Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

The Yuan’s Quiet Rise and Next Week’s Summit

The Yuan’s Quiet Rise and Next Week’s Summit7 May 2026

Consolidation Featured, but the Yen and Mexican Peso are Under Pressure, While PBOC Fixed the Dollar Lower20 Sep 2024

Little Discussion about the US Budget Deficit in the Debate, But Falling Yields Drag the Greenback Lower11 Sep 2024

Greenback Consolidates Last Week’s Surge25 Mar 2024

Key Chart Points Hold and the Dollar’s Rally Stalls Ahead of the Weekend19 May 2023

Hawkish ECB Comments Boost Risk of a 50 bp Hike Next Month14 Apr 2023

Dramatic Swing in Sentiment Extends the Greenback’s Rally17 Feb 2023

US CPI Featured and Why the Fed may Still Hike by 50 bp7 Jan 2023

USD Stretched Ahead of Employment Report, while Yuan Jumps on Hopes of New Property Initiatives6 Jan 2023

The Yen and Yuan Continue to Weaken7 Sep 2022

Turn Around Tuesday Began Yesterday, Likely Ends before Wednesday30 Aug 2022

Dollar Longs Pared as Jackson Hole Gathering is set to Start

Dollar Longs Pared as Jackson Hole Gathering is set to Start25 Aug 2022

Wait A Sec, That’s Not Really An *RMB* Liquidity Pool…1 Jul 2022

Angry April TIC Zeroed In On China’s CNY and Japan’s JPY21 Jun 2022

Follow China’s True Line5 Jun 2022

Synchronized Not Coronavirus19 May 2022

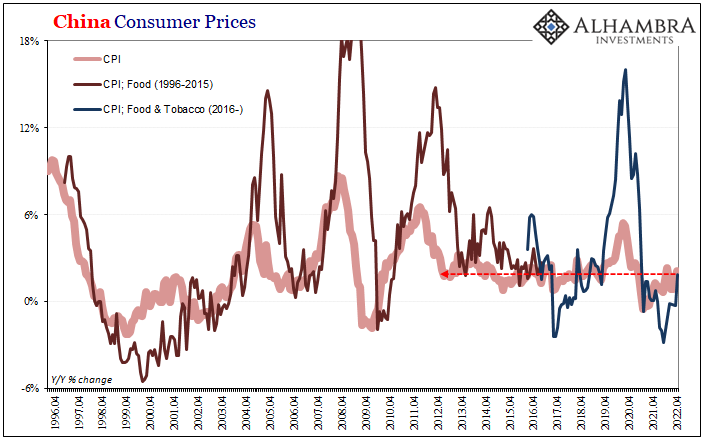

Synchronizing Chinese Prices (and consequences)14 May 2022

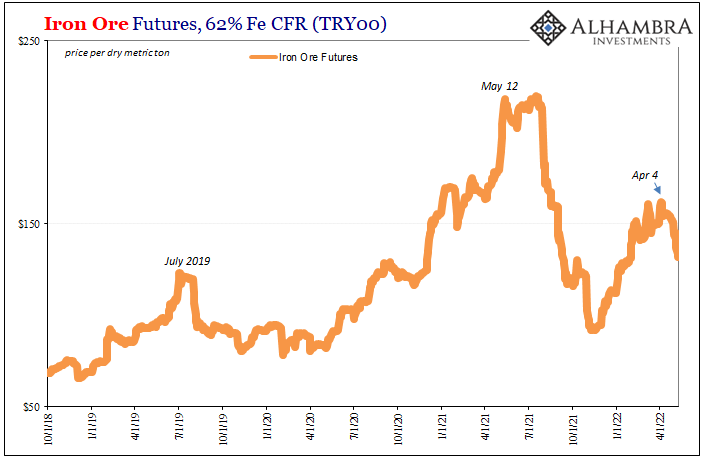

Industrial Synchronized Demand11 May 2022

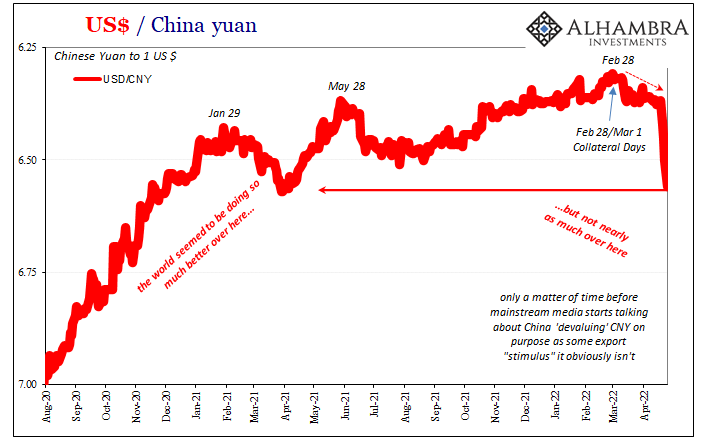

CNY’s Drop Wasn’t ‘Devaluation’ in ’15 nor ’18, and It Isn’t ‘Devaluation’ Now25 Apr 2022

The (less) Dollars Behind Xi’s Shanghai of Shanghai25 Apr 2022