George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Market participants have to confront a stark asymmetry. There are many ways to lose money, but there appears to be only three ways to make money. Nearly all strategies seem to come down to some variant of momentum or trend following, mean reversion, and carry trades.

Trend Following

Foreign exchange traders use these virtuous and vicious circles to follow trends in foreign exchange markets. Elliott wave theory is a more sophisticated form of explaining these circles. Often FX traders and algos “overshoot”, they let an exchange rate rise or fall very strongly in a short period, so that exports and the current account balances of the concerned country are strongly affected over a longer view. The result is that currencies that overshoot need to perform a “trend inversion”, a trend in the opposite direction. FX traders never hold positions for a longer time, the closing of positions/profit taking accelerates the inverse trend. There is one exception to this rule, namely when FX traders are joined by carry traders that use big interest rate differentials and swap rates.

Overshooting: Trend Following May Distort Fundamental Data

FX trading can be thought of as similar to “groupon” deals, often traders follow a master, that indicates where the trend is going. Followers imitate the master’s strategy, even if FX rates get completely distorted from fundamental reality in a short period of time – I am not saying that you should not imitate this trend following strategy.

This is exactly what happened in July 2012, with the huge depreciation of the euro to 1.21 USD and in January/February 2012 with a strong appreciation to 1.36 and more. Thanks to reduced risk aversion and verbal Japanese government intervention, the euro rose from 97 to 129 yen in only 6 months. Japanese production costs are now 30% cheaper than German ones; big Japanese car makers are shifting from European to Japanese part producers. Lower car demand helps to intensify the European unemployment crisis.

While the Japanese take profits from lower production costs with deflation over many years, Germans see inflation and therefore higher costs (see more on the effect of inflation/deflation on productivity, the “real mean reversion“).

Fundamental data, especially current account balances, have not changed that much during these six months. The typical surplus and deficit countries remain the same. An inversion of credit cycles happens rarely, the latest inversions were the Lehman event in 2008 and possibly the recent upwards trend in U.S. housing. This inversion leads to completely different investor perceptions of risk, but is often corrected again by the reality of fundamentals.

Traders often have a short memories. They replicate recent developments into the future. One example is that in 1999 after the Asian crisis, everyone bet on a Japanese recovery. The yen was the strongest performing currency, even if the Japanese actually needed to still de-lever from their housing bubble for another 10 years or more.

The appreciation of the euro to 1.36 in January shows that traders remember the strong euro from the year 2011 that was driven by strong Chinese construction and investments as well as exports of German machines to China in the absence of European austerity.

Momentum Trades

Mean Reversion

Central Bank Interventions are based on mean reversion

The main SNB argument is Dornbusch’s “overshooting” model

During speculative attacks, currencies can get into strongly overvalued or undervalued territory. This was effectively the case in August/September 2011.

When the Swiss franc was severely strengthening, the SNB moved the real effective exchange rate from an 25% to a 13% overvaluation, recently this has come down to 11%. The EUR/CHF did not change a lot but other currencies fell.

UBS Real Effective Exchange Rate Franc

UBS'sExport-weighted exchange rate CHF - Click to enlarge

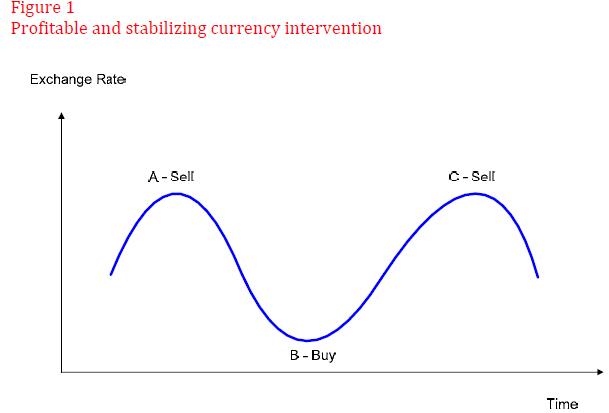

The RBNZ describes currency interventions based on mean reversion with

“An early contribution to the debate was Friedman’s ‘Profits Test’1 , which assumed central banks that were trying to minimise fluctuations in the exchange rate behaved like speculators when intervening. As a result, they tend to buy local currency / sell foreign currency the when exchange rate is low, to support the local currency, and sell local currency / buy foreign when the exchange rate is high to depreciate the local currency. The combination of ‘buying low and selling high’ implies that if the central bank succeeded in stabilising the exchange rate, then its operations would be profitable (Figure 1).

Carry Trades

- Friedman, M (1953) “The Case for Flexible Exchange Rates”, Essays on Positive Economics, University of Chicago Press [↩]