Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

FX Daily, June 9: Profit-Taking Gives Turn Around Tuesday Its Name

FX Daily, June 9: Profit-Taking Gives Turn Around Tuesday Its Name9 Jun 2020

FX Daily, May 15: Much Talk but Little Action15 May 2020

FX Daily, March 10: Markets Stabilize after Body Blow10 Mar 2020

FX Daily, February 14: Investors Continue to Look Past the Coronavirus

FX Daily, February 14: Investors Continue to Look Past the Coronavirus14 Feb 2020

FX Daily, November 14: Unexpected German Growth Fails to Buoy the Euro14 Nov 2019

Steady euro area growth and rise in core inflation4 Nov 2019

FX Daily, October 31: No Good Deed Goes Unpunished31 Oct 2019

FX Daily, August 14: Markets Paring Exaggerated Response to US Blink

FX Daily, August 14: Markets Paring Exaggerated Response to US Blink14 Aug 2019

FX Daily, July 31: Sterling Steadies, Attention Shifts to FOMC31 Jul 2019

Germany Struggles On25 Jul 2019

FX Daily, June 6: US Tariff Threats on Mexico Compete with ECB for Attention6 Jun 2019

FX Daily, May 15: Angst Continues15 May 2019

What’s Germany’s GDP Without Factories9 May 2019

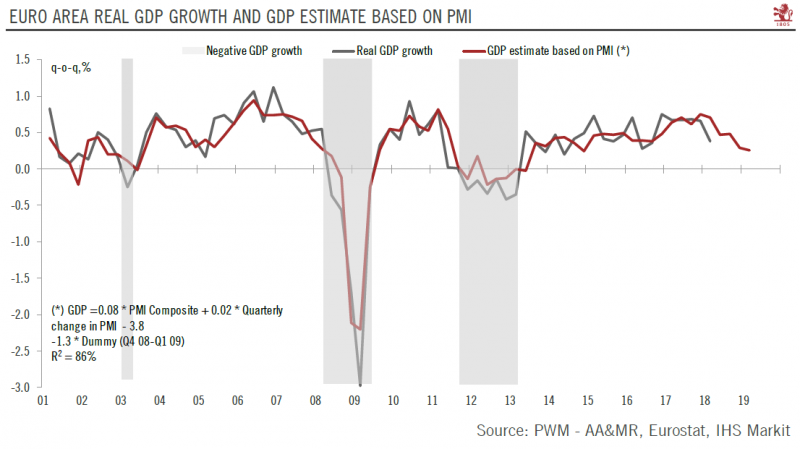

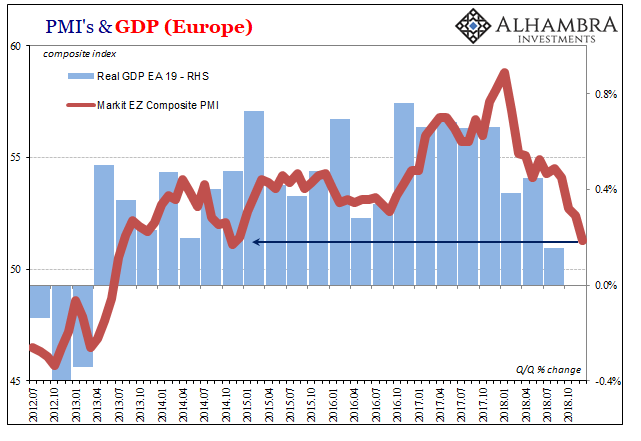

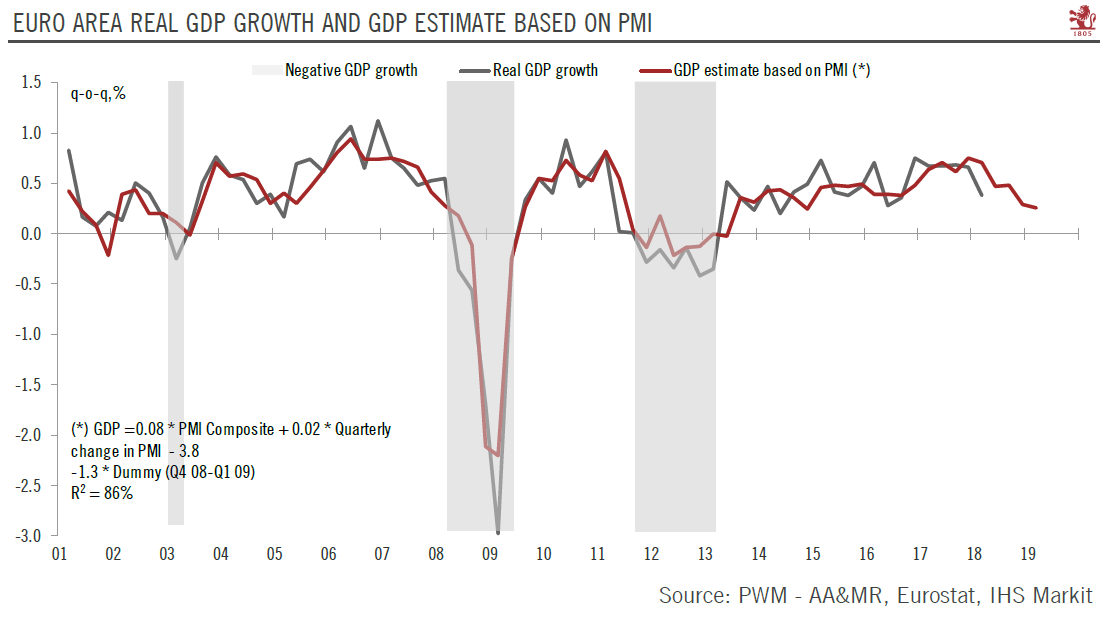

Update on euro area economic activity

Update on euro area economic activity25 Jan 2019

Just In Time For The Circus26 Dec 2018

The Direction Is (Globally) Clear29 Nov 2018

Global PMI’s Hang In There And That’s The Bad News25 Aug 2018

The Currency of PMI’s27 May 2018

What Really Happened In Europe10 May 2018

FX Daily, May 02: Confident Fed Key to New Found Respect for the Dollar

FX Daily, May 02: Confident Fed Key to New Found Respect for the Dollar2 May 2018