George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

The same as every year in December/January: Swiss media and economists are doomsaying. This time they claim that the banking industry and the UBS job losses will bring Switzerland into trouble. Once again they do not understand that the Great Recession was only to a small part a banking crisis, but it was mostly a housing crisis that did not affect Switzerland at all. On the contrary, thanks to the recovery after the Great Recession, money flowed back into Switzerland and helped to boost the Swiss economy and housing.

Still in March 2012, the SECO spoke of a 3.7% unemployment rate for 2013, until this December they downgraded the number to 3.3%, clearly above the current seasonal adjusted number of 3.0%.

Once again media are claiming that some job losses will bring trouble: the financial sector in the canton of Zurich gives a yearly output of 30 billion CHF per yea, therefore less jobs in this sector would be a problem

Schadenfreude über Stellenabbau im Sektor nicht angebracht RT @retolipp: Finanzsektor im Kt. ZH erwirtschaftete Wertschöpfung von CHF 30 Mrd

— Roman Kappeler (@swissroman) January 11, 2013

But banking and insurance employs only 5% of Swiss employees and most of the lost jobs are not even in Switzerland.

Finance Minister Eveline Widmer-Schlumpf has made her first comments on Tuesday’s announcement by Swiss bank UBS that it would cut 10,000 jobs, 2,500 of which are in Switzerland.

UBS to cut up to 3,000 jobs in London

Axe falls swiftly as Swiss bank moves to halve City workforce in global cull of up to 10,000 jobs. Guardian

The Swiss economy is strong thanks to money inflows, an appreciation of real estate prices, huge current account surpluses, more well-qualified personnel since the bilateral agreements and consumer spending, all reflected in the so-called “strong franc”.

All this will outweigh some lost bankers. On the contrary, many of these (former investment) bankers will find a new job in the coming years, possibly in private banking, that will have a great future thanks to investors in search of safe-havens and countries with growth and safety.

Similarly, the Swissmem companies (machinery, electronics, metallurgy) should finally shed some jobs in Switzerland and not rely on the SNB subsidies with an artificially weak currency:

“There was a risk that a significant number of Swiss export companies would either have been wiped out or have had to leave Switzerland.” WSJ.

(Interestingly he is saying “was” and not “is”.) These people will find a new employment somewhere else. But with the potential SNB losses of 60-80 billion francs, the Swiss could create jobs for twice the size of the Zurich financial sectors’ yearly GDP contribution.

Swissmem was one of the main contributors to regular SNB surveys about how the strong franc affected their business and managed to manipulate the thinking of the central bank.

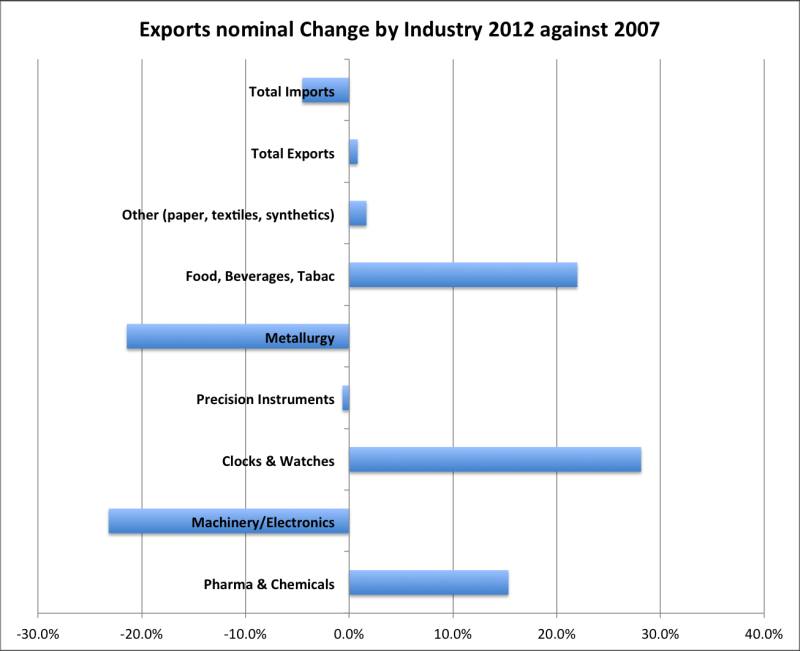

According to the Ricardian principle, the Swiss population should do what they are best at. This is shown via this chart, based on the ever increasing Swiss trade balance, compared to 2007, when the franc was very weak.

Swiss exports by industry since 2007 (source SNBCHF)

It is not the job of a central bank to subsidize a certain group of exporters, but to prevent a real estate bubble and future price inflation, even at a moment when inflation is not visible yet. Sooner or later it will come – see details when.

That would have been the first case in history that a country with low debt, strongly rising but not overvalued real estate prices, huge current account surpluses, solid consumer spending and quite high inflation expectations due to rising house prices goes into a deflationary spiral.

We think that especially one country in the European periphery is a far stronger candidate for a deflationary spiral, see which one.

But despite of all, the real responsible in the SNB was not Jordan, but they were Jean-Pierre Roth and Philip Hildebrandt. Read “Because They Knew What They Were Doing: The Parallels between European and SNB Leaders”

Are you the author?

Tags: Deflationary Spiral,jobs,SECO,Swiss economy,Swiss National Bank,Swissmem,Switzerland,Switzerland Trade Balance,UBS