George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

The following is possibly the best speech of an SNB board member.

For our blog: Short introduction by George Dorgan

Increase of credit in the U.S. was around 1.5% lower than real GDP growth between 1988 and 2001. This picture changed during the great moderation from 2001 to 2007: credit overtook real GDP growth and, thanks to low interest rates, it was 1.5% higher than real GDP growth, nearly equal to nominal output increase.

The most shocking is the following: Since 2010 the gap has become even higher: 2% more credit than real GDP growth. This essentially means that the credit bubble after 2010 is bigger than the one before the financial crisis.

source Pictet

As Pictet shows, the U.S. housing sector is still de-leveraging, but businesses are borrowing again.

source Pictet

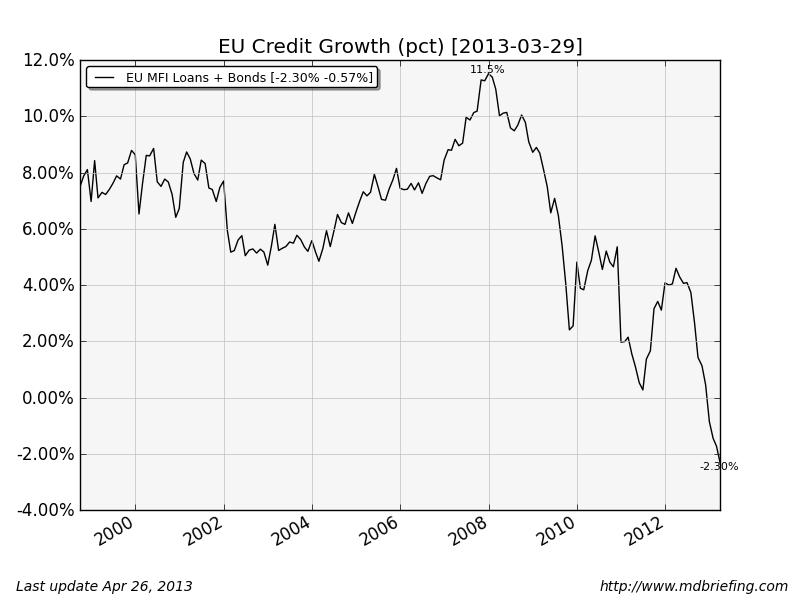

For us, the Swiss franc exchange rate is partially driven by competition in credit growth against the U.S., while European credit growth is still severely hampered. But since recently the U.S. is in the lead again, Swiss second and the euro zone is at the bottom.

Jean Pierre Danthine shows that since the financial crisis, Switzerland is quickly catching up with the previously excessive credit growth in countries like the U.S., Ireland, UK and Spain.

Jean-Pierre Danthine: Credit – is the sky the limit?

Introductory remarks by Mr Jean-Pierre Danthine, Vice Chairman of the Governing Board of the Swiss National Bank, at the International Center for Monetary and Banking Studies, Geneva, 16 April 2013.

* * *

I would like to thank Claudia Strub and Till Ebner for their very valuable support in drafting this speech and for the underlying analysis of the topic. I would also like to thank Robert Bichsel for his helpful comments.

1. Introduction

The Swiss Federal Council has recently decided to activate the countercyclical capital buffer (CCB) acting on a proposal by the Swiss National Bank (SNB). The key feature of this new tool is to counter the “pro-cyclical” behavior of financial institutions whose collective action can be a source of systemic risk. To this end it requires banks to temporarily increase the level of capital they must hold as a backing for mortgage loans on residential property. In doing this, Switzerland is one of the first countries to make effective use of a tool advocated by the international community as a means for preemptively dealing with cyclical risks to financial stability. What was the motivation for activating this instrument? The main goal of the CCB is to increase the resilience of financial institutions against the background of imbalances in the domestic mortgage credit and housing markets that have been building up gradually over the last several years. In 2012, these imbalances intensified further reaching levels that pose a risk to the stability of the banking sector, and hence to the Swiss economy. Here, two facts stand out.

First, real estate prices in Switzerland have been persistently increasing since 2000, at accelerated speed since 2008, reaching levels estimated to be 40 to 60% higher than 12 years ago (see Figure 1).1.

Dynamic Swiss real estate market - Click to enlarge

Second, the growth of credit volumes has been significant with the consequence that credit volumes relative to gross domestic product (GDP) have reached new historical peaks (see Figure 2a and 2b).

Figures 2a/b: Substantial increase in credit-to-GDP ration driven by persistent strong credit growth - Click to enlarge

The fact that these two developments have progressed hand in hand spells out conditions that may lead to subsequent financial instability. Indeed, historical evidence – widely documented by the Bank for International Settlements (BIS)2 – shows that such a twin development – elevated residential prices and dynamic credit growth – constitutes the prime advance indicator of financial instability. We only have to look outside our borders, to the US and various regions of Europe, or back through Switzerland’s own past to get a feel for the devastating consequences on the real economy of financial crises originating in real estate excesses.

2. Credit: is the sky the limit?

Today I would like to focus on one of the two critical elements mentioned above, the growth of credit volumes. Figure 2b easily explains the question asked in the title: is the sky the limit? The answer is just as easy. Clearly the credit-to-GDP ratio cannot grow indefinitely because otherwise the cost of servicing the debt would end up exhausting the whole of GDP. In other words: What we observe here cannot be the manifestation of a secular trend! As we

- Since 2000, average growth rates of real supply prices for single-family houses and owner-occupied apartments come to 2.5% and 3.7%, respectively (annual growth rates based on quarterly data provided by Wüest&Partner) [↩]

- Borio, C. (2012); see also Schularick, M. and Taylor, A. (2012 [↩]