George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

The increasing volatility of SNB EarningsAnnual results are not really definite. Given that the SNB accumulates foreign currencies with interventions, they have huge swings. But the SNB may lose 50 billion in one year and win 60 billion in the next year or vice verse. Good years of the Credit CycleThis trend was stopped in 2016, even without the need for a cap on the franc. But one should consider that we are in the good years of the credit cycle now. Bad quarters like the one in Q4/2018 are rare now.

Franc will rise again with crisis or inflationWith a new financial crisis or a with a big rise of inflation, the run into the Swiss franc will start again. And this at an exchange rate that is not digestible for the SNB.

And this will lead to a massive SNB loss around 150 billion CHF.

|

[ProfitLoss2019] |

Some extracts from the official statement.

|

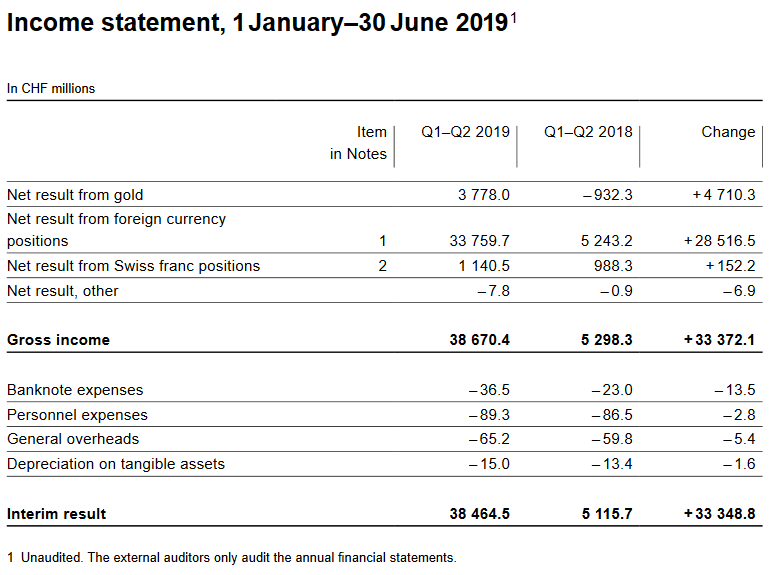

Income statement, 1 January–30 June 2019 Source: snb.ch - Click to enlarge |

||||||||||||||||||||||||||||||||||||||||||||||||

Profit on foreign currency positionsThe main driver of the profit was price changes in bonds and equities, what will not be the case when inflation will finally climb upwards. As often in the past, the SNB lost money on Exchange Rate

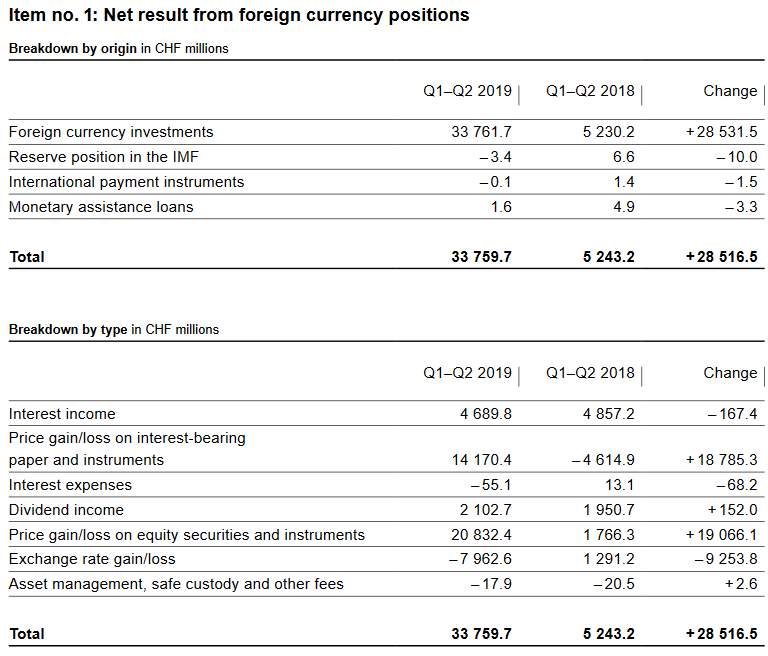

The following numbers are in billion Swiss Francs.

|

SNB Profit on Foreign Currencies Source: snb.ch - Click to enlarge |

||||||||||||||||||||||||||||||||||||||||||||||||

Valuation loss on gold holdingsGold finally had profits. Usually the Swiss Franc is in line with gold. This means that higher prices in gold is able to counter the losses on Exchange Rate.

Percentage of gold to balance sheetThe percentage of gold has risen to 5.5% thanks to higher prices.

Balance Sheet The balance sheet has expanded by over 68.3 bn. francs by 8.81%.

|

SNB Balance Sheet for Gold Holdings for Q2 2019 Source: snb.ch - Click to enlarge |

||||||||||||||||||||||||||||||||||||||||||||||||

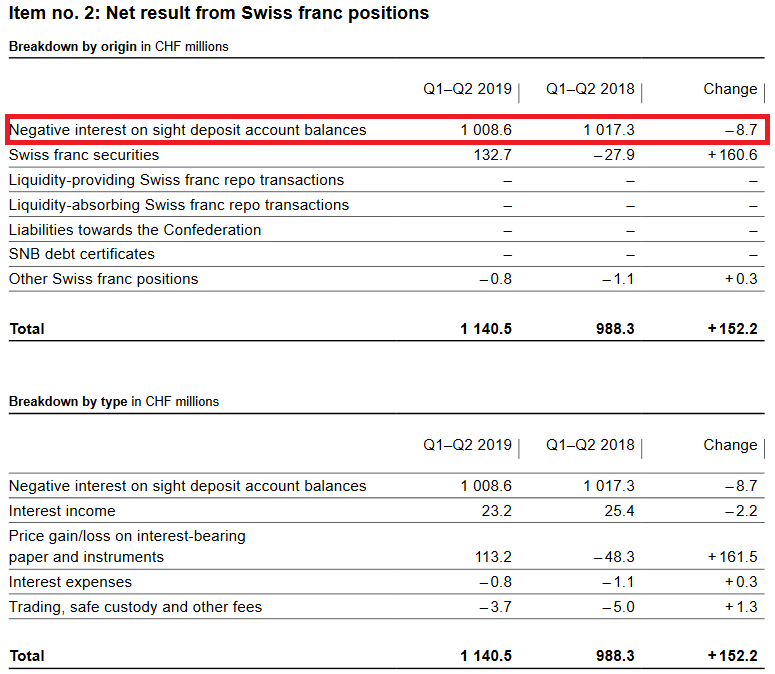

Profit on Swiss franc positionsThe SNB maintains its profitability, last but not least, thanks to the reduction of the profitability of banks. When too many funds arrive on their accounts, they must deposit them on their sight deposit account at the SNB.

Negative Interest ratesFurthermore, the SNB harms the Swiss economy, when it reduces the profits of Swiss banks by negative interest rates. But with this measure she maintains her own profitability. The SNB obtained slightly less money for negative rates, while sight deposits were slightly up (see below). The reason might that banks better use their exoneration from negative rates. Still, as compared to the FX profits or gains on equities, this number is relatively low.

|

SNB Result for Swiss Franc Positions for Q2 2019 Source: snb.ch - Click to enlarge |

||||||||||||||||||||||||||||||||||||||||||||||||

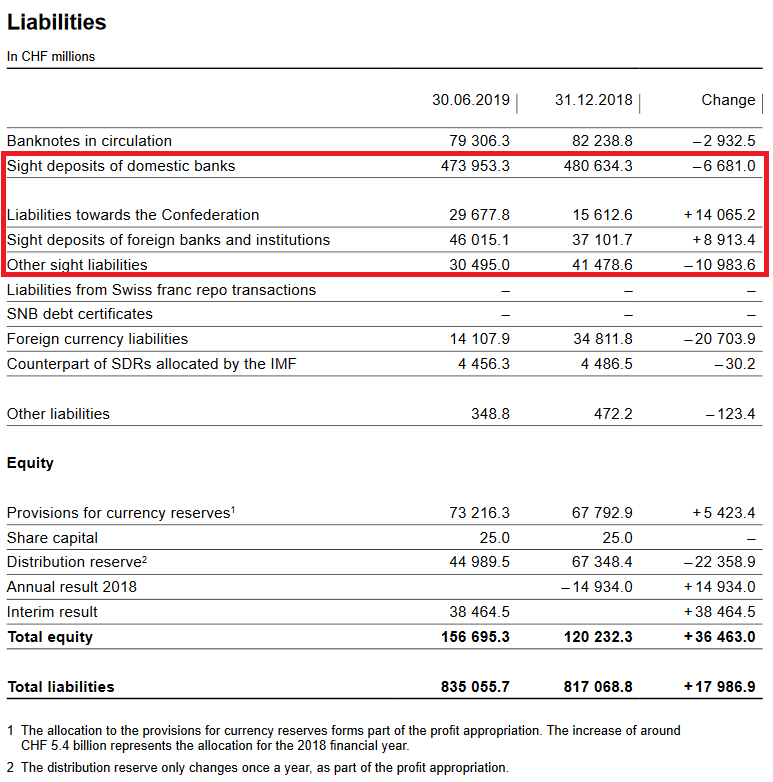

SNB LiabilitiesElectronic Money Printing: Sight Deposits Sight deposits is the biggest part of SNB interventions. In the current business cycle sight deposits are falling slightly, because companies invest more, instead of holding cash.

Paper Printing Banknotes in circulation: -2.93 bn francs to 79.3 bn. CHF

It showed that safe-haven Swiss francs, e.g. 1000 franc bank notes are currently less in demand than previously.

Provisions for currency reservesThe SNB seems to think that the price gains in bonds and in stocks are forever sure. While she will do some adjustment for FX changes, for a potentially stronger franc.

|

SNB Liabilities and Sight Deposits for Q2 2019 - Click to enlarge |

Tags: newsletter,SNB balance sheet,SNB equity holdings,SNB Gold Holdings,SNB profit,SNB results,SNB sight deposits,Swiss National Bank