George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

We have insisted in several posts that the northern euro zone is very reluctant to continuously bail out the periphery and in particular its banks. The euro group chief Dijsselbloem has confirmed this now.

In several posts (e.g. in Eurobonds, fiscal or banking union are all pure utopia or in

German Economists and Merkel, the Implicit Followers of the Gold Standard or in

A Sustained US Recovery Will Make a Eurozone Split Up Possible)

we insisted that the northern members of the euro zone are very reluctant to continuously bail out the weak ones, and in particularly to bail out the banks, hedge funds and bond holders. Finally, they would not allow the moral hazard that the euro group would throw good money after bad.

Conditionality has maintained its place against the unlimited cheap funding contained in the ECB’s Outright Monetary Transactions (OMT), even markets believed the opposite for months.

On the contrary, cheap funding has not helped yet ,monetary transmission has not work in the periphery yet. European growth is still slow, but conditionality has already hit.

- Eurobonds will not come in our generation. Germany’s Merkel clearly stated that she will not allow this as long as she lives.

- Even the German opposition does not want a direct ESM financing of banks. Only 17% of Germans want Eurobonds. Germans would accept a fiscal union only when German discipline dominates.

- As opposed to Germany, who still feels responsible due to its history, Finland is especially resistant and wants collateral for further bailouts

Below we publish an important part of an interview with the chief of the euro group, the Dutch finance minster Dijsselbloem.

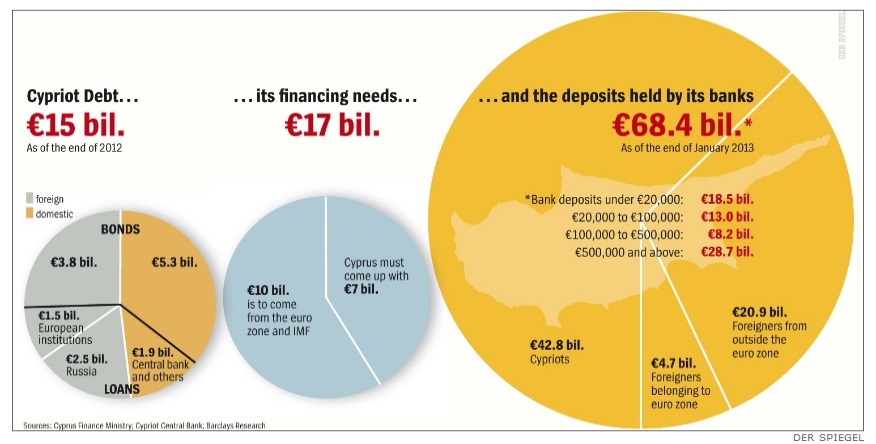

One day after the interview, Dijsselbloem issued a statement and said that Cyprus is “a specific case with exceptional challenges” and that “no models or templates” will be used in the future. This is visible in the following graph:

The deposit data is two months old, many of them managed to leave Cyprus in time.

The interview:

Q: To what extent does the decision taken last night end up setting a template for bank resolution going forward?

A: What we should try to do and what we’ve done last night is what I call “pushing back the risks”. In times of crisis when a risk certainly turns up in a banking sector or an economy, you really have very little choice: you try to take that risk away, and you take it on the public debt. You say, “Okay, we’ll deal with it, give it to us.”

Now that the situation is more calm and the financial markets seem to have become more steady and easier, we should start pushing back the risks. If there is a risk in a bank, our first question should be: “Ok, what are you the bank going to do about that? What can you do to recapitalise yourself?” If the bank can’t do it, then we’ll talk to the shareholders and the bondholders. We’ll ask them to contribute in recapitalising the bank. And if necessary the uninsured deposit holders: “What can you do in order to save your own banks?”

In other words, taking away the risk from the financial sector and taking it onto the public shoulders is not the right approach. If we want to have a healthy, sound financial sector, the only way is to say: “Look, there where you take on the risks, you must deal with them. And if you can’t deal with them, you shouldn’t have taken them on and the consequence may be that it’s end of story.” That is an approach that I think we should, now that we’re out of the heat of the crisis, consequently take.

I’ve tried to do so as far as I could in nationalising the SNS bank in the Netherlands. We’ve completely wiped out the shareholders and the junior bondholders. We have to bring down the tab to be picked up by the taxpayers.

Q: What does that say for other countries in the eurozone that have very highly-leveraged banking sectors, Luxembourg, Malta even? Much larger than Cyprus’.

A: It means: deal with it before you get in trouble. Strengthen your banks, fix your balance sheets, and realise that if a bank gets in trouble, the response will no longer automatically be we’ll come and take away your problems. We’re going to push them back. That’s the first response that we need. Push them back. You deal with them.

Q: That sounds a whole lot like what people were suggesting before Lehman Brothers. They made a bad investment in Lehman Brothers; let it go down. And we saw what happened after that. Is there any risk that this change in thinking risks coming back to the ‘too big to fail’…

A: I think we have to realise before we come to a decision can we let a bank fall over, is it too big to fail, there are a lot of things that can be done. To start with, we should not waste any time in fixing balance sheets. Banks have to build up their reserves, have to become much more stable and strong within themselves.

Secondly, we need mechanisms to deal with risks in terms of: if a bank is in trouble, can you take out the bits you want to save and let go of the bits you don’t want to save, the “living will” approach.

Thirdly, if a bank does get in trouble, to who can we shift the account? Who’s going to pay for it? That’s what I was talking about just now, to shareholders, etc. Then there comes a point where you, as a government, may have to step in, but that should be the order. You take preventive measures, you make sure banks are more stable, more robust. If there still is a problem, you need mechanisms to address them, to pull banks apart, etc. You need to bail in those people whose equity is involved, etc.

Q: This is basically the [Michel] Barnier proposal [for a common EU bank resolution regime]. The priority seems to be removing that moral hazard.

Q2: Those proposals now look like they’re going to be delayed, I think, from Barnier. In a way, you’ve had a chance with Cyprus as a kind of test case, if you like. Does it feel like that?

A: Like I said, it’s very hard to do this if there’s a lot of nervousness in the markets and there is still a crisis atmosphere. Now that the crisis atmosphere is disappearing – we had a little upheaval last week after the levy discussion – but looking at it a couple of days later now, a week later now, the markets have really been very wise in responding to this whole levy thing. So now that the crisis seems to fade out, I think we have to dare a little more in dealing with this.

Q: It just makes me think of one thing, off the cuff, which has to do with the ESM [European Stability Mechanism] and the direct recapitalisation of banks. Does that change the kind of calculus in terms of how that is used going down the road? There have been suggestions it may never be used if you have fully-functioning bail-in systems. Is that what we’re saying?

A: I think that’s what we should aim at. We should aim at a situation where we will never need to even consider direct recap. The interesting thing of course that in the Spanish situation, because that where the demand for a direct recap instrument started, from the Spanish banking crisis. We are now dealing with the Spanish banking sector – restructuring it, recapitalising it, bad bank, some bail-in – without this instrument. If we have even more instruments in terms of bail-in and how far we can go in bail-in, the need for direct recap will become smaller and smaller.

I can just repeat what I said. I think that the approach has to be: Let’s deal with the banks within the banks first, before looking at public money, be it direct recap or any other instrument coming from the public side. Banks should basically be able to save themselves, or at least restructure or recapitalise themselves as far as possible.

Q: Is that new philosophy, was it hard among the 17 [finance ministers], are there people who it’s been hard to convince this is the right approach?

A: Well, there is still nervousness, understandably, about can we pull it off, what will it mean in the financial markets, how will the financial markets react to the eurozone, to the financial institutions in the eurozone, etc.

That was one of the reasons why, last week, we didn’t go down the bail-in track [in Cyprus] but went down the levy track. Now we’re going down the bail-in track, and I’m pretty confident the markets will see this as a sensible, very concentrated and direct approach instead of the more general approach [of] let’s levy everyone to gather the money for the banks. So yes, that that is a sort of shift in approach.

Q: Is this something that you’ve sort of market tested, if you like, with the market? You’ve had a lot of feedback? You just said you feel very confident that the market will respond positively to the bail-in approach. Is that the feedback you’ve had?

A: You get two kinds of feedback. There’s the economic analysts that say this is a sensible approach, it makes sense. And then there’s more the investors’ reaction, who will say: “Look, we’re not to going to pay the tab, are we? If you do so, we will make our financing more expensive.”

My reaction would be: Maybe it’s inevitable that if you push back the risks, risks will be priced. Because if I finance a bank and I know if the bank will get in trouble I will be hit and I will lose my money, I will put a price on that. I think that’s a sound economic principle. And having cheap money because the risks will be covered by the government and I will always get my money back is not leaving to the right decisions in the financial sector, it’s not leading to the right risk management in the financial sector.

So there’s those two reactions from the financial markets: the analysts who are saying, let’s be real, this is a sensible approach, and the investors. My response is: If risks are going to be priced, then that is probably the right way to do it. It will force all financial institutions as well as investors to think about the risk they are taking on. They will have to realise it may also hurt them, the risks might come towards them instead of pushing them away. (source FT)

With the upcoming U.S. recovery, it becomes clear that the crisis in some countries in Southern Europe (and even France) will not have a much worse effect on the global economy than the Asian crisis in 1998.

The differences are the following: as opposed to the period after 1998, the United States is still struggling today. Secondly, the construction of the common currency does not allow for printing a way out of the crisis and devaluing. Consequently this crisis will take much longer to resolve than the issues related to the Asian crisis after 1998.

Are you the author?Tags: Bonds,Cyprus,Deposits,Too Big To Fail