George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

The increasing volatility of SNB EarningsAnnual results are not really definite. Given that the SNB accumulates foreign currencies with interventions, they have huge swings. But the SNB may lose 50 billion in one year and win 60 billion in the next year or vice verse. Low Inflation, Crashes and Central Bank Money PrintingThe crisis caused by the Covid19 virus,is a typical crisis with low inflation (at least for now). During such a crisis, central bank money printing helps asset price to rise again. This applies to all assets on the SNB balance sheet:

The Corona crisis is just one of these low inflation crisis. Therefore SNB profits have recovered; this time far more quickly than during the Financial Crisis. As opposed to 2009 until early 2011, the Swiss Franc is currently not overvalued. Therefore the SNB did not let the Swiss franc appreciate. Without an a franc appreciation, however, the SNB must make profits during a period of central bank money printing. But a prolonged crisis, will again put pressure on SNB to let the franc appreciate. Franc will rise again with inflationWith a big rise of inflation, the run into the Swiss franc will start again. And this at an exchange rate that is not digestible for the SNB.

And this will lead to a massive SNB loss around 150 billion CHF. However, we are not there yet: Inflation is low and interest rates even lower. |

Some extracts from the official statement.

|

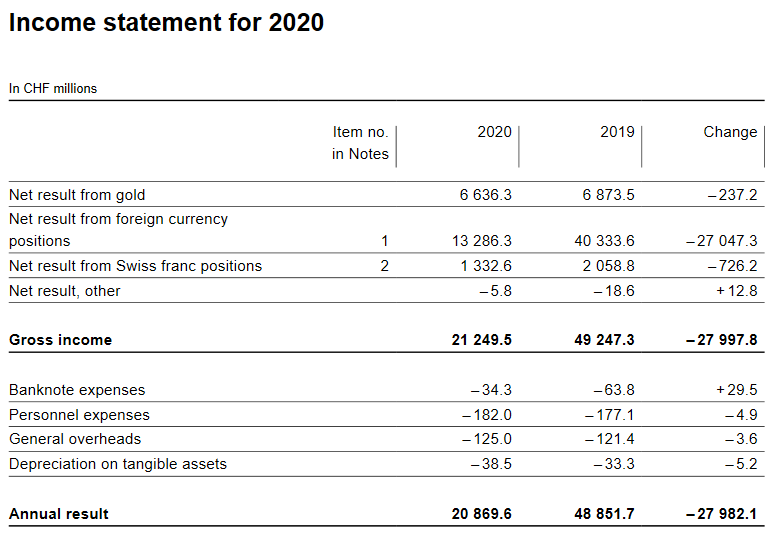

Income statement for 2020 Source: snb.ch - Click to enlarge |

||||||||||||||||||||||||||||||||||||||||||||||||||||

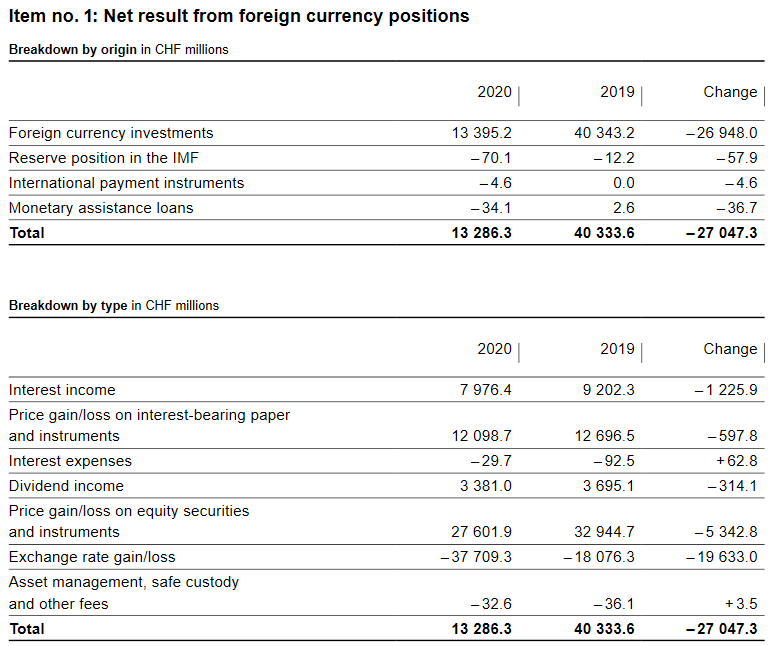

Profit on foreign currency positionThe profit on foreign currency positions was CHF 13.3 billion (2019: CHF 40.3 billion). Interest and dividend income totalled CHF 8.0 billion and CHF 3.4 billion respectively. A gain of CHF 12.1 billion was recorded on interest-bearing paper and instruments, while equity securities and instruments registered a gain of CHF 27.6 billion. Exchange rate-related losses totalled CHF 37.7 billion. The following numbers are in billion Swiss Francs.

|

SNB Profit on Foreign Currencies Source: snb.ch - Click to enlarge |

||||||||||||||||||||||||||||||||||||||||||||||||||||

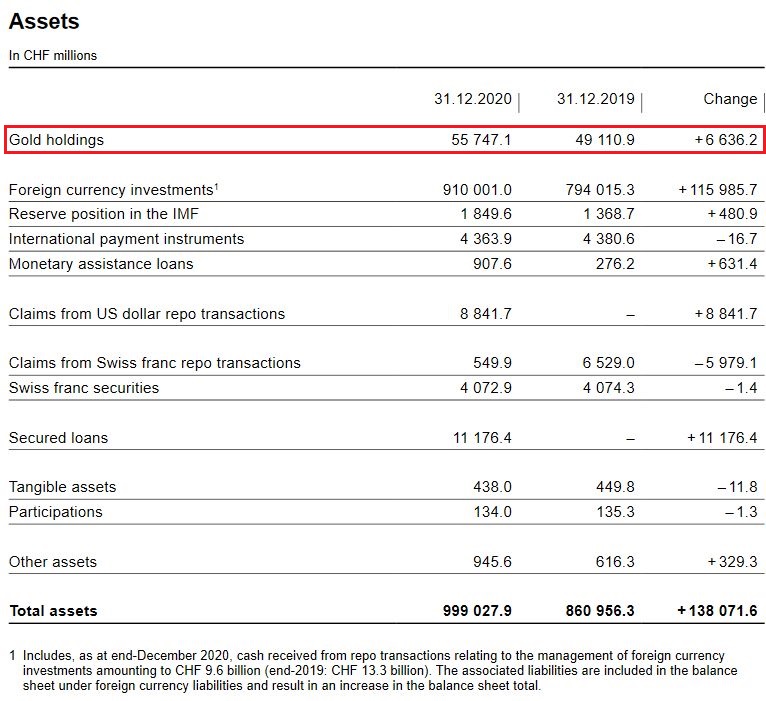

Valuation gain on gold holdings

Percentage of gold to balance sheetThe percentage of gold has risen to 5.58% thanks to higher prices.

Balance Sheet The balance sheet has expanded by 138.1 bn. francs, this is 16.04%.

|

SNB Balance Sheet for Gold Holdings for Q4 2020 - Click to enlarge |

||||||||||||||||||||||||||||||||||||||||||||||||||||

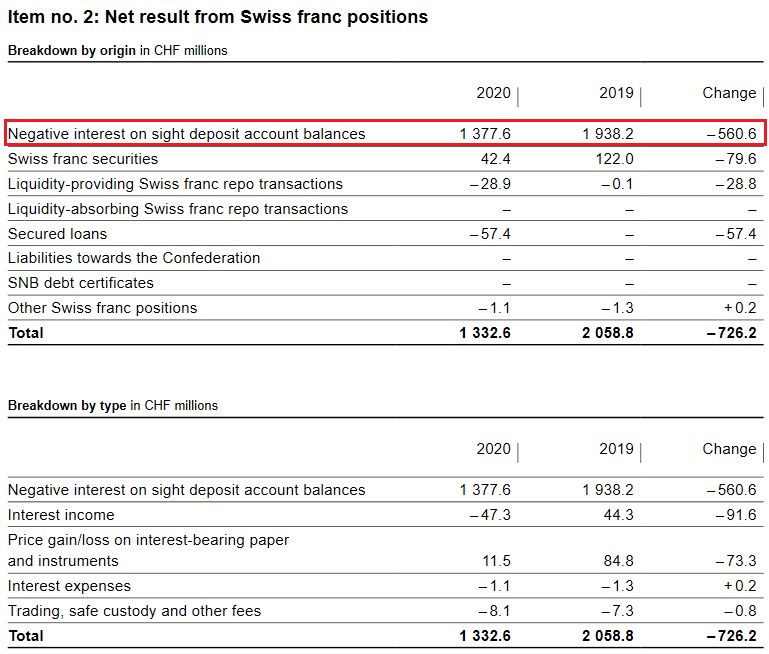

Profit on Swiss franc positionsThe SNB maintains its profitability, last but not least, thanks to the reduction of the profitability of banks. When too many funds arrive on their accounts, they must deposit them on their sight deposit account at the SNB.

Profit on Negative Interest ratesFurthermore, the SNB harms the Swiss economy, when it reduces the profits of Swiss banks by negative interest rates, currently -0.75%. But with this measure she maintains her own profitability. The SNB obtained far less money for negative rates, while sight deposits were slightly up (see below). The reason is this time the Corona crisis and that banks lend more money and did not put on the accounts of the central bank. Still, as compared to the FX profits or gains on equities and bonds above, this number is relatively low.

|

SNB Result for Swiss Franc Positions for Q4 2020 - Click to enlarge |

||||||||||||||||||||||||||||||||||||||||||||||||||||

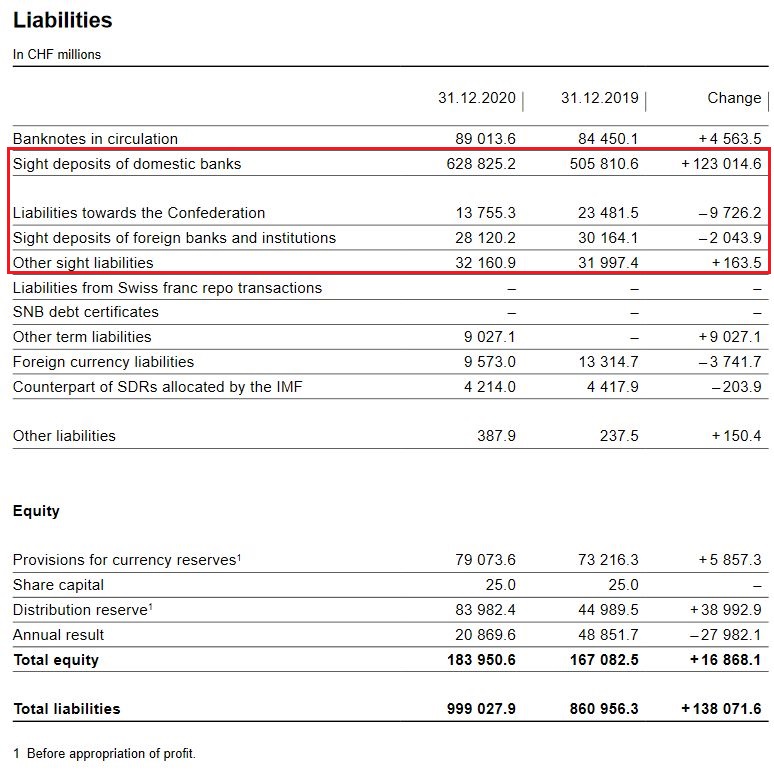

SNB LiabilitiesElectronic Money Printing: Sight Deposits Sight deposits is the biggest part of SNB interventions. Sight deposits increased more strongly (19%) than the total balance sheet. The increase was on domestic banks.

Paper PrintingBanknotes in circulation: +4.56 bn francs to 89.0 bn. CHF. This old form of a printing press, today a less important form of central bank interventions. It showed that safe-haven Swiss francs, e.g. 1000 franc bank notes are currently less in demand than previously. Increase in minimum allocation to provisions for currency reservesGiven the high market risks present in the SNB balance sheet, the percentage increase in provisions is generally calculated on the basis of double the average nominal GDP growth rate for the previous five years. In addition, a minimum annual allocation of 8% of the provisions at the end of the previous year had applied since 2016. In light of the significant increase in balance sheet risks since then, the minimum annual allocation has now been raised to 10% from 2020. This is aimed at ensuring that sufficient allocations are made to the provisions and the balance sheet is further strengthened, even in periods of low nominal GDP growth. Since nominal GDP growth over the last five years has averaged just 1.7%, the minimum allocation of 10% will thus be applied for the 2020 financial year. This corresponds to CHF 7.9 billion (2019: CHF 5.9 billion). As a result, the provisions for currency reserves will grow from CHF 79.1 billion to CHF 87.0 billion. |

SNB Liabilities and Sight Deposits for Q4 2020 - Click to enlarge |

Full story here Are you the author?

Tags: Featured,newsletter