George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

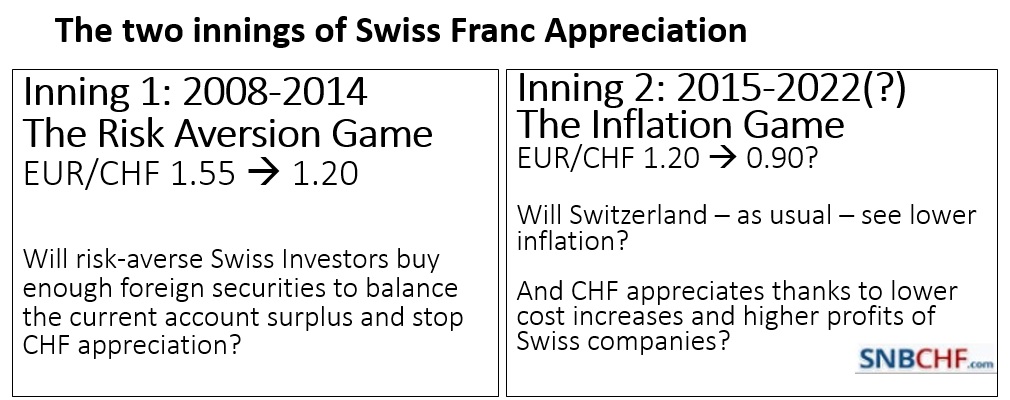

We show the two phases or two innings or phases of Swiss franc appreciation: The “risk aversion game” and the “inflation game”.

With the weakening of emerging markets and the strengthening of the United States in 2013/2014, the Swiss National Bank (SNB) had won the first battle in the war against financial market, the “risk aversion game“, the first innings in a two-part match. Risk aversion is lower because the United States recovered thanks to lower oil prices.

The “inflation game” started earlier than we expected, at least in the eyes of the Swiss National Bank, namely in January 2015. They anticipate higher inflation that will come with rising wages in the United States and Germany.

From a historic perspective (see the 1970s lessons here), the Swiss franc appreciated more during the inflation phases, thanks to lower inflation, when taken in comparison with the U.S. or Europe.

In the first inning the Swiss franc appreciated because of the financial and the euro crisis. Assets in Europe did not yield enough compared to the ones in Switzerland. Logically Swiss investors did not move enough money abroad to counter the strong Swiss trade surpluses. This blog explains the simple balance of payments mechanisms that requires a stronger Swiss franc.

The second inning will start when German and U.S. wage inflation reduce profits of German or American companies. Once again Swiss investors will keep their money in Switzerland. Rising wages in Germany will help to create demand for products of Swiss exporters, but reduce profits of German companies. Balance of payments and the Swiss franc will adjust accordingly.

As compared to Germans and Americans, the Swiss companies will keep wage hikes limited because they “import” qualified personnel or outsource activities. As we explain here, the main driver of a stronger CHF will be higher profits of CHF-denominated stocks.

During the “early nice inflation”, the euro may appreciate against CHF

Be aware that in between inning 1 and inning 2, during phases of relatively low inflation and hopes on American rate hikes, the euro may appreciate against CHF, a period we have just entered.

We know that thanks to global competition and cheap goods imported from Asia, the business cycles in our times take longer, hence the reader (or Marc Meyer here) should not expect high inflation and the collapse of the Swiss National Bank right at this moment.

But beware:

Everyone loves an early inflation. The effects at the beginning of an inflation are all good. There is steepened money expansion, rising government spending, increased government budget deficits, booming stock markets and spectacular general prosperity, all in the midst of temporarily stable prices. Everyone benefits, and no one pays. That is the early part of the cycle. In the later inflation, on the other hard, the effects are all bad.

Ronald H. Marcks

The SNB exited the peg because it feared inflation

The SNB decided to get fully prepared for the inflation battle and – due to ECB euro bashing and massive currency inflows – they ended the peg earlier than I predicted at the CFA Society.

The central bank allowed a strong CHF appreciation that will exercise sufficiently deflationary pressures on the Swiss economy, so that the inflation phase starts later.

The deflationary pressures inside the Swiss CPI will be external, similarly as they were before. They may have repercussions on the internal economy: Swiss wage increases may be slower than the current 0.8% per year. Exporters or banks have already introduced wage cuts. We are seeing this first stage of inflation currently in the United States, while 2013 was the transition period from strong growth in Emerging Markets to slow global, but stronger US growth.

Labor Strikes and Wage Hikes in Germany

(January 2015)

Strong wage inflation and labor strikes in Germany combined with potential ECB quantitative easing increases fears of financial repression in the euro zone. This causes renewed pressure on the SNB. For the first time for many months, the SNB had to intervene. The SNB had to combat Fed QE until the year 2013. For us the next battle against both European QE and rising inflation rates appears to be far more difficult.

Rising wages in the United States

Deutsche Bank’s Torsten Slok describes here the rising wage inflation in the United States. In particular the IT sector is concerned.

References:

The biggest nonsense came from Goldman Sachs, they expected the SNB to hike rates. They thought that this would not result in a stronger franc.

Goldman Sachs on FT Alphaville: When will the SNB end FX intervention and start raising rates?

2 comments

DragoM2M

2014-12-16 at 12:39 (UTC 2) Link to this comment

What do you think about current levels of yield on Swiss government bonds? The 50 year bond maturing in 2064 is now trading at a yield to maturity of less than 0.9%.

http://www.six-swiss-exchange.com/bonds/security_info_en.html?id=CH0224397007CHF4

GeorgeDorgan

2014-12-17 at 05:30 (UTC 2) Link to this comment

Low bond yields reflect two points:

1) Risk-off: Before the 2008 crisis, people increased their debt and reduced savings. Now this has become different, everybody seeks a safe-haven to preserve wealth. The Swiss investors do not risk to place their trade and current account surplus of 14% of GDP. This applies in particular to pension funds that buy such bonds.

2) Similar to the Czech Krona, the Chinese Yuan, currencies with strong current account surpluses and low inflation must appreciate over time. Hence despite low yields, you have will a currency gain. The Russian Ruble is collapsing because inflation is too high and cannot be slowed down, in particular when Russian oil income falls.

As explained here, CHF must appreciate thanks to lower inflation.

This is reflected in the interest rate parity.

https://snbchf.com/fx-theory/interest-rate-parity/