Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

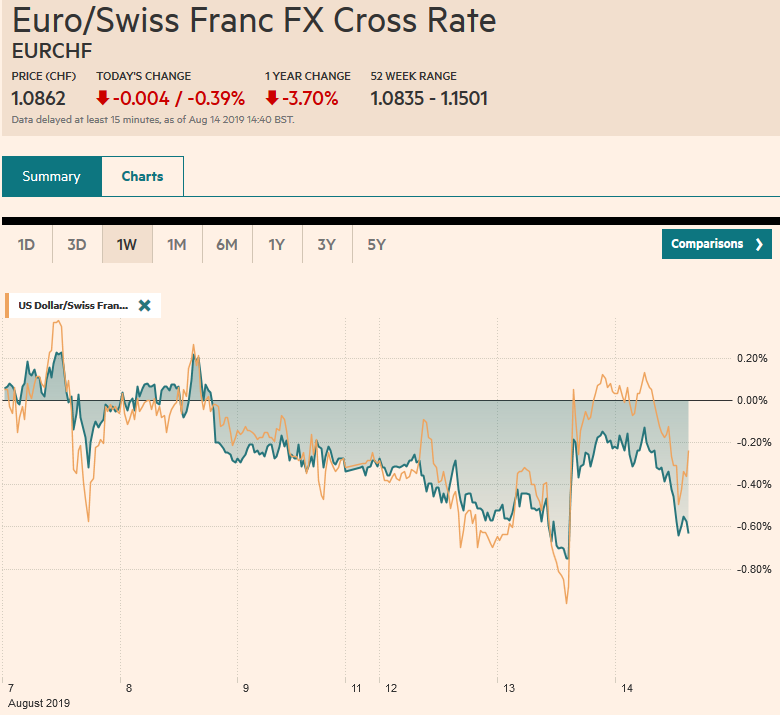

Swiss FrancThe Euro has fallen by 0.39% to 1.0862 |

EUR/CHF and USD/CHF, August 14(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

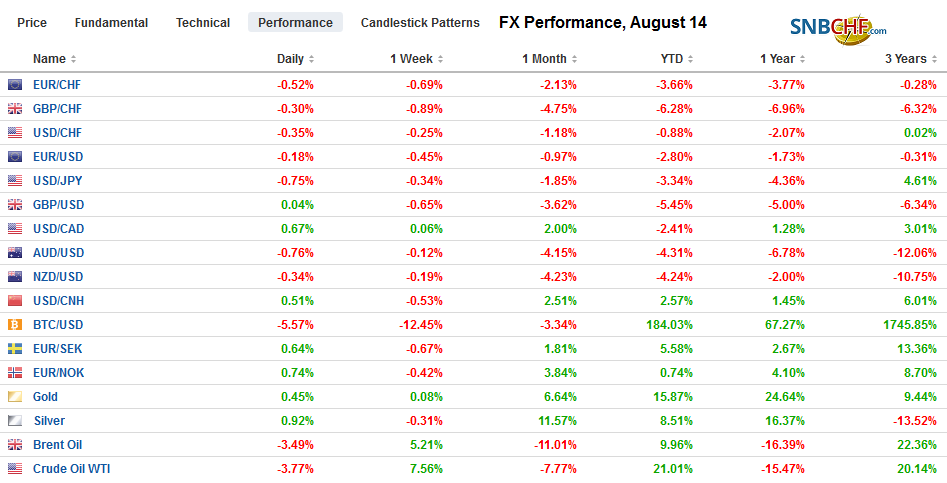

FX RatesOverview: The US cut its list of Chinese goods that will be hit with a 10% tariff at the start of next month by a little roe than half, delaying the others until the mid-December. This spurred a near-euphoric response by market participants throughout the capital markets. However, as the news was digested, it did not seem as much of a game-changer as it may have initially. Disappointing Chinese data also seemed to encourage risk-off. Asia Pacific equities had a muted response to the reversal higher in US stocks yesterday, and the Dow Jones Stoxx 600 is seeing most of yesterday’s gains unwound. US shares are trading with a heavier bias in the European morning. The rise in US yields yesterday helped keep Asia Pacific yields firm, but US 10-year yield surrendered yesterday’s gains, and European benchmark 10-year yields are off one-two basis points. The dollar is mixed. The dollar-bloc and Scandis are heavier, while the yen, Swiss franc and euro enjoy a firmer tone. Among emerging market currencies, Asian currencies did well, perhaps helped by the strengthening of the yuan. The Singapore dollar was an exception by moving lower. The more volatile, and accessible emerging market currencies like the Russian rouble, South African rand, Turkish lira, and Mexican peso are nursing losses. |

FX Performance, August 14 - Click to enlarge |

Asia Pacific

The PBOC set the dollar’s reference rate at CNY7.0312, which was weaker than the models suggested (VNY7.041). The greenback reached an eight-day low near CNY7.01. While part of this could be a signal after the US trade move, but, as noted yesterday, China cannot afford to have the yuan be perceived as a one-way bet, and the slowing momentum was evident.

China’s economic reports were weaker than expected, which underscore the likelihood of a policy response. Industrial output slowed to a 17-year low of 4.8%. The market had anticipated something closer to 6%, which is where it was in July 2018, and after a 6.3% year-over-year pace in June. Retail sales slowed from a 9.8% year-over-year increase in June to 7.6%. Fixed investment edged lower to 5.7% from 5.8%. The general sense is that while the trade conflict with the US is weighing on activity, the world’s second-largest economy also appears to be moderating due to its own internal dynamics.

Japan reported that its tertiary index slipped 0.1% in June, but that sector as behind the surge in core machinery orders. Non-manufacturing core machine orders surged 30.5%, bolstered by demand from the estate industry, postal and delivery services. Orders from the manufacturing sector fell 1.7%, which was more in line with expectations.

The dollar jumped yesterday from JPY105 to JPY107. Japanese accounts took advantage of the rally to sell dollars at better levels and drove the greenback to about JPY106.25. It has consolidated in the European morning near JPY106.50, where a $475 mln option expires today. There are nearly $1.1 bln in options struck between JPY105.80-JPY106.00 that roll off today and almost $500 mln at JPY107.00. These levels also correspond to retracements of yesterday’s dollar rally (61.8% and 50% respectively). The Australian dollar briefly poked above $0.6800 yesterday but was unable to make more headway today. The risk extends to the lows from the past two sessions near $0.6745, but the intraday technical are overextended as North American traders return to their posts. A large A$1.2 bln expiring options at $0.06790 may be in play.

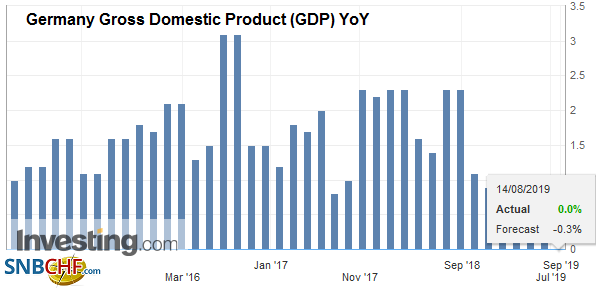

EuropeGerman GDP contracted by 0.1% in Q2, which was in line with expectations, though we saw the risk on the downside after a series of disappointing reports. It was the second quarterly contraction in the past four quarters. While this does not meet the rule of thumb definition of a recession (two consecutive quarterly declines), it surely illustrates the challenges facing Europe’s largest economy. The weakness seems to be softening Germany’s reluctance to use fiscal policy, though the unpopular Solidarity tax will end for most shortly. |

Germany Gross Domestic Product (GDP) YoY, Q2 2019(see more posts on Germany Gross Domestic Product, ) Source: investing.com - Click to enlarge |

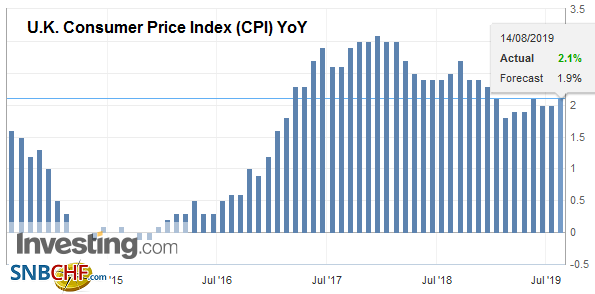

| The UK reported firmer than expected consumer prices. CPIH, which includes own-occupied housing costs, rose to 2.0% from 1.9%. Economists had expected a tick lower to 1.8%. |

U.K. Consumer Price Index (CPI) YoY, Jul 2019(see more posts on U.K. Consumer Price Index, ) Source: investing.com - Click to enlarge |

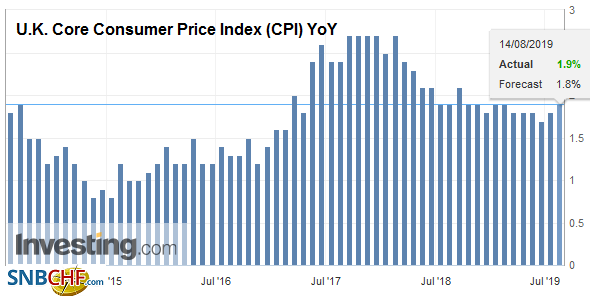

| This matches the high from last November and follows on the heels of the employment report that saw a stronger than expected increase in average weekly earnings (3.7% three-months year-over-year). Despite the rising pressures, and the decline in sterling, which contains inflation risks as well, the market is still pricing in strong chances of a rate cut late this year or early next. |

U.K. Core Consumer Price Index (CPI) YoY, July 2019(see more posts on U.K. Core Consumer Price Index, ) Source: investing.com - Click to enlarge |

| Italy’s political drama is gradually playing out. The vote of confidence required by the League’s withdrawal of support is unlikely to take place this week as Salvini wanted. Now it appears Prime Minister Conte will address Parliament on August 20, and a vote of confidence will likely follow, though the situation still seems fluid. Conte could resign, for example, or there could be further delays. Italian stocks and bonds continue to underperform. |

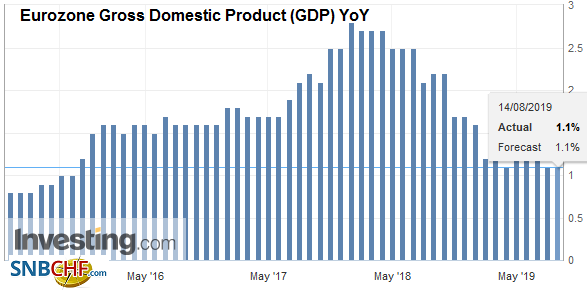

Eurozone Gross Domestic Product (GDP) YoY, Q2 2019(see more posts on Eurozone Gross Domestic Product, ) Source: investing.com - Click to enlarge |

| The euro reached a low to start the week a little above $1.1160. It retested it today on a little follow-through selling after yesterday’s retreat. Resistance is seen in the $1.1180-$1.1200 area. Sterling traded in a range of roughly $1.2015 to $1.2105 on Monday, and it remains confined to that range. The intraday technicals suggest the odds favor the range holding today. Sterling is posting gains against the euro for the third day running. If sustained it would be the long such streak in a month and threatens to end the historic 14-week slide. |

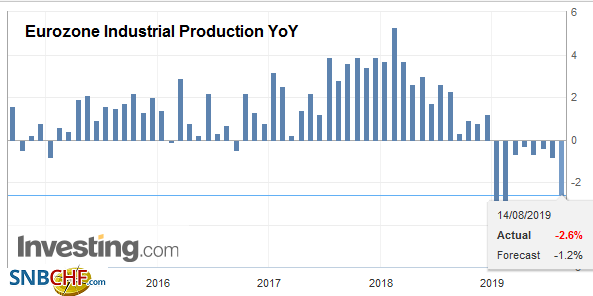

Eurozone Industrial Production YoY, June 2019(see more posts on Eurozone Industrial Production, ) Source: investing.com - Click to enlarge |

America

The US decision to break its new tariff increase into two parts saw the markets respond dramatically, but the shine is off today. Contrary to speculation, it does not appear that the US apparent concession was part of a quid pro quo. The US decision also showed two contradictions. First, Trump has been arguing that the tariffs were paid by the Chinese, though few if any believed that. The decision to remove a host of popular consumer products from the levies that will be imposed next month so as not to be a factor in holiday sales. The seems to be an admission of the obvious: American consumers pay the import tax. The second contradiction is that if a disruption of the holiday sales was the key to the decision, why would the tariff on the second batch of goods kick in ten days before Xmas? Some suggest that slide in the US stock market spooked the administration that often cites it as a key metric of its performance.

The US moves follow on the heels of the IMF’s Article IV review that threw down the gauntlet and contradicted America’s claim that China was manipulating its currency. As the IMF had indicated that this was its assessment last month, US officials must have known this before it labeled China. The US actions included removing bibles and shipping containers altogether from the list of products that will be taxed, and taxing the earbuds but not Iphones to which they are associated, seems whimsical and makes US policy look feckless. Trump accuses China of maybe wanting to wait for a Democrat to negotiate with, but this is self-servicing political spin. We see the Democrat leaders touting a tough line on China, and in some areas, like Huawei, even more aggressive than the Trump Administration. If China prefers a different US administration, perhaps it is that the current one seems unpredictable and inconsistent. Trade talks might not be completely derailed, but 1) there does not appear to be much urgency as next set of negotiations are scheduled in a couple of weeks and 2) expectations for an agreement are slim to none.

The US economic diary features July import and export prices today. The report is not typically a market mover. Tomorrow, the US reports August Empire and Philly Fed surveys, July retail sales, and industrial production. For the most part, sequentially softer data is expected. No Fed officials are scheduled to speak, though the FOMC minutes from the July meeting that cut the target rate by 25 bp will be released next week. Fed comments, especially from the doves are awaited, after the CPI figures that showed a 3-month annualized core rate of 2.8%. The back-to-back 0.3% monthly rise in the core rate was the strongest two-month performance in a decade.

The US dollar is recovering from testing the 20-day moving average against the Canadian dollar yesterday (~CAD1.3175). It has firmed toward the middle of yesterday’s range in Europe. The intraday technicals are getting stretched as the US dollar approaches CAD1.3250. Only a convincing move above the CAD1.33, which has capped the greenback recently on a closing basis and is where the 200-day moving average is found. The Mexican peso also recovered yesterday as part of the risk-on move after the US tariff announcement. The dollar found support near the 200-day moving average (~MXN19.36). Initial corrective targets are found in the MXN19.52-MXN19.56 area. Tomorrow the central bank meets. The odds of a 25 bp cut to 8.25% has risen this month. It stands around 22% now, up from 3% at the end of July.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,Currency Movements,EUR/CHF,Eurozone Gross Domestic Product,Eurozone Industrial Production,Germany Gross Domestic Product,newsletter,Trade,U.K. Consumer Price Index,U.K. Consumer Price Index,U.K. Core Consumer Price Index,USD/CHF