Home › 1) SNB and CHF › 1.) SNB Press Releases › The good years have started, increasing SNB Profits

Previous post

Next post

The good years have started, increasing SNB Profits

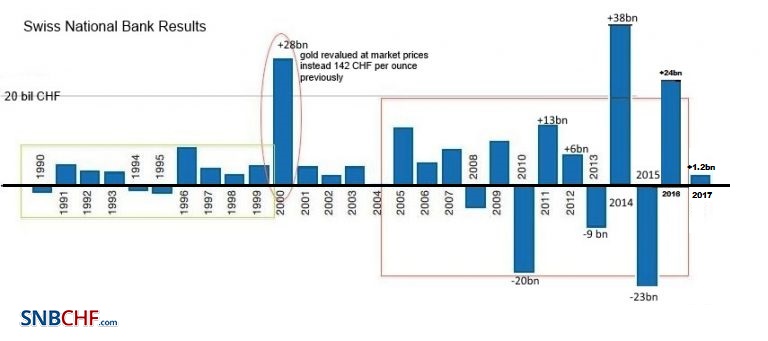

The increasing volatility of SNB Earnings

Annual results are not really definite. Given that the SNB accumulates foreign currencies with interventions, they have huge swings.

But in 2017, the picture is changed. Assuming a “biblical” cycle of seven good years and seven bad years, the SNB could now increase profits every year – thanks to a weaker franc and the seven good years.

… until the next recession comes and the seven bad years start.

At that moment the SNB will have to tolerate a massive loss:

- Given that the recession would be inflationary, she will tolerate a far stronger franc, for example EUR/CHF may fall from 1.25 to 0.90 over some years.

- Which will result into up 60-80 bn. CHF loss at the peaks.

|

SNB Results Longterm H1 2017 - Click to enlarge |

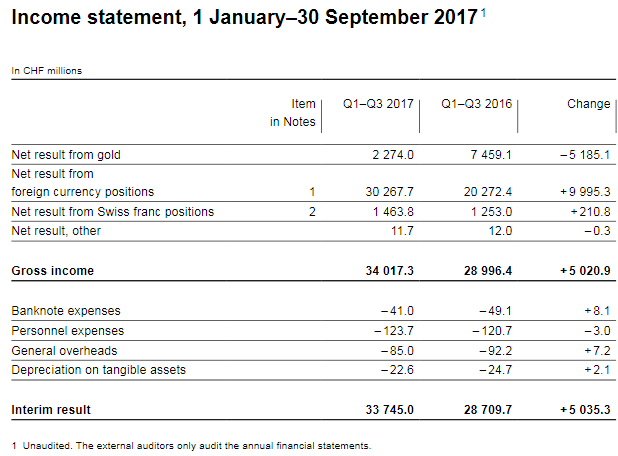

Interim results of the Swiss National Bank as at 30 September 2017.

The Swiss National Bank (SNB) reports a profit of CHF 33.7 billion for the first three quarters of 2017.

A valuation gain of CHF 2.3 billion was recorded on gold holdings. The profit on foreign currency positions amounted to CHF 30.3 billion, and the profit on Swiss franc positions to CHF 1.5 billion.

The SNB’s financial result depends largely on developments in the gold, foreign exchange and capital markets. Strong fluctuations are therefore to be expected, and only provisional conclusions are possible as regards the annual result.

|

Income statement, 1 January–30 September 2017  Source: snb.ch - Click to enlarge |

Profit on foreign currency positions

The net result on foreign currency positions amounted to CHF 30.3 billion.

Interest income accounted for CHF 6.8 billion and dividends for CHF 2.5 billion. Movements in bond prices differed from those in share prices. A loss of CHF 4.0 billion was recorded on interest-bearing paper and instruments. By contrast, equity securities and instruments benefited from the favourable stock market environment and contributed CHF 14.4 billion to the net result. Overall, exchange rate-related gains amounted to CHF 10.5 billion.

SNB results Q3 2017

(in bn CHF) |

Profit |

Balance Sheet |

Profit in % |

| Total Profit on foreign currencies |

30.3 |

813.5 |

3.70% |

| Interest income (coupons) |

6.8 |

813.5 |

0.84% |

| Dividend income |

2.5 |

813.5 |

0.31% |

| Price changes in bonds |

-4.0 |

813.5 |

-0.49% |

| Price changes in equities |

14.4 |

813.5 |

1.77% |

| Exchange Rate Losses |

10.5 |

813.5 |

-1.29% |

|

SNB Profit on Foreign Currencies Q1-Q3 2017 Source: snb.ch - Click to enlarge |

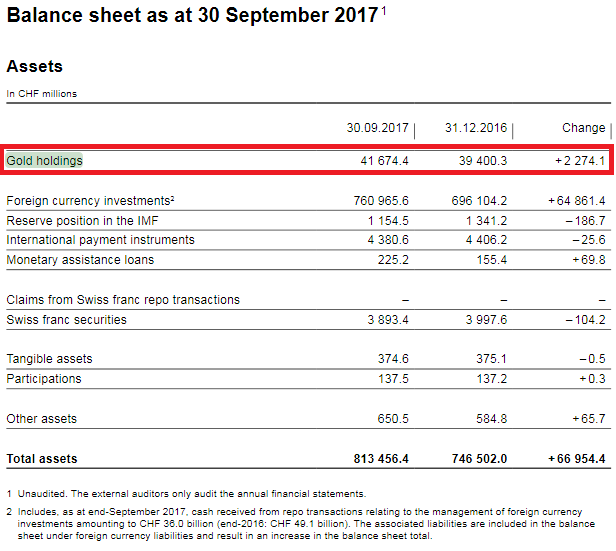

Valuation gain on gold holdings

A valuation gain of CHF 2.3 billion was achieved on gold holdings, which remained unchanged in volume terms. Gold was trading at CHF 40,071 per kilogram at end-September 2017 (end-2016: CHF 37,885).

SNB Results Q3/2017

(in bn CHF) |

Profit |

Balance Sheet |

Profit in % |

| Total Profit on Gold |

2.3 |

813.5 |

0.28% |

Percentage of gold to balance sheet

The percentage of gold compared to the total balance sheet is falling.

SNB Balance Sheet items

(in bn CHF) |

Q3 2017 |

2016 |

2015 |

2014 |

| Gold |

41.7 |

39.4 |

35.5 |

39.60 |

| Total Balance Sheet |

813 |

746 |

640 |

561 |

| Gold in % of Balance Sheet |

5.13% |

5.28% |

5.55% |

7.06% |

Balance Sheet

The balance sheet has expanded by over 66.5 bn. francs by 8.91%.

|

Q3 2017 |

2016 |

Increase in % |

| SNB balance sheet in CHF |

813.5 |

746.5 |

8.98% |

| Swiss GDP in CHF |

656 |

650 |

0.92% |

| % of GDP |

124.01% |

114,85% |

|

|

Balance Sheet as at 30 September 2017 Source: snb.ch - Click to enlarge |

While the SNB supports foreign stock markets and foreign companies, it does not invest in Swiss stocks.

|

Q1-Q3 2017 |

2016 |

| Swiss Franc Securities |

-31,6 |

45,5 |

| Total Balance Sheet |

813456 |

746502 |

| %CHF securities |

-0,0039% |

0,0061% |

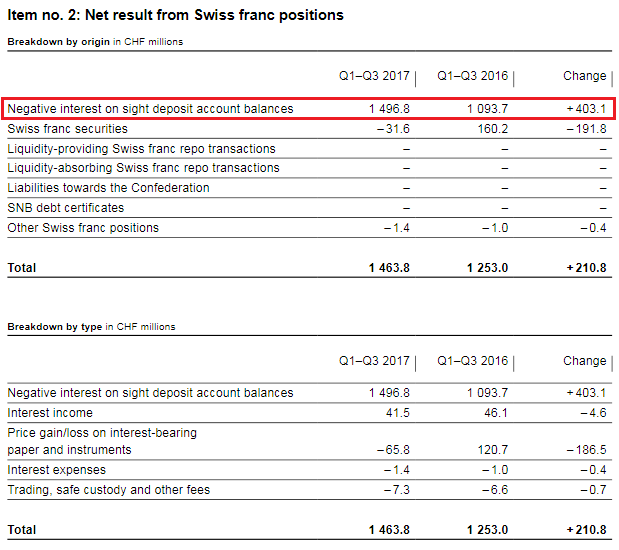

Profit on Swiss franc positions

The net result on Swiss franc positions totalled CHF 1.5 billion overall, which essentially resulted from negative interest charged on sight deposit account balances.

Negative Interest rates

Furthermore, the SNB harms the Swiss economy, when it reduces the profits of Swiss banks by negative interest rates. But with this measure she maintains her own profitability.

|

Q1-Q3 2017 |

2016 |

Change in % |

| Income through negative interest rates |

1.49 |

1.09 |

36.70% |

| SNB balance sheet |

813.5 |

746.5 |

0.08% |

| in % of balance sheet |

0.18% |

0.15% |

|

|

SNB Result for Swiss Franc Positions, Q1-Q3 2017 Source: snb.ch - Click to enlarge |

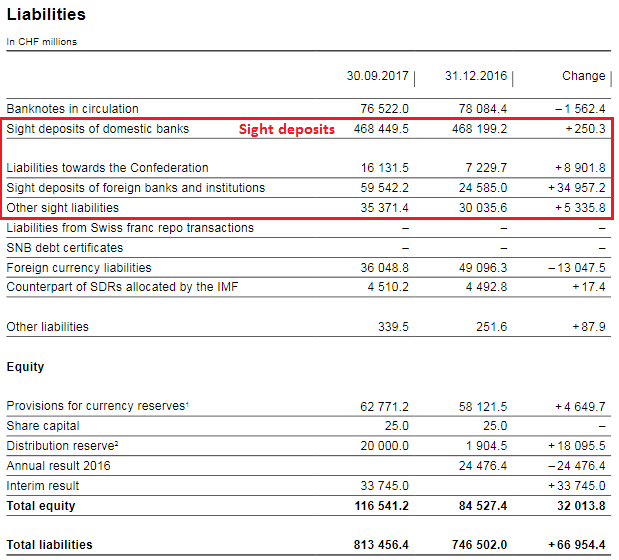

SNB Liabilities

Electronic Money Printing: Sight Deposits

Sight deposits is the biggest part of SNB interventions.

|

Q3 2017 |

2016 |

Change in% |

| Total Sight Deposits |

556 |

530 |

4.91% |

| Balance Sheet |

813.5 |

746.5 |

8.98% |

| % of balance sheet |

68.35% |

71.00% |

|

Paper Printing

Banknotes in circulation: -1.6 bn francs to 76.5 bn. CHF

The old form of a printing press, today a less important form of central bank interventions.

Provisions for currency reserves

As at end-September 2017, the SNB recorded a profit of CHF 33.7 billion, before the allocation to the provisions for currency reserves.

In accordance with art. 30 para. 1 of the National Bank Act, the SNB is required to set aside provisions permitting it to maintain the currency reserves at the level necessary for monetary policy. The allocation for 2017 will be determined at the end of the year.

|

SNB Liabilities and Sight Deposits, Q3 2017 Source: snb.ch - Click to enlarge |

Full story here

Are you the author?

George Dorgan (penname) predicted the end of the EUR/CHF peg at the CFA Society and at many occasions on SeekingAlpha.com and on this blog. Several Swiss and international financial advisors support the site. These firms aim to deliver independent advice from the often misleading mainstream of banks and asset managers.

George is FinTech entrepreneur, financial author and alternative economist. He speak seven languages fluently.

Previous post

See more for 1.) SNB Press Releases

Next post

Tags:

newslettersent,

SNB balance sheet,

SNB equity holdings,

SNB Gold Holdings,

SNB profit,

SNB results,

SNB sight deposits,

Swiss National Bank

Permanent link to this article: https://snbchf.com/2017/10/snb-interim-results-q3/

1 comments

Stefan Wiesendanger

2017-11-03 at 13:25 (UTC 2) Link to this comment

Mark to market reporting is highly problematic for the SNB. Philipp Hildebrand was fired because of a perceived conflict of interest between his personal holdings of foreign currency and the influence of his employer on the exchange rate. How much worse are the conflicts of interest embedded in the current institutional setup: the SNB as trustee of the value of the Swiss Franc reports huge profits if the value of the CHF drops and terrible losses if on the contrary it appreciates. To make it even worse, these inherently volatile profits and losses are prominently reported in the media with an eager eye on the profit distribution to the government.

Call it conservatism, call it revisionism – the solution would be obvious: abolish mark to market and move the reporting of effective and potential exchange rate effects from the P&L section to the risk section of the yearly report. And while at it, why not return to the old regime of ample undisclosed reserves instead of short-term market valuations? Maybe this requires leaving the IMF who may prescribe central bank accounting principles but so be it. If you aim higher than others, international standardisation is not your friend.