George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

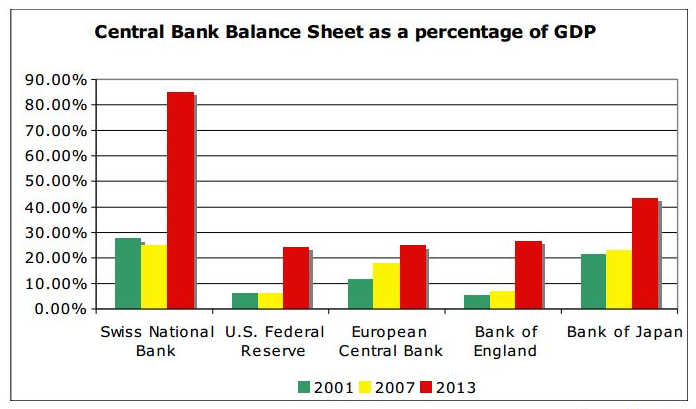

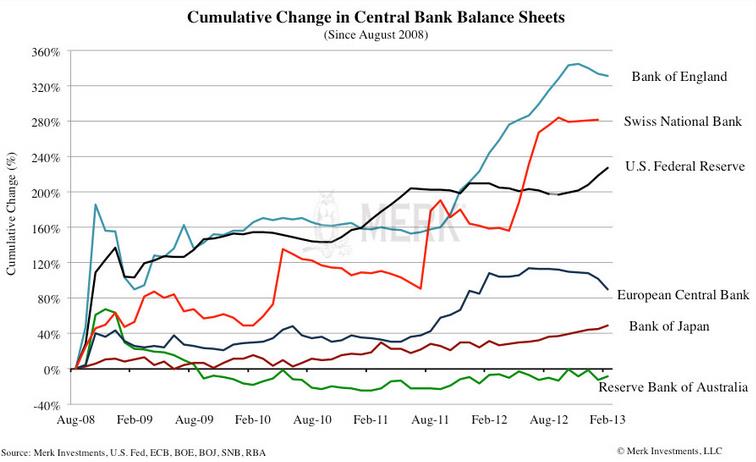

Since 2008 the balance sheet of the Swiss National Bank is 280% higher, this is the equivalent of 60% of Swiss GDP. So did most other central banks, too. But there is one big difference: The risk for the SNB is far higher, the SNB nearly exclusively possesses assets denominated in volatile foreign currency.

The Fed or the Central Bank of Japan mostly own local government bonds, they run an inflation risk but no currency risk.

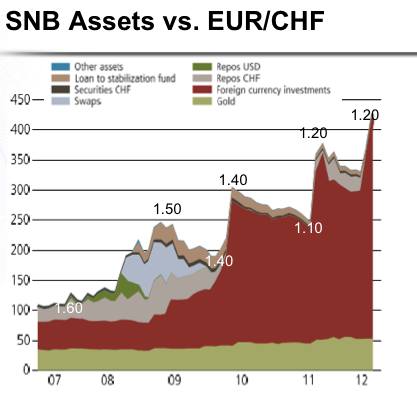

The following graph from UBS shows how the SNB has increased both assets and liabilities, its balance sheet expansion.

| We like to compare the increases with the fall of the EUR/CHF exchange rate.

The graph shows that a decrease of reserves was only possible when EUR/CHF appreciated. Maintaining the EUR/CHF relatively stable was only possible when reserves strongly rose.

|

Since 2008 the balance sheet of the Swiss National Bank is 280% higher, this is the equivalent of 60% of Swiss GDP. So did most other central banks, too. But there is one big difference: The risk for the SNB is far higher, the SNB nearly exclusively possesses assets denominated in volatile foreign currency. - Click to enlarge |

The following tables show the SNB balance sheet in comparison to the one of the Bank of Japan, another central bank that strongly intervenes in markets.

As said, the huge difference is that the Swiss buy foreign assets and foreign currency whereas the Japanese possess only 5% foreign assets, see more details.