Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has fallen by 0.15% to 1.0729 |

EUR/CHF and USD/CHF, October 14(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Turn around Tuesday saw the dollar bounce, particularly against the Australian dollar and European currencies, among the majors. Sterling pared earlier losses on reports that the UK would not walk away from the talks just yet, while the euro remains on its back foot. Emerging market currencies are mixed, leaving the JP Morgan Emerging Market Currency Index nursing small losses for the third consecutive session. The precious metals tumbled yesterday but have also steadied today, with gold near $1900. Led by the real estate and financials, the S&P 500 snapped a four-day advance yesterday but spent the session within the range seen Monday, leaving the opening gap untouched. Though Hong Kong reopened after being closed due to a storm and posted small gains, Asia Pacific markets mostly fell. India and New Zealand markets were the chief exceptions and posted small gains. Singapore and South Korea central banks left policy unchanged as expected. European equities are higher and recouping around half of yesterday’s 0.55% loss. US shares are also edging higher. Europe’s peripheral 10-year benchmark yields slipping lower to new record levels. The US 10-year yield is little changed, around 0.72%. Crude oil is little changed, leaving November WTI hovering around $40 a barrel. |

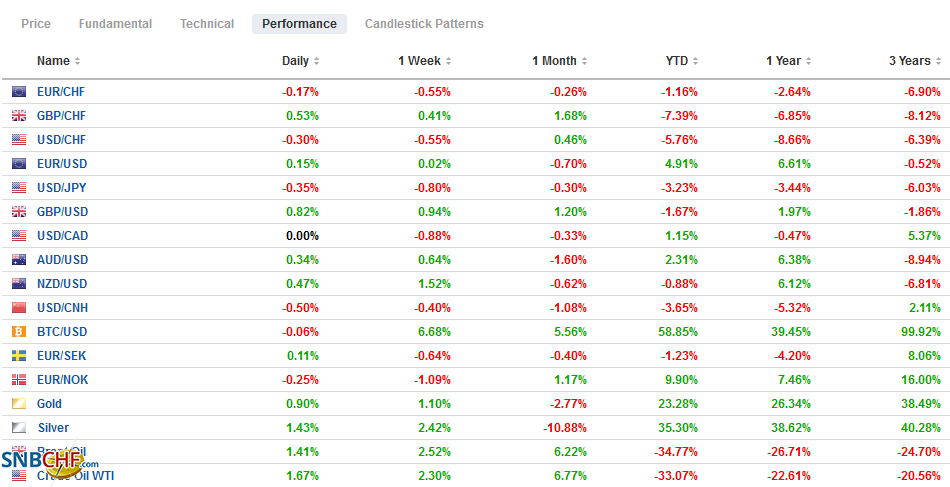

FX Performance, October 14 - Click to enlarge |

| Asia Pacific

China’s trade policies are irking its trading partners. US tariffs and Phase 1 trade agreement are well known. Yesterday, the EU imposed up to a 48% tariff on aluminum extrusions from China. It was the provisional result of an investigation that may not be completed until early Q2 21. The levies could be applied for five years, depending on the results of the investigation. |

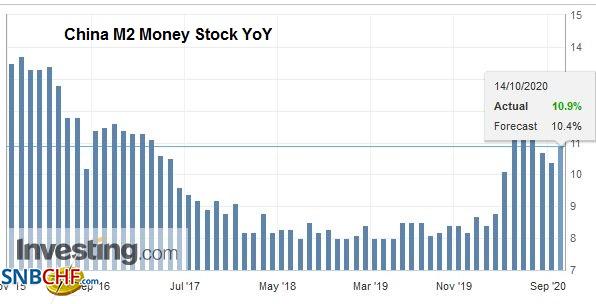

China M2 Money Stock YoY, September 2020(see more posts on China M2 Money Stock, ) Source: investing.com - Click to enlarge |

| China is no slouch, either using trade as an offensive weapon. Sanctions and limiting access to funding as the US does is not (yet) a strong weapon for China. Trade can be. Often times, the policy is not legislated or written down but announced nonetheless. This appears to be happening to Australia now. China reportedly has instructed power stations and steel mills not to use Australian coal. Several months ago, Beijing weighed in against thermal coal, but now the “soft” ban includes coking coal, according to reports. This follows a ban on Australian barley, beef from five abattoirs, and an anti-dumping investigation into some Australian wines. |

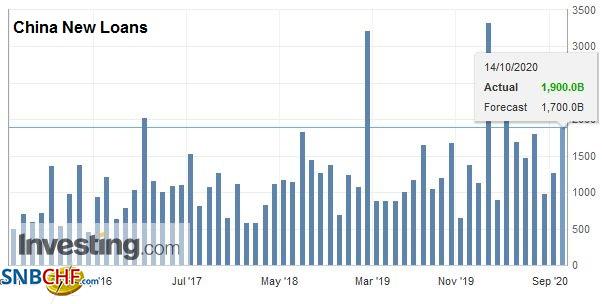

China New Loans, September 2020(see more posts on China New Loans, ) Source: investing.com - Click to enlarge |

Chinese banks boosted lending last month, while nonbanks pulled back, according to the latest figures. Bank loans jumped to CNY1.9 trillion in September from nearly CNY1.28 trillion in August. It is the most since March. Leaving the virus’s response aside and discounting the seasonal surges in January, the lending in September is the highest. On the other hand, nonbanks, or what is referred to as the shadow banks, slowed, and aggregate financing actually slowed to CNY3.48 trillion from CNY3.58 trillion in August. Separately, the PBOC’s money market operations saw it drain liquidity for the third consecutive session. The repo rate jumped, but the 10-year bond yield rose a couple basis points to new highs for the year above 3.20%.

The dollar remains, as it did yesterday, within Monday’s range against the Japanese yen (~JPY105.25-JPY105.85). So far today, it is in around a 10-tick range on either side of JPY105.40. There are $1.2 bln in expiring options between JPY105.15-JPY105.20. On the upside, there are about $1.9 bln in expiring options between JPY105.75 and JPY106.00. The Australian dollar held above yesterday’s $0.7150 low but the attempt to recover stalled in Europe a little above $0.7180. It needs to resurface $0.7200 to help the technical tone. There were concerns that the cut in the reserve requirements for currency forwards was a signal for a weaker yuan. The yuan did weaken on Monday but strengthened yesterday until the dollar’s broader strength pushed it slightly lower. Today, the PBOC set the dollar’s reference rate at CNY6.7473, a little stronger than the bank models suggested, and the market took the yuan higher. It’s nearly 0.2% gain today, the yuan is one of the strongest currencies against the dollar today.

Europe

The WTO confirmed the earlier ruling that Boeing received improper government assistance and can impose tariffs on up to $4 bln of imports from the US. It is not as much as Europe sought ($8.6 bln), and it is less than the $7.5 bln “awarded” the US for EU’s illegal assistance to Airbus. A range of consumer goods, including food, rum, and vodka, are targeted. The US has repealed the objectionable tax breaks, but the arbitrators said it was not sufficient to stay their decision. The dispute will continue, and it is not immediately clear that the US position would change regardless of the election outcome.

Brinkmanship requires going to the brink. And that is precisely where the UK and EU find itself on the eve of the summit and self-declared deadline by Prime Minister Johnson. The EU negotiator says not enough progress has been made to move the process to the next phase of codifying an agreement. The UK’s response was to reiterate its willingness to abandon the talks entirely. Short-date implied volatility roses, but from the three-month tenor and out it fell. Although there is no official word, reports based on a “person close to negotiations” said that Prime Minister Johnson will decide whether to go forward with talks after the summit, not before.

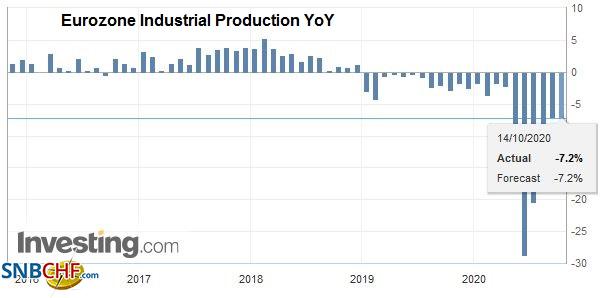

| Germany, France, and Spain had already reported disappointing August industrial output figures. It is hardly surprising that the aggregate report was weaker than expected. In the end, it rose by 0.7% after a revised 5.0% gain in July (initially 4.1%). Industrial production is 7.2% lower than a year ago, slightly more than in July. Meanwhile, there is an attempt in some press stories to play up the divergence of opinion at the ECB. While it cannot be denied, it also should not be exaggerated. The meeting later this month is not so controversial. There seems to be a strong consensus to wait for more information, including updated staff forecasts, available in December. |

Eurozone Industrial Production YoY, August 2020(see more posts on Eurozone Industrial Production, ) Source: investing.com - Click to enlarge |

The euro was not able to get much above the $1.1810 area, the (50%) retracement of the decline since September 1. It was sold to about $1.1730 yesterday and is seeing the losses extend in Europe today. A convincing break of $1.1700 weakens the technical tone. The initial target would be around $1.1665, but the $1.1600 area is the lower end of the three-month range. On Monday, sterling was flirting with a one-month high near $1.3080, the (50%) retracement of the decline since September 1. At $1.2920 yesterday, it was probing the three-week uptrend line. It was sold today a little below $1.2865 before recovering to session highs (~$1.2975) in the European morning following what appears to be a 48-hour respite in the UK threat to leave negotiations. However, it quickly retreated to little changed levels around $1.2930-$1.2950.

| America

The updated IMF forecasts for the US were of the good/bad news variety. The outlook for this year improved from the 8% contraction estimated in June to -4.3% now. The bad news is that the forecast for next year was cut by a third to 4.5%. The Bloomberg survey has a median estimate of a 4% contraction this year and 3.7% growth in 2021. Its forecasts for Canada were upgraded. Rather than contract by 8.4%, the IMF sees the Canadian economy shrinking by 7.1%, and next year, growth is seen reaching 5.2%. To round out the North American update, the IMF sees the Mexican economy contracting by 9% this year, better than the 10.3% decline forecast in June. The outlook for next year improved to 3.5% from 3.3%. |

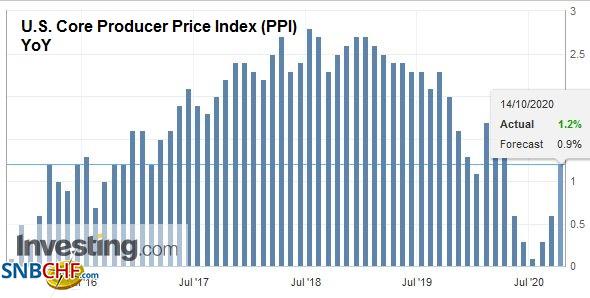

U.S. Core Producer Price Index (PPI) YoY, September 2020(see more posts on U.S. Core Producer Price Index, ) Source: investing.com - Click to enlarge |

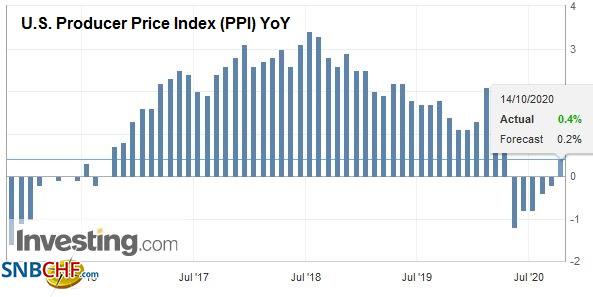

| US September CPI was spot on forecasts. The headline rate ticked up to 1.4%, and the core rate was steady at 1.7%. To appreciate why the core rate is steady, consider that a little more than half of the core basket is composed of two things: shelter and health care (services and products). Housing costs rose by 2% year-over-year, and health care is up nearly 5% over the past year. Food and energy account for a fifth of the CPI basket. Food prices, says the Bureau of Labor, are up almost 4%, and energy prices have fallen by 7.7%. The inflation focus shifts to producer prices today. Both the headline and core rates are expected to have risen by 0.2% in September. Such a rise would lift the headline rate above zero for the first time since March. The core rate may have risen to 1.0% from 0.6% in August. It would also be the highest since the 1.1% pace in March. |

U.S. Producer Price Index (PPI) YoY, September 2020(see more posts on U.S. Producer Price Index, ) Source: investing.com - Click to enlarge |

While Canada and Mexico have light economic diaries today, half a dozen Fed officials speak throughout the session. The US dollar rose to a three-day high of almost CAD1.3160 today, but the general tone is one of consolidation after falling 1.4% last week. For most of the last few days, the greenback has been confined to the lower end of last Friday’s range (~CAD1.3110-CAD1.3200). It is not going anywhere quickly. The US dollar is also consolidating against the Mexican peso. It has been registering slightly higher lows in recent sessions, but it remains well below last week’s high near MXN21.76. It appears to be a prelude to the next leg lower, which will likely see a retest on last month’s low (~MXN20.85), which is also a six-month low.

Full story here Are you the author?Tags: #USD,$CNY,Brexit,China,Currency Movement,ECB,Featured,newsletter,Trade,WTO