George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

In the following we present the drivers of Swiss price inflation. We first show the components of the consumer price index. Then we explain which of them are upwards-drivers of inflation and which cause a downwards adjustment.

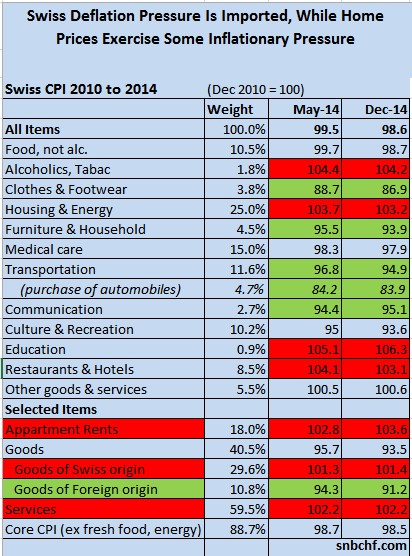

Swiss Consumer Price IndexThe following are the details of May and December 2014 for the Swiss consumer price index (CPI) on a December 2010 basis of 100. Imported goods like clothes and footwear, furniture and household articles, cars (inside “transportation”) and holiday packages (inside “culture and recreation”) have seen price reductions, thanks to the stronger franc – see the concerned CPI categories in a green color below. Prices of services, energy, housing and locally produced goods, visible in the red color, have increased in recent years. |

Swiss CPI December 2014(see more posts on Switzerland Consumer Price Index, ) - Click to enlarge |

2010 consumer price index based on 2005The following table from the November 2010 consumer price index shows that many of the green components, mostly imported goods, saw stronger price increases between 2005 and 2010: Imported goods showed price increases until 2010:

But also the internal price drivers:

|

Swiss CPI November 2010 (indexed to 2005 levels) - Click to enlarge |

Downwards drivers of Swiss consumer prices

There are many factors that still continue to drive Swiss consumer prices downwards.

1) Slow price adaptation for imported goods

Imports make up 26.5% of the Swiss consumer price index (CPI). Apart from energy, the main items are clothes, foot ware, package holidays, cars, furniture and household articles. According to analysis of the Swiss price monitoring agency (page 4), import prices require up to one year to reflect 40% of the foreign exchange rate. The main reasons are the following:

- Transfer prices for imported goods only adjust gradually and multi-national firms try to keep higher profits in Switzerland in order to pay lower taxes. Swiss retailers like Migros and Coop are often bound to Swiss franc contracts with these multi-nationals and cannot give FX rate changes directly to the consumers.

- Retailers have long-term contracts, longer lasting production processes or purchased early. This and their bargaining power prevented a quick weakening of prices.

- Many companies expected the EUR/CHF to rise again and waited before they gave the FX rate back to the consumer.

- Some importers hedged the weaker euro, for example to EUR/CHF 1.29 via forward contracts. Due to this higher EUR/CHF rate they could not give cheaper prices in full.

- Parts of the supply chain are still in Switzerland, e.g. the retailers who must pay rent, labor costs and high marketing costs in the Swiss franc. We will clarify, if and how far the 26.5% import share is affected by this Swiss part of the supply chain.

2) Car oversupply and weakening prices for existing inventory

During 2010 and 2011 car dealers thought about making big profits with the perceived “temporary” euro weakness. Large quantities of new and used cars were imported to Switzerland, which created an oversupply that finally concerned even used cars of Swiss origin. According to research by the Swiss price monitoring agency, car prices were 20% higher in Switzerland in August 2011 than in the euro zone, but until 2008 only 5 to 10%.

Subsequently, prices for used cars that were still in stock needed to be reduced. The price index for cars and motorcycles – 4.7% of the CPI basket, part of the “transportation” category – stood at 99.4 in November 2010, the same value as in November 2009 despite the weaker euro and price reductions, that car dealers called the “euro bonus”. Thereafter however, this index subcomponent of the “transportation” category has fallen to 95.9 in 2012 and finally to 83.9 in December 2014.

(source detailed Swiss price indices)

3) Existing rental contracts: heavy state regulation

Due to falling Swiss government bond yields and monetary easing, mortgage rates have fallen to record lows. By Swiss regulation, weaker mortgage rates must be reflected in the so-called “reference interest rate” for existing rental contracts. Based on the reference interest rate, Swiss tenants have the right to demand and receive a rent reduction for existing contracts. Even if some tenants are reluctant to really do this, it helped to contain rising rents caused by higher real estate prices.

| Reference index | Date of Change |

|---|---|

| 2.00% | 02.09.2014 |

| 2.00% | 03.06.2014 |

| 2.00% | 04.03.2014 |

| 2.00% | 03.12.2013 |

| 2.00 % | 03.09.2013 |

| 2.25 % | 04.06.2013 |

| 2.25 % | 04.03.2013 |

| 2.25% | 04.12.2012 |

| 2.25% | 04.09.2012 |

| 2.25% | 02.06.2012 |

| 2.5% | 02.03.2012 |

| 2.5%* | 02.12.2011 |

| 2.75% | 02.09.2011 |

| 2.75% | 02.06.2011 |

| 2.75% | 02.03.2011 |

| 2.75% | 02.12.2010 |

| 3.00% | 02.09.2010 |

| 3.00% | 02.06.2010 |

| 3.00% | 02.03.2010 |

| 3.00% | 02.12.2009 |

| 3.00% | 02.09.2009 |

| 3.25% | 02.06.2009 |

| 3.5% | 03.03.2009 |

| 3.5% | 02.12.2008 |

| 3.5% | 10.09.2008 |

Once the SNB raises interest rates, this downwards adjustment can turn into a continuous upwards move. This movement will be amplified with rising home prices.

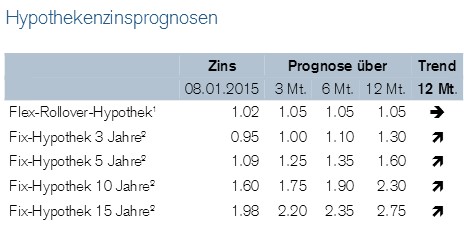

Development of Swiss mortgage rates:Credit Suisse and other Swiss banks announced the “bottoming out” of In 2009 Credit Suisse called for a bottom of 3.75% for fixed ten-years mortgages. In 2010 they saw rising rates coming: 10 years mortgages were at 3%. In December 2012 mortgage rates were at 2.04% and once again, Credit Suisse called it the bottom. In 2015 the bottom fell to 1.60%. As usual the banks predict higher rates in the future. |

|

Lower rates, however, do not mean that one needs to delay the decision to buy a home: for us, the Swiss real estate bubble has just started and has another ten to fifteen years to go. With the counter-cyclical capital buffer, however, the SNB might require more capital from banks. A reason that rates might really bottom out in two or three years time.

4) Long-term rental contracts for businesses

Especially for Swiss businesses, rental contracts are on a long-term basis, e.g. over five or ten years. The landlord cannot increase the rent for existing business contracts. On the contrary, a lower reference interest rate could theoretically reduce the rent (details here).

5) Owner-occupied rent is missing in CPI

Similar to the European HICP, the Swiss consumer price index contains only some smaller components of owner-occupied rent. Rising house prices are therefore not reflected in the inflation figures (only via homes for rent).

6) European debt crisis and lower European inflation

The continuing European debt crisis, the weak ECB monetary transmission and weak growth in monetary aggregates in the euro zone put limits on European inflation and therefore on Swiss import prices. Furthermore, a slower increase of peripheral wages might slow down prices for imported goods: 10% of Swiss imports come from Italy, 3% from Spain.

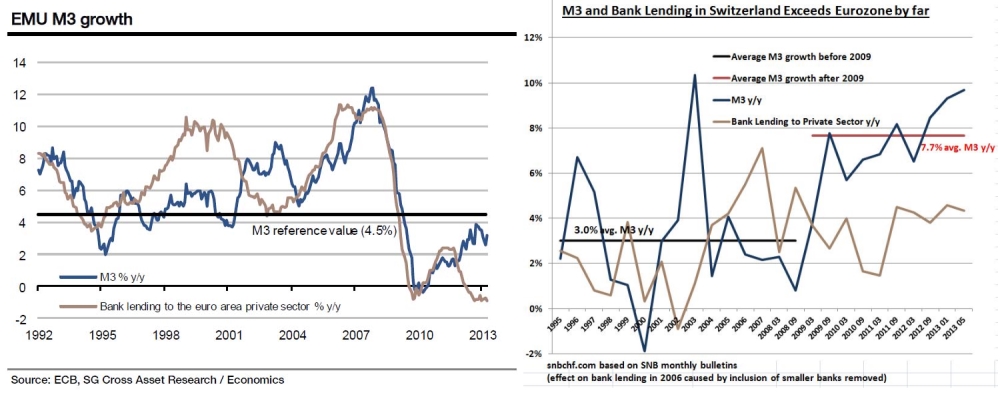

Upwards drivers of Swiss consumer prices1) Monetary expansion and capital inflowsSwiss M1 has risen by 100% between 2008 and 2012, the same as between 1994 and 2004; credit growth has also expanded by nearly 20% in both of these periods. For many economists, monetary expansion and rising asset prices have an effect on price inflation. One of these economists is the SNB’s former chairman Hildebrand. He showed in 2004 that a period of inflation had regularly followed the SNB’s monetary expansion in response to the rise of the franc. |

EMU vs. Swiss M3 Credit - Click to enlarge |

Swiss consumer price inflation has not yet followed the path Hildebrand indicated. Even Thomas Jordan, his follower as chairman of the SNB, is not afraid of the risk when the central bank pegs the Swiss franc to the euro. With this move he has contradicted some statements he published previously:

During the 1970s, monetary targets helped the Swiss avoid the worst effects of the stagflation in the United States. Currently, however, the SNB seems not to care about monetary targets any more. A reason might be that well-qualified immigration and labor competition helps to contain wages. |

|

2) Immigration into SwitzerlandIn the 1970s the Swiss decided to accept a far bigger revaluation of the Swiss franc than the SNB is ready to do now. The USD/CHF rate fell from 4.35 to 1.55 in only eight years. Finally Swiss GDP fell strongly because many foreigners left Switzerland (see below). Today things are different: with the Swiss-European bilateral agreements, only a small part of foreigners will leave Switzerland. Most of them are very well qualified. On the contrary, UBS even speaks of the “ten million Switzerland”, as compared to the eight million today. The combination of well-qualified personnel speaks for a rising consumer price index (CPI) via rising rents or higher prices of food. On the other side, those well-qualified people are able to reduce prices in particular in the export and tradables area, in the big multi-nationals, mostly covered in the PPI. In this analysis we concentrate on the CPI. |

Swiss Change of Permanent Resident Population - Click to enlarge |

3) Rising wealthAccording to SNB data, in 2011 the net worth of households rose by CHF 128 billion, or 4.7%, to CHF 2,822 billion. Financial assets held by households climbed by CHF 24 billion to CHF 1,982 billion (1.2%), with the increase dampened by the decline in share prices in Switzerland and abroad. Overall, assets were up by CHF 153 billion to CHF 3,528 billion (4.5%). Liabilities – mainly mortgage loans – grew by CHF 26 billion to CHF 706 billion (3.8%). As a result, net worth per capita increased by around CHF 12,000 to CHF 354,000 (3.6%). Higher wealth, however, has the consequence that cheaper consumption prices are less important for consumers and increases the ability of sellers to ask higher prices. 4) Rising real estate prices and resulting higher rentsThe same SNB data shows that the rise in wealth was mainly due to increased real estate prices, with the market value of real estate owned by households growing by CHF 130 billion to CHF 1,547 billion (9.2%). When the tenant changes then the landlord is then able to ask for a higher rent, which pushes inflation upwards. As visible in the graph from the tenants association, rents (red line) have risen far more than the overall CPI (blue line). |

Switzerland rents versus Consumer Prices 2008-2014 - Click to enlarge |

5) Higher real wages and disposable income

Real wages are up 2.2% against last year, rents and other prices are rising far more slowly. Hence, disposable income is getting bigger. With the higher disposable income consumers are less sensitive to higher consumption prices.

6) Rising German salaries and imported goods from Germany

The majority, namely 38.5% of Swiss imports come from Germany. German labour costs were rising by 3.4% per year in 2012, while in 2014 wages are up 3%, but cheaper oil reduces deflation.

7) Collective bargaining

Another aspect of inflation is (collective) bargaining: workers want to obtain higher salaries, so either they negotiate a higher salary e.g. together with unions or more often they go for a different employment opportunity. Traditionally bargaining was much stronger in Anglosaxon countries, Southern America and Southern Europe than in Germany or Switzerland.

In many of Asian collective societies, in particular Japan, people stay longer at one job with the consequence that wage increases are smaller.

Summary

The following table compares the upwards and downwards drivers of Swiss inflation.

Factor Direction Horizon

Slow price adaptation for imported goods after strong franc slowing inflation short-term (1-2 years)

Car oversupply, weakening prices slowing mid-term (2-5 years)

Existing rental contracts with smaller reference interest rate slowing short-term

Missing owner-occupied rent slowing systematic failure, in SNB secondary targets

European peripheral debt crisis slowing mid- (to long-term)

Monetary expansion higher inflation mid-term to long-term

Immigration, cheap labor lower inflation long-term (> 10 years)

Rising wealth higher mid-term to long-term

Rising real estate prices, higher rents higher mid-term to long-term

Higher disposable income higher mid-term

Higher German salaries, higher import prices higher mid-term

Low unemployment, (collective) bargaining Higher short-term to mid-term

It becomes clear that the short-term and some mid-term deflationary factors will be washed out in the next two to five years: car prices, the weak reference interest rates and price adaptation of imported goods will continue to put downwards pressure on the CPI. How quickly this happens depends on the state of the global economy.

The SNB has set its inflation forecast for 2016 to values of close to 1%. The 1% threshold is for us the level when the floor should be removed. This inflation forecast also implies that the floor will not be raised.

According to the UBS real estate index, prices are in the risk zone and have finally established the countercyclical capital-buffer. This measure would force banks to set capital aside for each loan, but would further reduce the capital basis of major Swiss banks.

We think that in three to five years time, Switzerland will reflect the German inflation rates: wages and labour costs will rise a bit more slowly than in Germany, but real estate and rents more quickly.

Should the floor still exist in ten years time, we agree with Thomas Jordan’s view from 1999 when he said “Swiss inflation rate would not be equal to the European one, but even higher.”

2 comments

Roman

2014-06-15 at 17:09 (UTC 2) Link to this comment

My perceived inflation is much higher. Every year the day ticket (Tageskarte) at Corvatsch costs 3-5 CHF more than the previous year.

The state owned railyway company SBB raises ticket prices every other year. Often products that are sold for more or less the same price have way lower quality (inferior product for the same price).

I would rather say we have at the same time price inflation for scarce products (event tickets, non-automatable services, land, real estate, bitcoin) and deflation for abundant mass products (e.g. consumer electronics, storage, chips, used cars, …).

George Dorgan

2014-06-16 at 05:51 (UTC 2) Link to this comment

Effectively currently the internal inflation like services or education moves at nearly 1.5% or 2% per year. Most other things are driven by the “strong franc” or by improvements in technology, e.g. in consumer goods.