comment

Good old inflation: viva Botswana. Sorry Rwanda