Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

FX Daily, June 12: Licking Yesterday’s Wounds Today

FX Daily, June 12: Licking Yesterday’s Wounds Today12 Jun 2020

The global economy doesn’t care about the ECB (nor any central bank)14 May 2020

FX Daily, May 13: Will Powell have any more Luck Pushing against Negative Rate Expectations in the US?13 May 2020

FX Daily, April 16: Markets Brace for another Jump in US Weekly Jobless Claims16 Apr 2020

FX Daily, March 12: Trump Dump as Market Turns to ECB12 Mar 2020

FX Daily, February 12: The Greenback Slips in Subdued Activity12 Feb 2020

Two Years And Now It’s Getting Serious11 Feb 2020

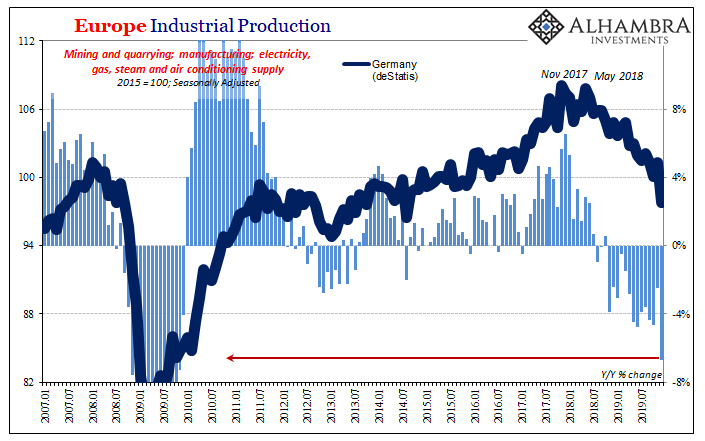

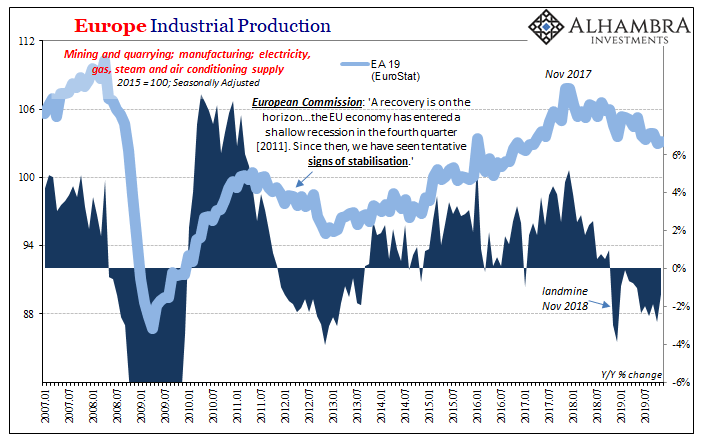

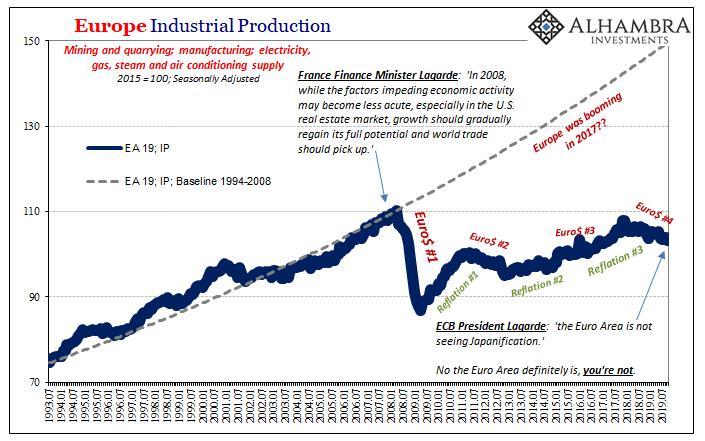

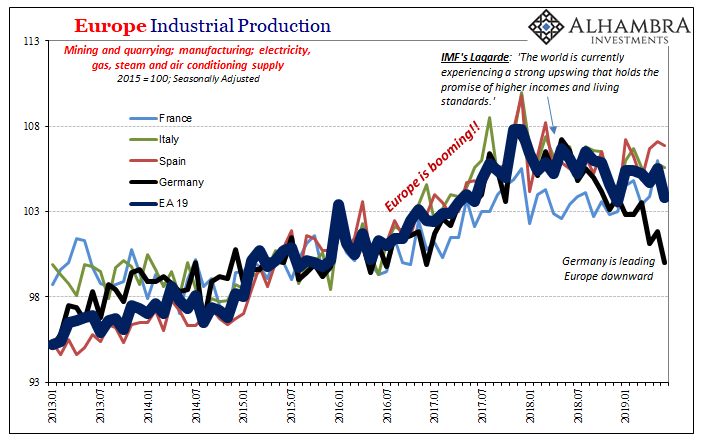

Germany, Maybe Europe: No Signs Of The Bottom19 Jan 2020

FX Daily, January 15: Phase 1 Trade Deal Shifts Terrain of US-China Rivalry15 Jan 2020

Lagarde Channels Past Self As To Japan Going Global14 Dec 2019

FX Daily, December 12: Enguard Lagarde12 Dec 2019

You Will Never Bring It Back Up If You Have No Idea Why It Falls Down And Stays Down10 Dec 2019

FX Daily, November 13: Investors Temper Euphoria13 Nov 2019

FX Daily, October 14: Optimism Took the Weekend Off14 Oct 2019

The Scientism of Trade Wars11 Oct 2019

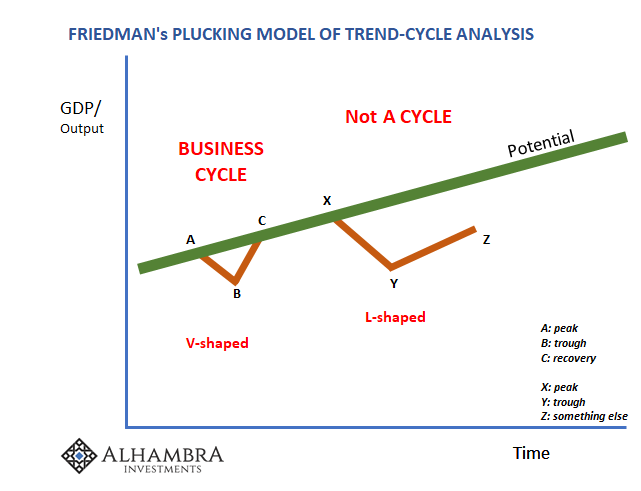

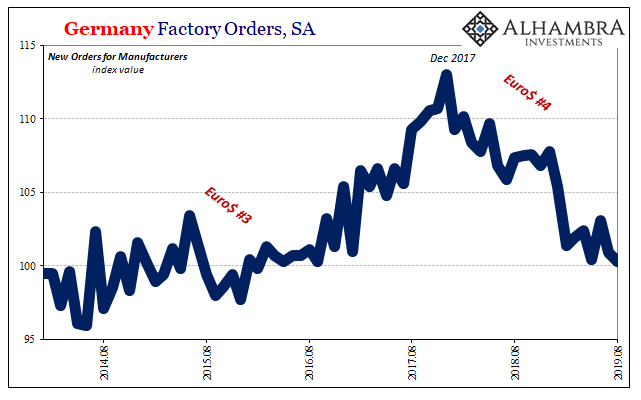

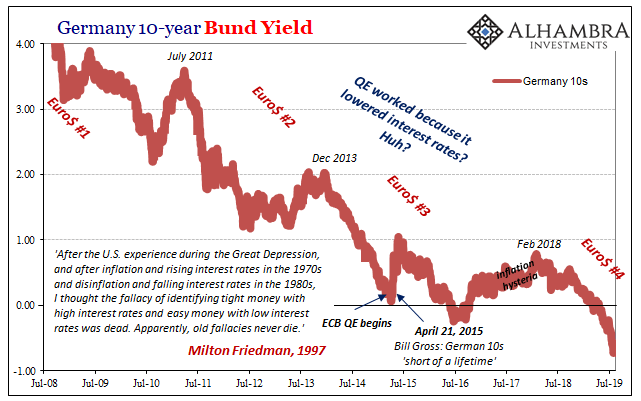

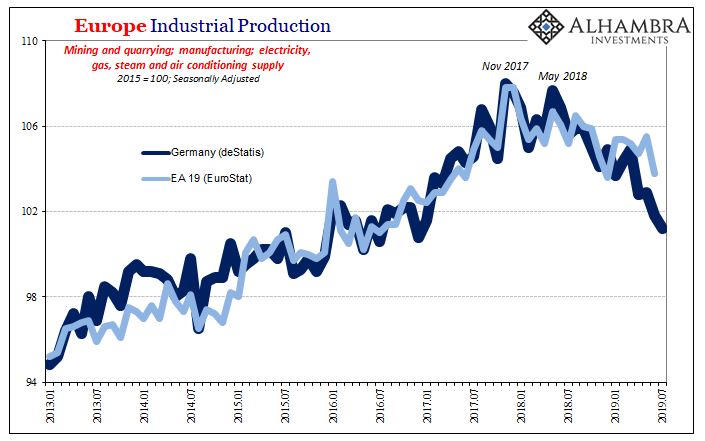

The Obligatory Europe QE Review13 Sep 2019

FX Daily, September 12: Focus on the ECB, while the Dollar Slips below CNY7.0912 Sep 2019

A Bigger Boat11 Sep 2019

Some Brief European Leftovers18 Aug 2019

FX Daily, August 14: Markets Paring Exaggerated Response to US Blink

FX Daily, August 14: Markets Paring Exaggerated Response to US Blink14 Aug 2019