Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

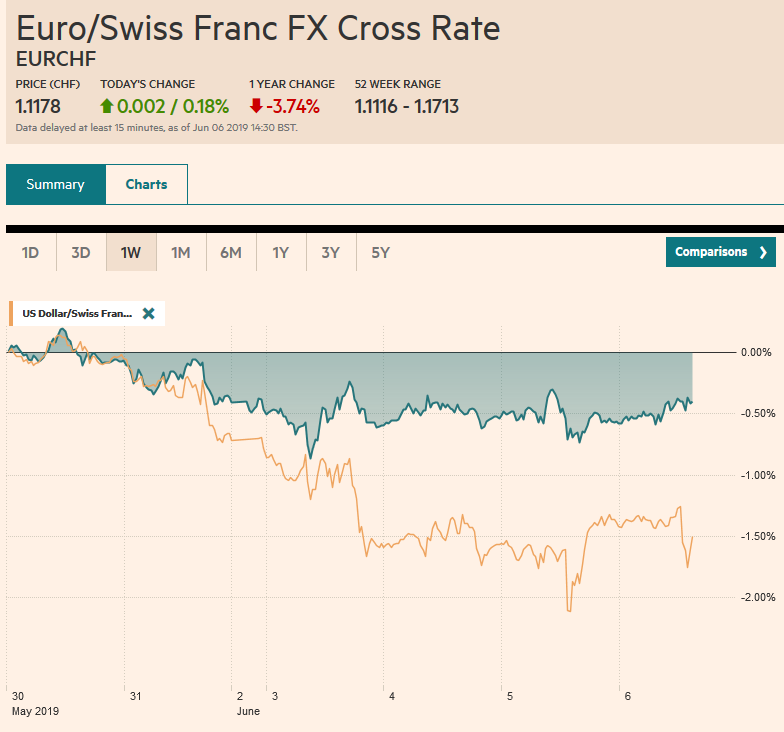

Swiss FrancThe Euro has risen by 0.18% at 1.1178 |

EUR/CHF and USD/CHF, June 06(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The implications of President Trump’s assessment that there has not been “nearly enough” progress in negotiations with Mexico that would avert the tariff on June 10 competing for investors’ attention, which had been squarely today’s ECB meeting. Minutes before Trump spoke Fitch cut its sovereign rating for Mexico to BBB from BBB+, while Moody’s cut its outlook to negative from stable. The risk-off mood was seen in Asia, where most equity markets fell, though Hong Kong, Korean, and Australian equities advanced. Indian stocks fell over 1% despite the central bank cutting the repo and reverse repo rates by 25 bp (to 5.75% and 5.50% respectively.) The Shanghai Composite also fell by more than 1%. It was the sixth consecutive decline. European markets are faring better, and the Dow Jones Stoxx 600 is extending its advance into a fourth session. Benchmark 10-year yields are mostly lower. Italy is underperforming following the EU’s warning on the country’s debt. The US 10-year yield is off around three basis points to 2.10%. The dollar is softer against all of the major currencies but sterling. Central and Eastern European currencies are firmer, while the Turkish lira, South African rand, and Chinese yuan are lower. The Mexican peso is stabilizing at lower levels. Oil prices are stabilizing after yesterday’s slide that was spurred by a surge in US inventories (22 mln barrels of crude and fuel). Gold is higher for the sixth consecutive session, and it has risen for 10 of the past 11 sessions. It approached $1345 yesterday, just shy of the year’s high seen in February. |

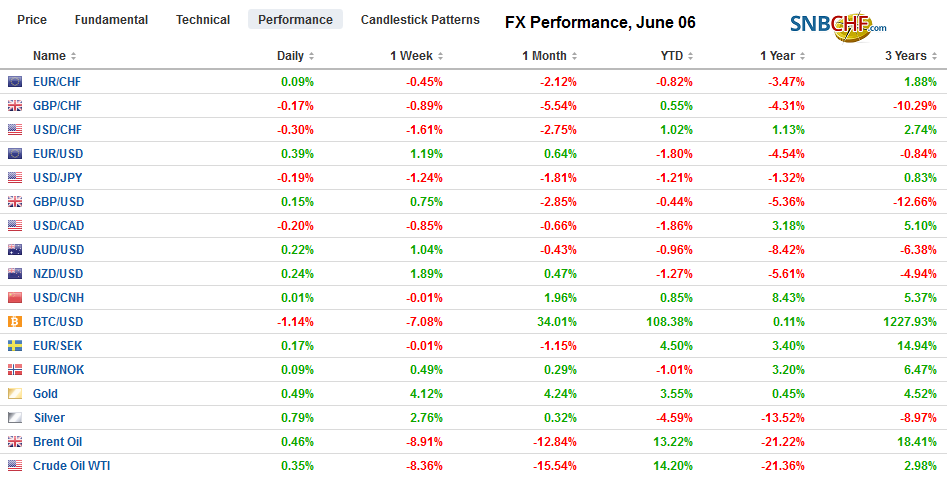

FX Performance, June 06 - Click to enlarge |

Asia Pacific

The trade tension with China is not deterring the US from pursuing policies that will antagonize China further. Reports suggest the US is close to striking a $2 bln arms deals with Taiwan that include state-of-the-art tanks, anti-aircraft and anti-armor weapons. It is not clear whether the F-16 fighter jets will be included in this or a subsequent deal. China will protest this, but there is little it can do, even though the US recognizes that Taiwan is a province of the PRC. Aid to Venezuela might be part of China’s counter, but the deteriorating economic prospects have led Russia to scale back its military presence as the Maduro government cannot afford to pay as much for protection.

The dollar is trading within yesterday’s range against the yen (~JPY107.80-JPY`108.50). It is the first session this week that the greenback has not yet been below JPY108.00, where a $2.8 bln expiring option is struck. There are $2.4 bln in options struck at JPY108.25 that also will be cut and $2.1 bln at JPY108.50. The dollar has fallen against the yen for six of the past seven weeks. It closed last week near JPY108.30. The Australian dollar reversed lower yesterday, failing to establish a foothold above $0.7000. However, buyers reemerged near $0.6965, but another run at $0.7000 may be difficult ahead of the US jobs report tomorrow.

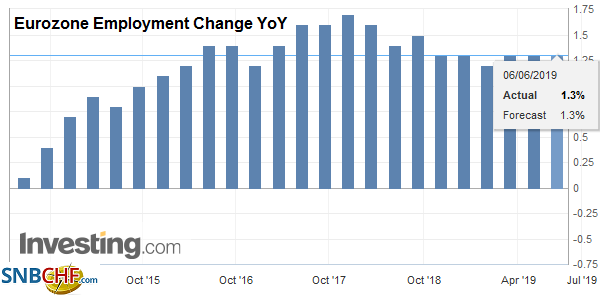

EuropeThe ECB cannot be happy. External risks have not diminished. Indeed, since it met last, the risks of a no-deal Brexit and escalation in trade tensions have increased. On top of this, price pressures have eased and at 1.2% in May was the lowest in a year. About a third of this increase is due to food and energy prices, putting the core at 0.8%. For all the effort, the core rate bottomed at 0.6% in January 2015. |

Eurozone Employment Change YoY, Q1 2019(see more posts on Eurozone Employment Change, ) Source: investing.com - Click to enlarge |

| The risks are to the downside, and the staff forecasts may be tweaked lower. The ECB is expected to provide more details about the new loan facility. A negative rate associated with the targeted lending would be most beneficial to those banks who have used this facility the most in the past, and that is understood to be in the south. The market appears to be discounting the chances of a 10 bp rate cut in about a year’s time, and at least one European bank predicted a resumption of asset purchases next year, under a new ECB president. |

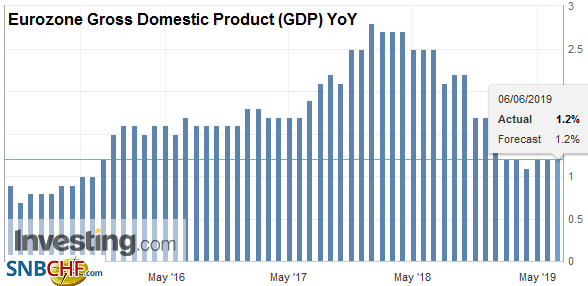

Eurozone Gross Domestic Product (GDP) YoY, Q1 2019(see more posts on Eurozone Gross Domestic Product, ) Source: investing.com - Click to enlarge |

Germany appears to be gradually improving. Yesterday, the May composite PMI was confirmed at a three-month high, which was a bit better than the flash estimate. Today it reported an unexpected increase in April factory orders. They were expected to be flat after a 0.6% increase in March. Instead, they rose 0.3%, and the March series was revised to show a 0.8% increase. That said, domestic orders actually fell 0.8%, while foreign orders rose 1.1%.

The euro posted a key reversal yesterday. After making new highs for the move, trading above $1.13 briefly for the first time since mid-April, it reversed course and closed below the previous day’s low (a little below $1.1230). Note that the $1.1210 area corresponds to a (50%) retracement of the euro’s bounce that began in the second half of last week. The next retracement (61.8%) is found near $1.1190. It languishes in yesterday’s trough and has not been above $1.1250 ahead of the ECB meeting. There is a roughly 950 mln option struck at $1.1200 that will be cut today and another 1.2 bln euros at $1.1220. The euro has typically fallen on days that the ECB has met since the beginning of last year. Last September and this past April have been exceptions to the rule. Sterling reversed lower after testing the 20-day moving average (~$1.2750) yesterday for the first time in since May 13. It slipped further today but found some bids by $1.2670. The broad dollar direction seems to be the most important consideration now.

America

Fitch seemed more concerned about the slowing of the Mexican economy and Pemex’s debt than the US threat to levy escalating tariff on all imports from Mexico. Fitch’s move is important because it is to bring it to BBB. Moody’s, which cut its outlook to negative is at A3 (A-), is at the high, with S&P in the middle at BBB+ (negative outlook). The peso, which had stabilized in recent days, was hit with this one-two punch. The dollar quickly jumped from around MXN19.58 to around MXN19.84. It is trading near MXN19.70 ahead of the open of the local markets. Recall the high set earlier this week was almost MXN19.61. It is almost as if Trump is juggling the continental issues and China. His tougher stand against Mexico comes as one can expect niceties from Mnuchin and the PBOC Governor who will meet at the G20 finance ministers meeting in Japan over the weekend. Trump seemed more relaxed in the UK about Huawei and seemed to offer reassurances that the intelligence relationship would continue. The US position shares with its trade stance, a desire to limit quantities. The fact that Mexico is apprehended nearly double the number of undocumented migrants last month from a year ago is not sufficient if the number of undocumented migrants trying to come into the US also rise.

A tariff on Mexico hurts Trump in three ways. First, like all tariffs is a tax that the buyer pays. Movement of goods within US companies, whose operations are on both sides of the border account for as much as 60% of trade. It would undermine support from part of his base. Second, such a tariff on Mexico would kill the USMCA. The threat alone is potent. Third, it could lead to Congress overruling the President on his use of emergency power, and taking back some trade authority. This would be the moral equivalent of a censure.

| The US reports the April trade balance, Q1 productivity and unit labor costs figures, and weekly jobless claims, but the focus today is elsewhere (ECB and tomorrow’s employment report) and Mexico. Yesterday’s news was mixed. The ADP disappointed with a lowly 27k increase in private sector jobs, but it was offset by the unexpected strength of the non-manufacturing ISM, which included a big rise in employment (58.1 from 53.7) and new orders (58.6 from 58.1). The Beige Book was also mostly upbeat with business outlook “solidly positive.” On the other hand, the distress of farmers has increased amid poor weather and lower prices for crops. Canada also reports April trade figures and non-oil exports may be the key to the market’s reaction. |

U.S. Trade Balance, April 2019(see more posts on U.S. Trade Balance, ) Source: investing.com - Click to enlarge |

After approaching last month’s low (~CAD1.3360), the US dollar popped back above CAD1.34 yesterday. It reached CAD1.3430 earlier today but is coming off in line with the softer tone against the other majors. It is difficult for short-term participants to have much conviction. The US dollar began the week north of CAD1.35 the upper end of its recent range has frayed the lower end of the range. The Dollar Index recovered yesterday after reaching its lowest level since April 12 (~95.75). However, there has been no follow-through buying today. It is in a 15 tick range through the European morning as the market awaits the ECB meeting and press conference.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,ECB,EUR/CHF,Eurozone Employment Change,Eurozone Gross Domestic Product,Eurozone Gross Domestic Product QoQ,Mexico,newsletter,U.S. Trade Balance,USD/CHF