George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Until 2009 the ratio between debt (aka “credit-money”) and M1 (aka “money-money”) strongly increased. Arthur F. Shipman had an idea in January 2009 that should reduce credit and risks of our banking system and make our economy more efficient:

- “The Federal Reserve must gradually increase the Reserve Requirement. This will reduce the amount of credit-money that can be created from each dollar of money- money.

- To counterbalance the reduction of available credit, the Federal Reserve must accelerate the growth of the quantity of money in circulation. Ordinarily, that would be inflationary. But the reduction in credit growth will counteract the tendency for prices to rise. It is a balancing act to be sure.

- The Federal Reserve must continue to make credit available at extremely low interest rates. This will encourage borrowing (which, after all, helps the economy grow) but it will also be inflationary.

- Congress must create tax incentives to accelerate the repayment of debt. For new borrowing helps the economy grow, while old debt is simply a burden. Yin and yang.”

The New Arthurian Economics

“Scott Sumner sees raising interest rates as the right way to reduce inflation. Bill Mitchell sees raising taxes as the right way to reduce inflation. I see paying down debt as the right way to reduce inflation.” — Arthurian

The distinguished economic journalist Martin Wolf has suggested that banks should be stripped of their ability to create money when they lend. Endorsing “100% reserve banking” as outlined by, among others, the IMF, Lawrence Kotlikoff and Positive Money UK, he calls for all money to be created by the state and banks to be reduced to pure intermediaries. He explains how this would work thus:First, the state, not banks, would create all transactions money, just as it creates cash today. Customers would own the money in transaction accounts, and would pay the banks a fee for managing them.Second, banks could offer investment accounts, which would provide loans. But they could only loan money actually invested by customers. They would be stopped from creating such accounts out of thin air and so would become the intermediaries that many wrongly believe they now are. Holdings in such accounts could not be reassigned as a means of payment. Holders of investment accounts would be vulnerable to losses. Regulators might impose equity requirements and other prudential rules against such accounts.Third, the central bank would create new money as needed to promote non-inflationary growth. Decisions on money creation would, as now, be taken by a committee independent of government.Finally, the new money would be injected into the economy in four possible ways: to finance government spending, in place of taxes or borrowing; to make direct payments to citizens; to redeem outstanding debts, public or private; or to make new loans through banks or other intermediaries. All such mechanisms could (and should) be made as transparent as one might wish.

Income = Final spending. More to the point, money that is saved is NOT spend and is NOT used for income… Money that is saved is not “readily accessible for spending”: FRED: “M1 includes funds that are readily accessible for spending. M1 consists of:

(1) currency outside the U.S. Treasury, Federal Reserve Banks, and the vaults of depository institutions;

(2) traveler’s checks of nonbank issuers;

(3) demand deposits; and

(4) other checkable deposits.. .” Money in an account that is not “readily accessible for spending” is not in M1.…

MZM includes money market funds, it is a line much closer to debt than is M1 money. (People earn interest on their money market funds, right? So somebody must be paying interest for the use of that money. So really, it is debt, not money.)

(New Arthurian economics blog source)The distinction between debt , MZM and money is based on Keynes’ citations available here

Munich Personal RePEc Archive (it is certainly published in Germany 🙂

The New Arthurian Economics

Arthur F. Shipman

16. January 2009

Online at http://mpra.ub.uni-muenchen.de/12816/

MPRA Paper No. 12816, posted 17. January 2009 19:44 UTC

Amid all the talk of our current economic problems little has been said about inflation. Yet the two greatest economists of the 20th century expressed much concern over it; one even quoted the other on the subject.1 And if our current problems are a consequence of mis-handling our previous problems, the trail goes back to the inflation of the 1960s.

TERMS AND DEFINITIONS

M1 = money in circulation.

M2 = M1 + money in savings.

Credit is money available for borrowing. Borrowing puts credit to use. Debt is the measure of credit in use.

Credit-money = credit in circulation, or debt.

Money-money = money in circulation, or M1.

THE CAUSE OF INFLATION

People say printing money causes inflation, but the economy is not so simple. Printing money causes inflation the way printing books causes reading: It allows and encourages, but nothing more. As economists say, you cannot push on a string. It is not the existence of money, but spending that affects the level of prices.2

Milton Friedman showed a strong link between the quantity of M2 money and the level of prices.3 M2 is the total count of money in circulation and in savings. Money in circulation—money in the spending stream—affects prices directly. Money in savings affects prices indirectly, via the use of credit.

Think of money-in-circulation as money printed by our central bank, and credit-in-circulation as money loaned out by private banks like CitiBank. The two monies are indistinguishable in appearance, but credit-money carries the added cost of interest. We will distinguish them here by calling the one credit-money and the other money-money.

The focus of Professor Friedman’s work was to emphasize the relation between money and prices. Meanwhile, during pretty much all of Friedman’s career, the Federal Reserve was holding back the growth of the quantity of money to hold back the increase of prices. For most of that time the Fed restricted only the quantity of money in circulation. (See Chart #1.) The quantity of money in savings was allowed to grow, probably because of the link between savings and investment,4 and our desire to encourage investment.

Over the years money-in-circulation (M1) fell as a portion of M2, and money-in-savings rose. Private banks, flush with savings, increased their lending to fill the M1-void created by the Fed.

Credit-money issued by private banks increased as a portion of total currency in circulation. Money-money issued by the central bank fell as a portion of the total. The power of the Federal Reserve—its ability to fight inflation through control of the money supply—declined along with its share of the total.

But the shift in the M2 mix5 toward increased savings (and the consequent growth of credit-in-circulation) is not only a cause of the decline in the Fed’s power to control inflation. It is also a cause of inflation. For as the circulation of credit-money increased, so also did the cost of interest in the economy as a whole. On top of material costs and labor costs and profits, the growing cost of interest began working its way into prices.6

And the more we relied on credit-money, the more the cost of interest added to prices.7 1973 are given only for 1960, 1965, and 1970. So Chart #2 shows the old data for 1915-1972, and the new data for 1973 and after. The gap you see in Chart #2 represents the gap between the old and new data.

The change in the cost-structure was so profound that it changed the behavior of prices. Before the time of JFK, inflationary peaks were limited by the availability of money in circulation (which in those years was excessive). Since the time of JFK, inflation rises and falls with interest rates. By 1980 the quantity of money-money in circulation (M1) was so low that it hindered the production of output and pulled inflation down below interest rates. Yet inflation rates and interest rates continue to display similar trends.

The change in the cost-structure was so profound that it changed the behavior of prices. Before the time of JFK, inflationary peaks were limited by the availability of money in circulation (which in those years was excessive). Since the time of JFK, inflation rises and falls with interest rates. By 1980 the quantity of money-money in circulation (M1) was so low that it hindered the production of output and pulled inflation down below interest rates. Yet inflation rates and interest rates continue to display similar trends.

Interest as a factor cost increased over the years. So did interest income, of course. But other factor costs (like wages and profits) are payments for productive factors (labor and capital equipment). Interest is not. Interest is a payment for facilitating production. As people say, either you work for your money or your money works for you. Unlike other factor costs, the cost of interest is not counterbalanced by growth of output.8 So it pushes prices up.

THE MONEY MIX, IGNORED

Moreover, the cost of interest (in the economy as a whole) is a variable associated with money-in-savings as a portion of M2. The Fed could easily reduce the cost of interest by reducing the savings part of M2 (and the consequent growth of credit-use) relative to the circulating part. Interest is a necessary component of the cost of output. But economic policy can reduce the interest component by changing the balance between money-in- circulation and money-in-savings. Policy-makers have overlooked the option.

Friedman observed the growing imbalance in the components of money, but did not see it as a problem. “Base” money, he says, “remained remarkably constant at about 10 percent of national income from the middle of the nineteenth century to the Great Depression. It then rose sharply, to a peak of about 25 percent in 1946. Since then the ratio of base money to national income has been declining, and in 1990 was about 7 percent.” Friedman adds, “Further financial innovation is likely to reduce still further the ratio of base money to national income.”9

Base money (a component of M1) has declined relative to the national income (which we may roughly equate with output). In other words, base-money has declined relative to output. But Friedman also (famously) points out that M2-money has increased relative to output, causing inflation. Friedman sees base-money falling while M2 is rising. So he sees the monetary imbalance. But he expresses no concern about it.

Base money (a component of M1) has declined relative to the national income (which we may roughly equate with output). In other words, base-money has declined relative to output. But Friedman also (famously) points out that M2-money has increased relative to output, causing inflation. Friedman sees base-money falling while M2 is rising. So he sees the monetary imbalance. But he expresses no concern about it.

In Capitalism and Freedom, Friedman calls for “a legislated rule” designed to achieve “a specified rate of growth” of the money supply. But “the precise definition of money” established in this rule, he says, “makes far less difference” than just having the rule would make.10 For Friedman, any money is good enough. He is not concerned about the mix of components in the money supply. But I am concerned. The imbalance in the money mix, ignored by economists and policy-makers, is the central cause of our economic troubles.

THE EXCESSIVE RELIANCE ON CREDIT

Friedman showed that the increase of M2 money (relative to output) matches the trend of prices. But M1 money has decreased as a portion of M2. If we re-draw Friedman’s chart using M1 money, we get a trend-line that fails to keep up with prices. Money-in- circulation, in other words, is not the driving force behind inflation. But if the circulating component of M2 is not driving inflation, then the savings component must be driving it. However, sedentary money does not push prices up. It is not the accumulation of savings that causes inflation, but the use of savings (in the form of credit-money). Turns out it’s not printing money that’s been causing inflation, but lending and spending.

Suppose we put this in perspective. How much credit-money is in circulation today? Too much. This is not just my opinion. It is the opinion of everyone who says there is too much debt. For debt is only a yardstick that measures the use of credit: Debt is the measure of credit in use. If there is too much debt, then without doubt there is too much credit-money in use. And that is the money that’s been causing inflation.

In 1950 there was 40 cents of money-money in circulation for every dollar’s worth of output produced. In the year 2000 there was 11 cents. By these numbers, if your store does a million dollars in sales each year, then on an average day in 1950, customers walking into your store would have been carrying in total over $1000. In the year 2000 they carried a total of about $300. A thousand dollars in their pockets in 1950; $300 in their pockets in 2000. The $700 difference has been made up by the use of credit.

Mis-management of the money for half a century is the underlying cause of our economic problems today. Economists and policy-makers ignored chronic imbalances in the money mix. They restricted the growth of M1 money, at times even creating recession, without stabilizing prices. They encouraged the growth of savings and the use of credit-money, causing the unprecedented accumulation of debt. They said we save too little, failing to notice there was barely enough money-money in circulation to set any aside as savings. They spoke of the “mature” economy, meaning it had attained a gigantic financial sector. They had eyes but they could not see.

The massive accumulation of debt exists today not because people have bad character, and not because people don’t care about the future. The debt exists because economic policy takes money out of circulation and encourages the use of credit. The debt exists because of our anti-inflation policy. Policy has tilted the playing field toward excessive reliance on credit. Debt is an unintended consequence. And we have no policy designed to accelerate the repayment of debt. So debt accumulates.

Reliance on credit has driven the growth of the financial sector. It has increased the cost of facilitation relative to the cost of production. It has driven money out of productive work and into finance. “Since 1990, Ford has made more money from financial services, principally automobile loans to consumers and dealers, than from car- and truck-making operations.”11 Meanwhile, the use of credit-money has been contributing to inflation just as much as money-money would. More, actually, due to the added cost of interest.

THE CAUSE OF HARD TIMES

An imbalance in the money, manifesting itself as excessive reliance on credit, is the central problem in our economy today. It is the cause of inflation. It is the cause of debt accumulation. It is the reason business profits are low.12 It is the reason consumers have to stretch every dollar. It is the reason our economic environment no longer promotes the general welfare. It is the cause of hard times. But the excessive reliance on credit is not a new problem. It is a “once in a hundred years” event, if I remember correctly the words of Alan Greenspan. It is a recurring problem. The most recent previous occurrence of this problem is remembered today as the Great Depression.

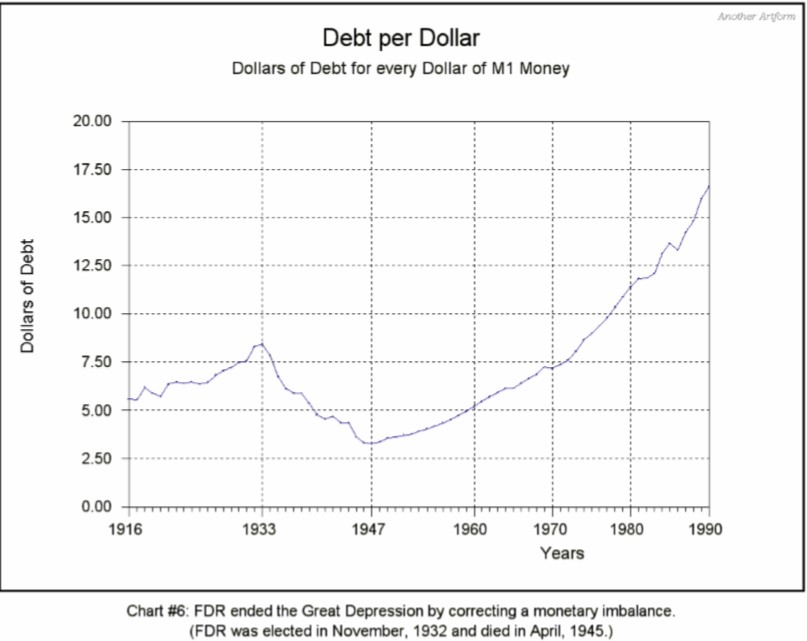

Franklin D. Roosevelt is remembered today for helping us through that time of troubles. Some people say his massive public spending ended the depression; others say World War II ended it. I say FDR ended the Great Depression by correcting a monetary imbalance. The massive public spending helped. The massive wartime spending helped. But if all that spending didn’t restore balance to the money mix, it would not have restored health to the economy.

A simple way to measure monetary imbalance is to compare credit-in-use to money-in- circulation. The higher this ratio, the more trouble people will have stretching their money to cover their bills. The ratio is calculated as dollars of debt per dollar of M1 money, or simply Debt per Dollar.

The Debt per Dollar ratio rose from $5.59 (in 1916) to $8.46 (in 1933). Then it fell to $3.28 (in 1947). Then it rose to $8.05 (in 1973) and rose to $12.12 (in 1983) and rose to $16.65 (in 1990) and $24.86 (in 2000) and $32.78 (in 2006).13 By 2007 each and every dollar of money in circulation had to support more than thirty-five dollars of credit in use. A dollar has to move mighty fast these days to be in all the places it has to be, to make all the payments that have to be made to keep the economy out trouble. So it’s no surprise our economy has got into trouble.

WHAT FDR DID

The Debt per Dollar ratio shows a persistent upward trend from the earliest data to the inauguration of FDR. It turns and shows a persistent downward trend throughout the Roosevelt administration. Then it turns again and shows an exponential upward sweep.

The trends on this chart are significant because they are so well-defined. The correction of monetary imbalance started—and ended—with the Roosevelt Administration.

As Chart #6 shows, the New Deal reversed a trend and corrected a monetary imbalance. The same solution is needed today. A reasonable goal would be to make it so that each dollar of money-money has to support about $20 of credit-money, rather than $35 or $40. But we don’t need to reduce debt-per-dollar to some particular figure. We just need to reverse a trend. We need the debt-per-dollar number to drift gently downward and keep heading down for a long time, just as it did under FDR.14

To reverse the trend and correct the monetary imbalance, our economic policies can follow this four-part plan:

- The Federal Reserve must gradually increase the Reserve Requirement. This will reduce the amount of credit-money that can be created from each dollar of money- money.15

- To counterbalance the reduction of available credit, the Federal Reserve must accelerate the growth of the quantity of money in circulation. Ordinarily, that would be inflationary. But the reduction in credit growth will counteract the tendency for prices to rise. It is a balancing act to be sure.

- The Federal Reserve must continue to make credit available at extremely low interest rates. This will encourage borrowing (which, after all, helps the economy grow) but it will also be inflationary.

- Congress must create tax incentives to accelerate the repayment of debt.16 For new borrowing helps the economy grow, while old debt is simply a burden. Yin and yang.

Note that the repayment of debt takes money out of circulation, thereby fighting inflation.

What we want is to get M1 up to maybe 20 cents per dollar of output and keep it there; and at the same time limit the growth of M2 (and credit-in-circulation) to avoid inflation.

ONE PROBLEM REMAINS

To fix our economy we must correct the monetary imbalance. It has been done before. FDR did it, and it worked. The four steps listed above create a policy that could keep a healthy economy healthy for a hundred years. If only we had put these changes in place

10 or 20 years ago, that would have been sufficient. Now, though, we may have waited too long. If Treasury Secretary Paulson is right, we are in an economic crisis of a sort not seen since the Great Depression. If Paulson is right, the solution requires government spending on a massive scale. If Paulson is right action is needed now. We cannot wait to see how far the economy falls. Every inch it falls will take yards and yards of government spending to gain it back. And that is a problem: For where will the money come from?

The money can come—the money should come—from the pool of funds the Federal Reserve has been withholding for half a century and more. The Fed can double the quantity of money-in-circulation on a whim. Of course, accepted theory says you can’t do that because it will cause inflation. But then, accepted theory ignores monetary imbalance. If we gradually double the quantity of money-money relative to output—and at the same time cut in half the quantity of credit-money that is created from money- money—then we have done nothing inflationary to the money supply. But we’ve reduced the growth of debt. We’ve reduced our reliance on credit. And we’ve reversed the trend of monetary imbalance.

The monetary imbalance resulted from a combination of factors: excessive reliance on credit, and a monetary policy that drives down the quantity of money in circulation. The solution requires us to increase the quantity of money in circulation, and to restrict the amount of credit created from that money. That is, correction of the monetary imbalance reduces debt and provides a source of funds. These funds can be used for the emergency spending needed to prevent a snowballing collapse of our economy.

Again: The Federal Reserve can provide the funds for the massive spending needed to prevent a second Great Depression. But if it does, it is absolutely essential to restrict the growth of credit use, so that total-currency-in-circulation grows at a non-inflationary rate.

We must continue to use credit of course, because credit helps our economy grow. But we must rely on credit-money for investment and growth, and on money-money for everyday expenses—as we did, say, in the time of Kennedy’s Camelot. And we must pay off our debt more quickly, because it completes the transaction, and because it fights inflation, and because it is the only way to relieve the burden that debt creates. Restoring the quantity of “M1 Relative to Output” to a level approaching that of the Kennedy years will make these things possible.

It is convenient that emergency funds can be provided by this four-step plan to restore monetary balance. It is convenient, but it is no coincidence. Snowballing economic crisis is the predictable final chapter in the story of monetary imbalance. The Arthurian plan can resolve the Paulson crisis because the crisis is the result of monetary imbalance pushed beyond its limits, and the plan deals specifically with monetary imbalance.

Resolving the crisis and correcting the imbalance require the same set of changes. It is no coincidence. It is evidence that my analysis of the problem is correct and my solution is the right solution.

© 2009 Arthur F. Shipman Released for Distribution [email protected]

BIBLIOGRAPHY & REFERENCES:

Bennet, James. “Ford Profits Up Sharply In Quarter.” The New York Times. October 27, 1994. Captured from //query.nytimes.com.

Bennet, James. “In Record Turnaround, Ford Had $2.5 Billion Profit in 1993.” The New York Times. February 10, 1994. Captured from //query.nytimes.com.

Friedman, Milton. Capitalism and Freedom. Chicago: University of Chicago Press, 1982.

Friedman, Milton, and Friedman, Rose. Free to Choose. New York: Harcourt Brace Jovanovich, 1980.

Friedman, Milton. Money Mischief. New York: Harcourt Brace & Company, 1994.

Keynes, John Maynard. The General Theory of Employment Interest and Money. New York: Harcourt Brace and Company,.

Meredith, Robyn. “Financial Powerhouse Takes Aim at Bad Credit Risks.” The New York Times. December 15, 1996. Captured from //query.nytimes.com.

Roosa, Robert V., “Cost-Push or Demand-Pull?” In Stabilizing America’s Economy. Ed. George A. Nikolaieff. New York: The H. W. Wilson Company, 1972. 117-27. From “A Strategy for Winding Down Inflation,” by Robert V. Roosa. Fortune (September 1971).

The data comes from Historical Statistics of the United States: Colonial Times to 1970, and from various editions of the Statistical Abstract.

- Free To Choose, Chapter 9, p.268: “There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency.” – John Maynard Keynes, quoted by Milton Friedman. [↩]

- In the current, depressing economic environment the concern is that our economizing will reduce our spending to the point that a snowballing deflation sets in. If a snowballing deflation takes hold, printing even a lot of money won’t do much to improve things. [↩]

- Money Mischief, Chapter 8, p.195: Friedman identifies his data in a footnote. He says his Figure 1 shows that money and prices “clearly have the same pattern” over the course of a century. [↩]

- The General Theory of Employment, Interest and Money, Chapter 2, p.21: Keynes describes “a nexus which unites decisions to abstain from present consumption with decisions to provide for future consumption.” [↩]

- M2 was re-defined some time around 1980, to account for deregulation and accelerating M2 growth. Editions of the Statistical Abstract after 1979 list much higher M2 values than the 1979 and earlier editions. For example, the number for M2 in 1970 is given as $424 billion (in the 1979 edition) and $625 billion (in the 1980 edition). I was unable to find revised data going back to 1915; and the revised numbers before [↩]

- The growing cost of interest left less to divide up as wages and profits. Wages and profits both suffered as a result. [↩]

- The growing circulation of credit-money changed the nature of inflation itself. Before 1960-63 we had demand-pull inflation. Since 1960-63 we have had cost-push inflation [↩]

- A bank’s costs include wages and salaries for the employees, and profits for the owners. In addition to these productive-factor costs there is the cost of interest the bank must pay to its depositors. That cost works its way into the prices we pay for goods and services without increasing the quantity of goods and services produced. And the more we rely on credit, the higher is this cost. [↩]

- Money Mischief, Chapter 10, p.255. A similar pattern is evident for M1 money in my Chart #1. [↩]

- Capitalism and Freedom, Chapter 3, p.54. [↩]

- From “In Record Turnaround, Ford Had $2.5 Billion Profit in 1993,” by James Bennet in The New York Times, February 10, 1994. And again: “Ford Motor Company has earned more as a banker than as a car builder in five of the last six years.” From “Financial Powerhouse Takes Aim at Bad Credit Risks,” by Robyn Meredith in The New York Times, December 15, 1996. [↩]

- “Ford’s net profit margin on auto sales was 2.4 percent.” That’s low. From “Ford Profits Up Sharply In Quarter,” By James Bennet, Published: October 27, 1994. Adam Smith’s The Wealth of Nations explains why profit must be measured as a “margin” or rate of return. Note that even the profits of Big Oil are low when measured as a profit margin rather than in dollars-per-second. [↩]

- Debt per Dollar has been doubling every 16 or 17 years. This is exponential growth. [↩]

- After that, it will have to be held down by design of policy. [↩]

- At present, the reserve requirement for money-in-savings is zero. This means the amount of credit-money banks can create is not limited at all by Federal Reserve policy. [↩]

- For example: If you make an extra $1000 payment on your mortgage or your college loan or your credit- card debt, you get to deduct $1000 from the taxes you owe the next April 15th. [↩]