George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

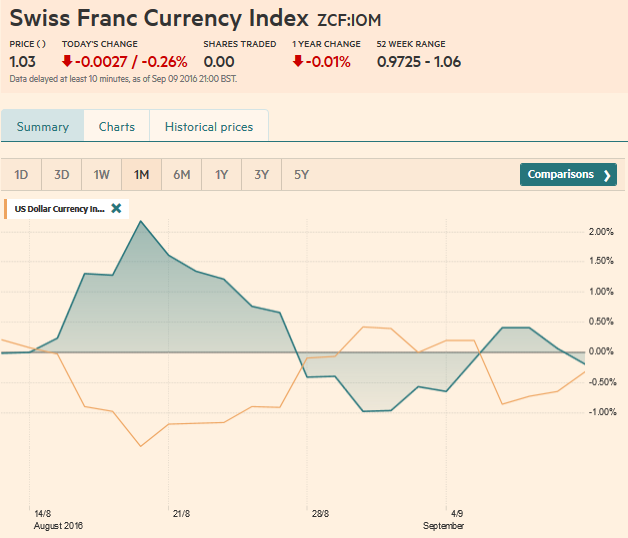

Swiss Franc Currency IndexThe Swiss Franc index remained mostly unchanged during the last week: Some gains against the dollar, but losses versus the euro. Since Tuesday the euro moved upwards against CHF. Given thatSwiss GDP was stronger than the one in the euro zone, this is surprising. But we must recognize that Draghi could be the reason. Inflation forecasts of 1.2% in 2017 and 1.8% in the euro zone would mean the ECB hikes rates maybe in 2018 or 2019. I personally do not believe it, given that wage inflation in Italy or Spain is clearly under 1%. This is lower than Swiss wage inflation of 0.8%.

|

Click to enlarge. |

|

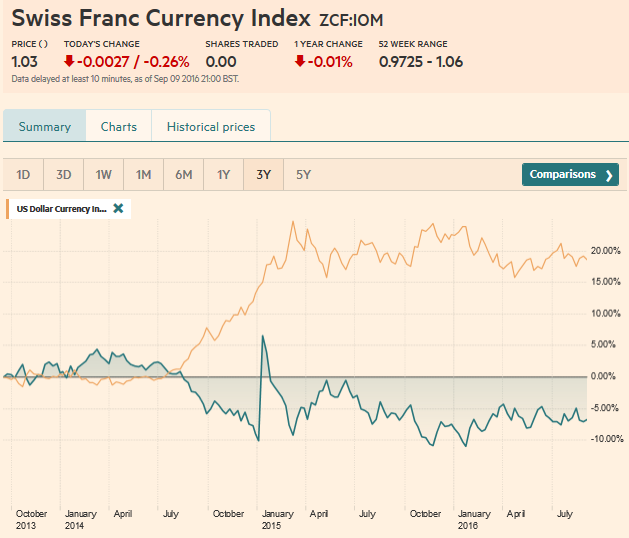

Swiss Franc Currency Index (3 years)The Swiss Franc index is the trade-weighted currency performance (see the currency basket)On a three years interval, the Swiss Franc had a weak performance. The dollar index was far stronger. The dollar makes up 33% of the SNB portfolio and 25% of Swiss exports (incl. countries like China or Arab countries that use the dollar for exchanges). Contrary to popular believe, the CHF index gained only 1.73% in 2015. It lost 9.52% in 2014, when the dollar (and yuan) strongly improved.

|

Swiss Franc Currency Index, Click to enlarge. |

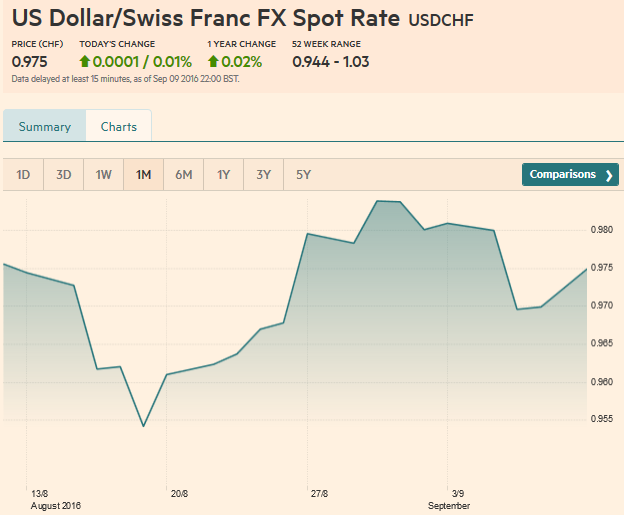

USD/CHF

|

USD/CHF Click to enlarge. |

US Dollar IndexThe US Dollar Index rebounded smartly off the trendline we have been monitoring. It is drawn off the May, June and August lows. It caught last week’s low of almost 94.45.

Rebounding before the weekend, it stalled in front of 95.60, nearly meeting a retracement level of the pullback that began at the start of the month. A move above 95.60 targets the 96.15-96.25 area that contains the August 31 high and the 200-day moving average.

Above there, the July high around 96.50 beckons.

|

USD Dollar Index, Click to enlarge. |

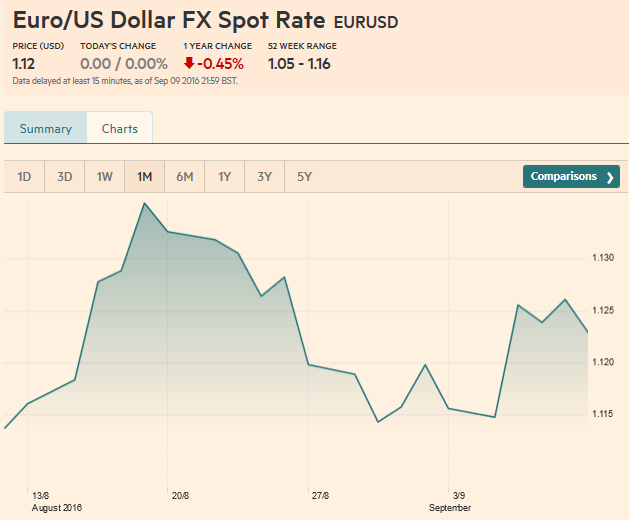

EUR/USDThe euro has fallen for the past four Fridays. It is an interesting pattern, but the significance is not clear. A break of $1.12 could spur slippage toward $1.1150-$1.1170, but we suspect the euro will be supported by caution ahead of Fed’s Brainard and what is expected to be a softer US retail sales report. On the upside, congestion around $1.1250 may hinder strong gains, especially given the proximity of the FOMC meeting.

|

EUR/USD, Click to enlarge. |

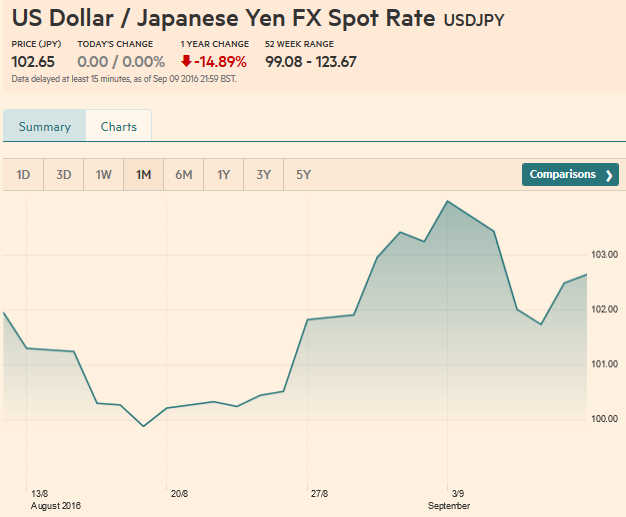

USD/JPYSimilar with the euro, the dollar has advanced against the yen for the past four Fridays. The next immediate target is the JPY103.15-JPY103.25 area, and then the recent high a little above JPY104.30. The technical tone though remains vulnerable. The MACDs may cross lower, while the Slow Stochastics have already turned. The sharp drop in US equities before the weekend will likely weigh on Asian shares at the start of the new week. The developments in the equity market may, in the first instance, hamper the dollar’s recovery against the yen. |

Click to enlarge. |

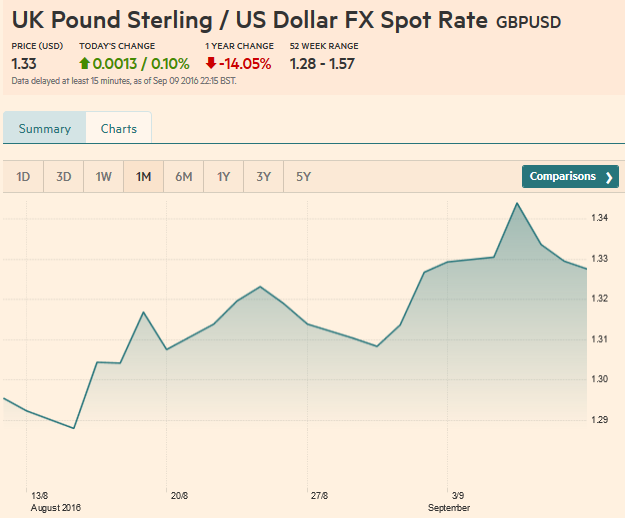

GBP/USD

|

Click to enlarge. |

AUD/USDThe technical tones of the Australian and Canadian dollars have deteriorated. The Aussie posted a key downside reversal on September 8 and saw follow-through selling before the weekend. The nearly two cent was the largest decline over two days since the UK referendum. Like the Canadian dollar, the Australian dollar’s RSI and MACDs warn of the risk of additional selling over the coming sessions. A break of the $0.7490-$0.7500 area is needed to boost confidence that a high of some import is in place.

|

Click to enlarge. |

USD/CADThe US dollar recovered off the midweek test on CAD1.28 and finished the week near CAD1.3050. The Canadian dollar’s pre-weekend loss of a little more than 0.8% was the largest loss in over month. It was sufficient to offset the gains it has registered earlier in the week. It closed the week with about a 0.4% decline, the most among the high income countries. The RSI and MACDs suggest additional losses are likely. The next objective is CAD1.3150. |

US Dollar - Canadian Dollar FX Rate(see more posts on Canadian Dollar, ) Click to enlarge. |

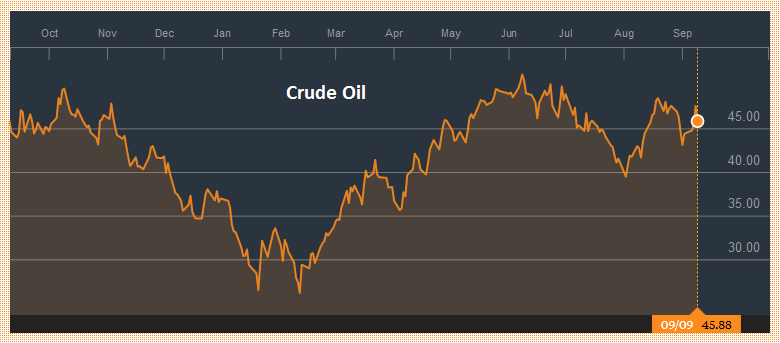

Crude Oil

|

Click to enlarge. |

US TreasuriesUS 10-year Treasury yields appear to be breaking out of the 1.50%-1.60%. It may take some time for participants to become convinced. If the range is broken, then the next important level is in the 1.70%-1.75%. Recall that as recently two months ago; the US 10-year yield was near 1.32%. It was around 1.66% ahead of the weekend. An important warning to the bears is that the technical readings seem stretched, and the fact that the December futures contract closed below its lower Bollinger Band may inject caution, especially ahead of Brainard speech and the US retail sales report.

|

Yield US Treasuries(see more posts on U.S. Treasuries, ) Click to enlarge. |

S&P 500 Index

|

Click to enlarge. |

Charts and CHF data added by George Dorgan and the snbchf team, Text Posted by Marc Chandler on Marc to Markets.

Are you the author?Tags: Australian Dollar,Canadian Dollar,Crude Oil,Dollar Index,EUR/CHF,EUR/USD,Euro,Japanese yen,MACDs Moving Average,newslettersent,S&P 500 Index,Swiss Franc Index,U.S. Treasuries,USD/CHF