Investors are optimistic that the Wednesday kickoff of the US-China trade summit, featuring President Trump and Chinese President Xi Jinping in Beijing, will result in a durable deal. The current hope is for an agreement currently labeled as a "Board of Trade" framework. Such a pact would create a trade mechanism in which each side could reduce tariffs on roughly $30 billion in non-sensitive goods.

The positive market reaction leading into the China trade summit has merit. Equity investors want more certainty on trade; thus, even a handshake and in-person trade dialogue between the US and China is positive. However, before anticipating a deal and market rally, there are a few considerations worth discussing.

- The Supreme Court struck down Trump's tariff authority earlier this year, forcing the administration to rebuild its trade toolkit by relying on slower and less effective mechanisms. Bottom line, Trump has less trade firepower than he did in 2025, and China knows it.

- Goldman Sachs claims the base case isn't a deal, it's a delay. Their economists see the most likely outcome as both sides pulling back from their most aggressive postures and extending the existing tariff pause, possibly indefinitely. That's more akin to a ceasefire than a lasting trade agreement.

- On August 12th, the pause on the 90-day China tariffs will end. If no durable trade framework is in place by then, tariff rates could revert to levels seen on April 2nd, 2025. That is a bearish scenario that markets are not pricing in today.

The China-US trade discussions will almost certainly create good optics. The question, however, is whether they will result in any meaningful resolution, thereby allowing investors to sleep more easily.

What To Watch Today

Earnings

Economy

Market Trading Update

Yesterday, we discussed market statistics on what happens after 6 weeks of consecutive market advances. Today, I want to focus on what happens to markets when trading becomes more erratic. On Monday, for example, value stocks lagged as technology outperformed. Tuesday saw the exact opposite as technology stocks were sold off. But on Wednesday, value stocks were under pressure as money gravitated back to technology.

The tape's been doing something strange for a few weeks now, and you should pay attention. In one session, value leads while growth gets slapped. The next session, it flips. Energy and industrials rip on Monday, then the AI semis tear higher on Tuesday while staples and utilities give back gains. Tuesday brought what could have been the worst Nasdaq selloff since March, then a 1.5% intraday rally into the close that almost erased it. The VIX popped above 19, the highest reading since late April, and then settled lower by the bell. That's not orderly trading. That's a market arguing with itself.

If this feels familiar, it should. We've seen this movie before, and the credits are worth reading.

Look back at late 1999 into early 2000. Value indexes outperformed growth by double digits over short stretches as the dot-com bubble began to wobble, then growth surged back to a final spasm of highs. By summer, the rotation became permanent. Look at 2007. Financial leadership oscillated wildly through the spring as credit cracks began to show. Within a year, the cycle had turned. Look at late 2021 into early 2022. Mega-cap growth swung from leadership to laggard to leadership over a few months. Then the Fed pivoted to hawkishness, and growth got crushed for the next 9 months.

The common thread isn't that this kind of rotation always precedes a bear market. It doesn't. What it does signal is that the consensus about the next regime has fractured. Investors who felt certain about the path of liquidity, rates, or earnings growth no longer do. So capital rotates daily, looking for a winner that can hold leadership for more than 48 hours.

That's exactly the picture in 2026. The top ten names in the growth index still represent 56% of its weight, and that concentration cuts both ways. When mega-cap AI works, growth dominates. When the narrative wobbles on AI capex digestion, oil prints, or Fed timing, capital scrambles for shelter in energy, staples, and industrials. The S&P 500's headline VIX stays muted while single-stock and semiconductor volatility run 2.5 times richer. Beneath a calm surface, the kitchen sink is in motion.

So what does erratic rotation forewarn? Not always a crash. Often a correction. Almost always a leadership change. As we've noted previously, the market doesn't ring a bell at tops. It rings a few different bells at once and lets you guess which one matters.

Bottom Line: When value and growth can't agree on who's in charge for more than a session, the market is telling you the regime is changing. Watch breadth, watch bond yields, and don't mistake daily noise for direction. The rotation itself is the signal.

PPI

Following the slightly higher-than-expected CPI, PPI was well above expectations, rising 1.4% versus the consensus estimate of 0.5%. The core PPI, excluding food and energy, was up 1.0%, well above the 0.4% estimate. The graph below, courtesy of Bloomberg, breaks down PPI into its major components. While fuels and related energy products account for a significant share of the increase, the other components have recently been trending higher.

The bond market reaction was muted to both the CPI and PPI news. In fact, bond yields fell slightly after the announcement. This is likely occurring for two reasons. First, longer-term yields have risen to levels not far from where they stood when inflation was much higher in 2022. Second, the market is betting that the surge in prices of some goods is largely driven by the Iranian conflict and is transitory. To that point, there are disinflationary factors gaining strength, such as tariff removals and reductions, and the productivity benefits of AI.

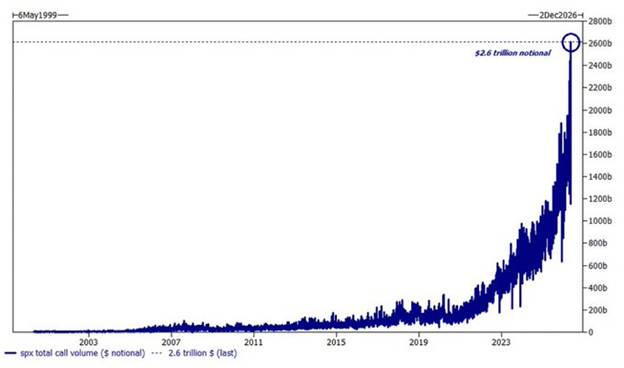

Gamma And Momentum: A Recipe For Spikes And Tears

When a stock trends higher, investors increasingly notice the bullish momentum and buy it, which pushes the price higher and attracts even more buyers. This type of herding behavior can create a self-reinforcing cycle- buying begets more buying.

When momentum is strong, the pressure on new investors to join the trade or on existing ones to add to their positions is enormous. As these investors focus on the incredible rewards they might receive, they often lose sight of the trade’s fundamental justification. The result is a crowded trade with sometimes breathtaking gains, but ultimately a sharp reversal that strips profits from most participants.

Retail and institutional momentum traders often use call options as a leveraged way to participate in price gains without buying the stock outright. Call options provide investors with limited downside risk and the potential for upside gains that can be multiples of the underlying stock’s price. Call buying can become a momentum accelerant, as we explain next.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

The post China Trade Summit: Deal Or Delay? appeared first on RIA.

Full story here Are you the author?You Might Also Like

Is The Iran War Good For The Petrodollar?

Is The Iran War Good For The Petrodollar?

2026-04-15

Diana Choyleva wrote an excellent editorial for the Wall Street Journal entitled “The Iran War Is A Boon For The Petrodollar.” She pushes back against claims that the Iran conflict is accelerating the death of the petrodollar. Instead, she argues the opposite: between Iran and Venezuela, the U.S. is defending and bolstering dollar dominance in …

The Stock Market Rally: Buy Or Fade It?

The Stock Market Rally: Buy Or Fade It?

2026-04-06

Last week, the stock market rally was one of the best performances in nearly a year. The S&P 500 surged 3.4%, the Nasdaq climbed 4.4%, and the bulls declared the correction over. As I have stated before, having watched markets for more than 35 years, I have come to recognize the difference between a relief …

USD Stablecoins And The Rebasement Of The US Dollar

USD Stablecoins And The Rebasement Of The US Dollar

2026-03-06

The “fiat is dying” argument has become a catchphrase narrative among digital asset bulls, gold bugs, and cryptocurrency advocates. That narrative’s core is that central banks have printed vast amounts of money. The “money printing” has led to currency debasement and rendered the U.S. dollar obsolete. We discussed this “debasement” narrative previously. The narrative is …

Software Stocks: Navigating The SaaSpocalypse

Software Stocks: Navigating The SaaSpocalypse

2026-02-25

The recent rotation from growth to value is well documented. While the return divergences between, for instance, technology stocks and materials or industrials stocks are significant, they do not tell the whole story. There are also extreme return differentials between broad industries and their sub-industries. In this article, we address one such divergence between the …

Calm Market Waters Hide Fierce Undercurrents

Calm Market Waters Hide Fierce Undercurrents

2026-02-18

The price movement in the broad S&P 500 index is relatively calm. Yet the market’s undercurrent, as measured by sharply diverging returns across stock sectors and factors, is anything but calm. The current market picture we paint is well embodied by a quote from Jules Verne in 20,000 Leagues Under the Sea. “The sea was …

Investor Lessons From 2025 For 2026

Investor Lessons From 2025 For 2026

2026-01-10

🔎 At a Glance 💬 Don’t Miss Our Upcoming “Live & In Person” Investing Summit Our 2026 Summit is THIS COMING WEEKEND and is a limited-seating event, so secure your tickets now before they sell out. Topics Include: I look forward to seeing you there. 🏛️ Market Brief – Market Starts Off The Year With …

Venezuela Leads Energy Stocks Out Of The Gate In 2026

Venezuela Leads Energy Stocks Out Of The Gate In 2026

2026-01-06

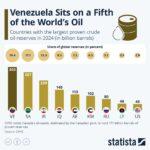

Venezuela holds 20% of the world’s proven oil reserves. Not only are they the largest, but as shown in the Statista graphic below, they hold approximately seven times that of the United States. Despite its large reserves, Venezuela has fallen well short of its ability to supply the world. US sanctions and the significant deterioration …

Tags: Featured,newsletter