Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has fallen by 0.13% to 1.0914 |

EUR/CHF and USD/CHF, September 12(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Some gestures in the US-China trade spat have given the market the reason to do what it had been doing, and that is taking on more risk. Equities are higher in Asia Pacific and opened in Europe higher before slipping. The MSCI Asia Pacific and the Dow Jones Stoxx 600 are advancing for the fourth consecutive week. US shares are firmer in European trade, and the S&P 500 will test the air above 3000 today. Its rally is lifting the benchmark for the third consecutive week. Benchmark 10-year bond yields, which have jumped since the start of the month, are consolidating mostly one-to-two basis points lower today, with market-sensitive ECB meeting and US CPI on tap. The dollar is softer against nearly all major and emerging market currencies. Among the majors, the exception is the Japanese yen, which is a little softer. The dollar poked through JPY108 for the first time in over a month. Among emerging markets, the Turkish lira is a laggard ahead of the central bank meeting where another large rate cut is expected shortly before the ECB statement. |

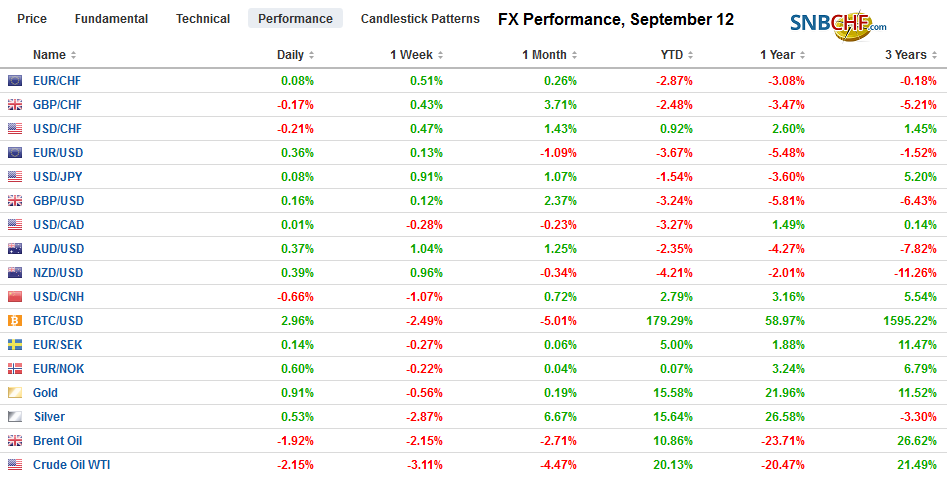

FX Performance, September 12 - Click to enlarge |

Asia Pacific

Shortly before the Asian markets opened, President Trump said he would delay the increase of the 25% tariffs to 30% from October 1 to October 15. The US President cited a request by the Vice Premier of China, due to the anniversary of the revolution. However, after Trump took “poetic license” recently to claim that Chinese officials called wanting to resume negotiations, this must be taken with a grain of salt. It is our understanding that the delay in the tariff increase was part of the quid pro quo for China to buy US agriculture products (soy and pork) ahead of the face-to-face talks that are planned for some time next month. The US and China have announced exemptions to the tariffs but rather than a signal of goodwill, it reflects the needs of domestic actors.

The dollar is trading at its lowest level against the yuan in three and a half weeks, below CNY7.09. The overnight repo rate has fallen sharply in recent sessions. It was at 2.60% on Monday and is now at 2.36%. A couple days after the FOMC meets next week when it is expected to deliver its second rate cut of the year, the PBOC will set its prime lending rate, and expectations are for a cut. Note that Chinese markets are closed tomorrow. The Shanghai Composite gained 1% this week and follows a nearly 4% rally last week and is the fourth week in the past five that it advanced.

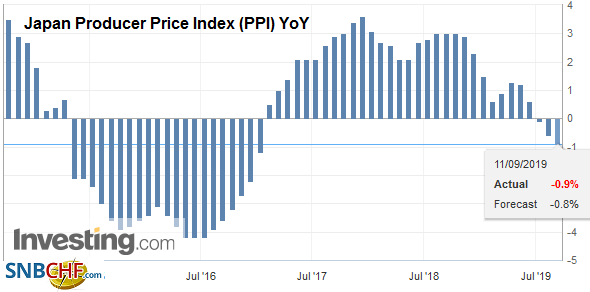

| Japan reported a series of mixed economic data. Yesterday’s China’s weak PPI was highlighted as a deflationary signal. Today Japan reported a 0.3% decline in the August PPI that brought the year-over-year rate to minus 0.9% from minus 0.6% in July. July core machinery orders fell 6.6%, which follows a 13.9% surge in June. The drop was not as much as most economists expected. Separately, Japan reported its July tertiary index edged 0.1% higher. The median forecast in the Bloomberg survey was for a 0.3% decline. It was the first increase since April. Separately, the roughly 3.5% decline in the yen since its low in late August will take some pressure off the BOJ, which meets next week. Still, many expect the BOJ may adjust its Yield Curve Control in recognition that the 10-year bond yield is beyond the minus 20 bp lower band. |

Japan Producer Price Index (PPI) YoY, August 2019(see more posts on Japan Producer Price Index, ) Source: investing.com - Click to enlarge |

The dollar reached almost JPY108.20 in the Tokyo morning before pushing lower. It found support near JPY107.80 in early European turnover. It is the fourth consecutive session the dollar is advancing, the longest streak in two months. On the upside, the JPY108.45 area corresponds to a (50%) retracement of the losses since the year’s high in April of roughly JPY112.40. A break of JPY107.60 might suggest a near-term top is in place. The Australian dollar has edged to a marginal new six-week high, just shy of $0.6890, but there is not much momentum. It is not clear that it has convincingly broken out of the consolidative range that has been seen since the start of the week. Overhead resistance is seen in the $0.6900-$0.6930 area. Initial support is likely around the week’s low (~$0.6935-$0.6940).

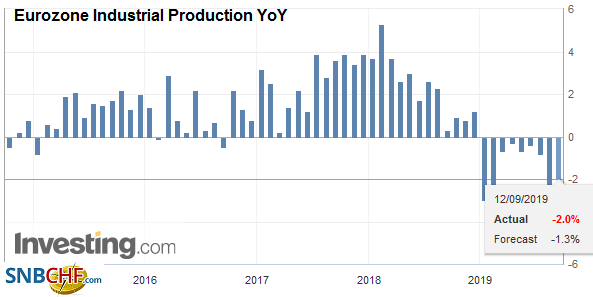

EuropeThe ECB’s policy response ought to be proportionate to its challenge in meeting its legally imposed mandate, so the argument goes, even though it chose its own technical definition of price stability. The new staff projections will likely cut growth and inflation forecasts. The exogenous shock of a disruptive Brexit remains a highly probable scenario and one that will be increasingly incorporated into 2020 budget assumptions (e.g., Ireland). The market feels most confident of a 10 bp rate cut that would bring the deposit rate to minus 50 bp. It is less confident of a new asset purchase program, primarily because 1) some creditors/hawks (e.g., German and Dutch ECB members) pushed back against the idea and 2) there is a sense in some quarters that monetary policy is exhausted. Quantitative easing would have never taken place if the creditors had had their way. The ECB does not appear to subscribe to the thesis that monetary policy is exhausted, but Draghi has been a persistent advocate that those countries with fiscal space (i.e., Germany and the Netherlands) should use it. Most observers who anticipate a resumption of bond purchases envision a 12-month program that purchases around 30-40 bln euros a month. Some adjustment to position limits may be required. |

Eurozone Industrial Production YoY, July 2019(see more posts on Eurozone Industrial Production, ) Source: investing.com - Click to enlarge |

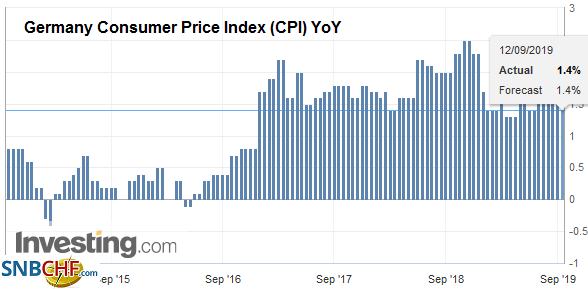

| Tiering, or exempting some types of deposits at the central bank from negative rates may dilute the full impact of the rate cut, and but be a useful compromise to preserve the loose consensus type of decision-making. Although there is a system of rotating voting power, not so dissimilar to the FOMC, we are under the impression that formal voting is not necessary. We suspect that if an asset purchase program is not announced or indicated that it will be announced shortly, investors will be disappointed, forcing a backing up of yields. Whatever succor the euro may draw from higher yields may be short-lived. There may be some ways that Draghi could build on the knowledge that his successor (Lagarde) Lagarde seems to promise policy continuity for adjusting forward guidance. This would be in stark contrast to when Draghi took the helm and quickly reversed Trichet’s rate hikes. |

Germany Consumer Price Index (CPI) YoY, August 2019(see more posts on Germany Consumer Price Index, ) Source: investing.com - Click to enlarge |

One of the battles UK Prime Minister Johnson lost with Parliament last week was that the government was forced to publish its projections of what could happen on a no-deal Brexit. The 12-page document was released yesterday, and it would frankly make a nice pilot of an apocalypse script for a TV series. Operation Yellowhammer outlines the social chaos that may result, possible food and fuel shortages, and pubic disorder. It estimates that as much as 85% of the trucks Dover-Calis straits may not be prepared for new customs. The report projected that even after three-months, the disruption would still be evident. Medicines were “particularly vulnerable” in the government’s estimate. Some cannot be stockpiled, and others cannot be sufficiently accumulated to cover what could be delayed “for up to six months”. There could be clashes between UK and EU fishing fleets. The report highlights the pressure that will be exerted on the government to re-establish negotiations.

The euro slipped through $1.10 yesterday but has remained above there today. The euro has risen to a little through $1.1030 today, but the intraday technical studies warn that it may not get much further. Resistance is seen in the $1.1040-$1.1050 area. That said, the one thing that market participants can count on its that the price action will turn more dramatic after the ECB meeting. There are a few chunky options that expire shortly after Draghi’s press conference to note. There are options for 1.5 bln euros at $1.10 and almost 700 mln at $1.0975. There is also an option for a little more than 865 mln euros at $1.1055 that will be cut. Sterling remains in the range seen on Monday (~$1.2235-$1.2385), and it is in a roughly $1.2315-$1.2345 range today. There is an option that will be cut today for nearly 500 mln euros struck at GBP0.8945, which is where the cross is as this is being written. The dollar is trading near a three-day low against the Turkish lira ahead of the central bank’s decision. The median forecast in the Bloomberg survey was for a 275 bp cut in the one-week repo rate to 17.0%. This follows a 425 bp cut in July. Given that inflation is falling faster than expected and that there were no sustained adverse reactions to the previous cut, we suspect the risk is for a larger reduction today than the market anticipates.

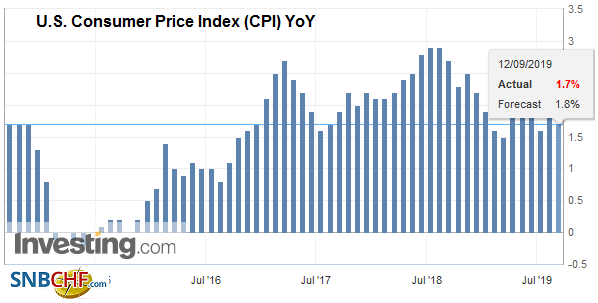

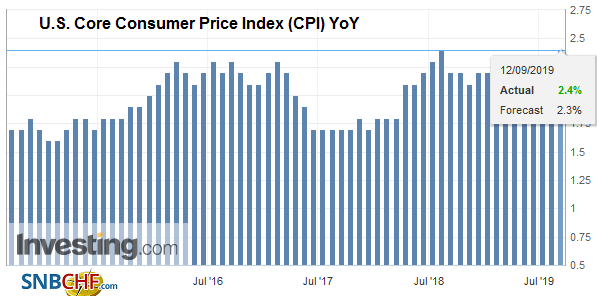

AmericaWhile Draghi’s press conference is underway, the US will report August CPI. Recall that in July the headline and core rate rose by 0.3% for the second consecutive month. That is not expected to be repeated in August, where the median forecasts look for a 0.1% and 0.2% increase respectively for the headline and core rates. It would allow the year-over-year pace to be steady at 1.8% at the headline and tick up to 2.3% for the core. The data is unlikely to impact expectations for next week’s FOMC meeting where a 25 bp cut is understood to be the most likely outcome by far. |

U.S. Consumer Price Index (CPI) YoY, August 2019(see more posts on U.S. Consumer Price Index, ) Source: investing.com - Click to enlarge |

| President Trump again lambasted the Fed for not easing rates more aggressively and even provocatively called for negative rates. Although many economists, including former Fed chair Greenspan, have suggested that it is just a matter of time before negative rates are seen in the US, we remain skeptical, and comments by a number of Fed officials suggest that there is little interest there. We are not convinced that negative interest rates have proven to be successful. To the extent that there have been some benefits, we suspect the cost would be too great in the US. That means that the Fed will likely see alternatives, should the zero-bound be approached again. |

U.S. Core Consumer Price Index (CPI) YoY, August 2019(see more posts on U.S. Core Consumer Price Index, ) Source: investing.com - Click to enlarge |

News that President Trump had considered easing sanctions on Iran, which was what ostensibly was the last straw that led to Bolton’s departure, sparked a sharp (~2.9%) drop in the price of October WTI yesterday. Iranian oil has been stored in bonded facilities in China and should the sanctions be lifted, then the risk is for considerably lower oil prices as this overhead supply enters the market. On the other hand, US oil inventories fell nearly 7 mln barrels, and at 416.1 mln barrels, the US commercial inventories are about 2% below the benchmark five-year average, for the first time this year. Also of note, oil imports have averaged about 6.7 mln barrels a day for the past four weeks, which is a nearly 12% reduction year-over-year. Lastly, we note that market-based measures of inflation expectations such as the five-year forward-forward or the breakevens (the spread between the yield of the conventional bond and the inflation-linked security) are particularly sensitive to oil prices.

The Canadian dollar ended a three-day rally yesterday and weakened by about 0.3%. The US dollar recovered from about CAD1.3130 to nearly CAD1.3215. It fell short of the (38.2%) retracement of the drop seen the start of the month when the Bank of Canada was not as dovish as the market expected (~CAD1.3230). Above there, the next retracement is seen near CAD1.3260, which is also where the 20-day moving average is found. The dollar has carved a shelf near MXN19.47 this week, which is a little above the (61.8%) retracement objective of the dollar’s rally from the end of July. Below there, support is seen near MXN19.35 and then MXN19.30, where the 200-day moving average is found. Late in the session, Argentina reports August CPI figures. The median forecast in the Bloomberg survey is for a 4.4% increase on the month after a 2.2% rise in July. It would lift the year-over-year to 55.4% from 54.40%. The US dollar ended a seven-week climb against the peso last week with a 6.6% drop. The dollar edged higher for the past three sessions but has only gained about 0.6%.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,ARS,Brexit,EUR/CHF,Eurozone Industrial Production,Germany Consumer Price Index,Japan Producer Price Index,newsletter,Turkey,U.S. Consumer Price Index,U.S. Core Consumer Price Index,USD/CHF