Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

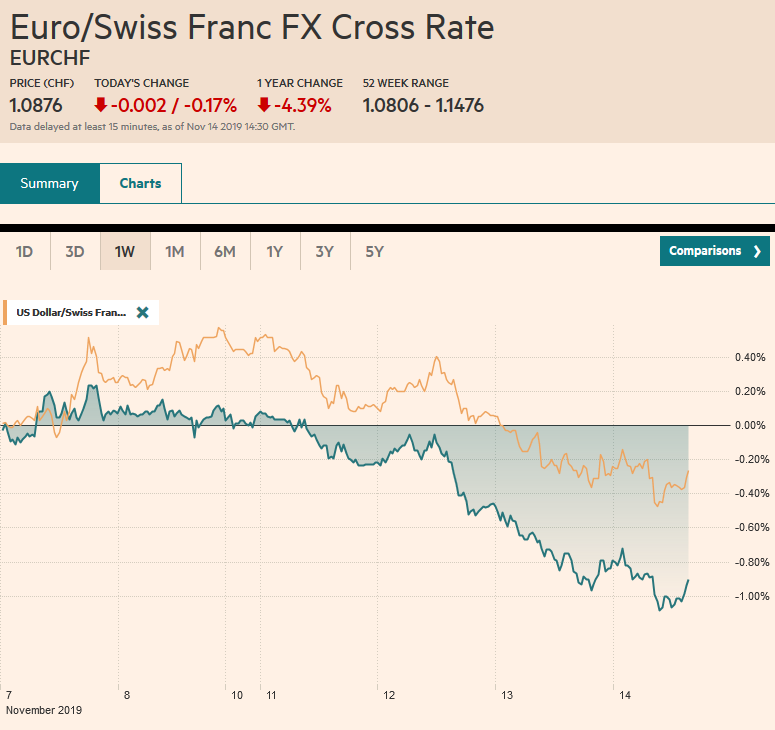

Swiss FrancThe Euro has fallen by 0.17% to 1.0876 |

EUR/CHF and USD/CHF, November 14(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Rising trade anxiety and disappointing economic reports from the Asia Pacific region helped unpin the profit-taking mood in equities, while bond yields continued to pullback. The MSCI Asia Pacific Index and the Dow Jones Stoxx 600 are in the red for the fourth time in the last five sessions. Germany reported a surprise 0.1% expansion in Q3, but it has done little for the DAX or the euro. The S&P 500 eked out a small gain yesterday but is trading heavier again now. Benchmark bond yields are mostly 2-5 bp lower, though the disappointing Australian jobs report fueled nearly a 10 bp decline in the Aussie bond yield. The dollar is mixed, with the risk-off mood aiding the Swiss franc and Japanese yen. Gold is edging higher for the third consecutive session, while oil is marginally extending yesterday’s gains. |

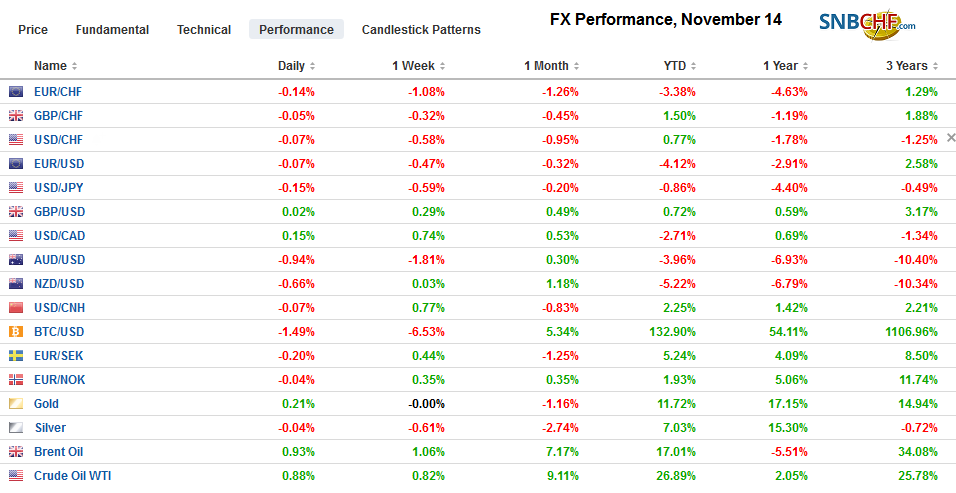

FX Performance, November 14 - Click to enlarge |

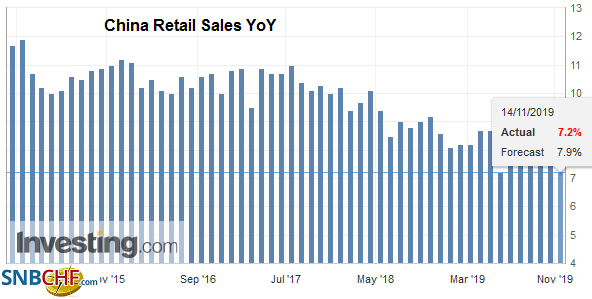

Asia PacificBeijing apparently thinks that Washington overplayed its hand. By announcing the “handshake deal” a month ago, obviously, prematurely, the US President revealed he wanted a deal. And one need not know the nuances of modern psychology to recognize the projection in Trump’s repeated claims of how China wants a deal more than him. There is not date to sign off on the handshake deal because nothing is agreed upon until everything is. There is no deal. China continues to insist that tariffs are rolled back sooner and more than the US is willing. The US insists on high quantitative targets. Reports indicate it wants China to agree to $50 bln a year in agriculture imports from the US. At its peak in 2017, China imported about $24 bln of US foodstuffs. And this was a culmination of a 700% increase since 2000. Separately, and not surprisingly, as it has already been tipped, China lifted its ban on US poultry. China, Japan, and Australia reported disappointing data. China’s fixed-asset investment, industrial output, and retail sales not only missed expectations but were weaker sequentially. The fourth quarter is off to a poor start and follows weak lending figures. The key takeaway is that economists are projecting that the world’s second-largest economy growth is slowing below the 6% threshold in the current quarter. Investors will anticipate further stimulus, perhaps as early as next week, when the prime loan rate is set. |

China Retail Sales YoY, October 2019(see more posts on China Retail Sales, ) Source: investing.com - Click to enlarge |

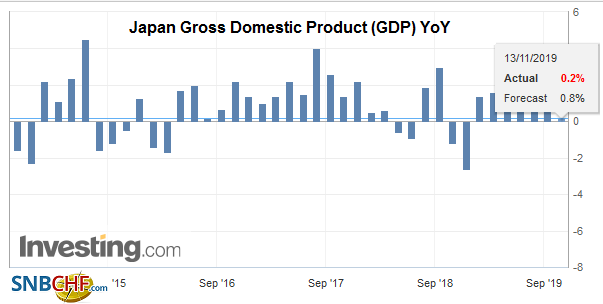

| Japan, the world’s third-largest economy, nearly stagnated in Q3, growing 0.2% at an annualized rate. Economists had expected something four-times the magnitude. It follows a 1.8% pace in Q2. Moreover, even this meager growth may prove unsustainable in Q4 as it was flattered by the surge in retail sales ahead of the new tax. Exports were a drag, while business investment rose. The Abe government has already proposed boosting spending in a supplemental budget by JPY5 trillion. |

Japan Gross Domestic Product (GDP) YoY, Q3 2019(see more posts on Japan Gross Domestic Product, ) Source: investing.com - Click to enlarge |

The resilience of the Australian labor market cracked last month as it lost 19k jobs. The market had expected a gain of nearly as many. It is the first loss of jobs since May 2018 and the largest loss since August 2016. The unemployment rate ticked up to 5.3% (from 5.2%), and the participation rate slipped to 66.0% (from 66.1%). That said, full-time positions fell (-10.3k) for the fifth time in 10 months. Separately, a private estimate of inflation expectations in November rose to 4.0% from 3.6%, which is the highest since March 2018.The odds of a rate cut next month edged higher to about 30%.

The US dollar is pulling further away from the last week’s high near JPY109.50. It is at an eight-day low, having dipped slightly below JPY108.60. There is an option for $520 mln struck at JPY108.57 that expires today and another for $450 mln at JPY108.20. The trendline from the August, October, and early November lows is found near JPY108.50 today. The Australian dollar is lower for the fifth consecutive session and has punched through $0.6800 for the first time since October 17. It has taken out its trendline drawn off the October lows, and may now offer resistance (~$0.6820). The next target is in the $0.6770 area, and there is an option that expires today for about A$530 mln at $0.6775. The dollar is little changed against the Chinese yuan near CNY7.02

EuropeGermany offered a pleasant economic surprise. It defied private sector forecasts as well as the Bundesbank’s own projections for a contraction in Q3. Instead, aided by government spending and consumption, the economy expanded by 0.1% quarter-over-quarter. On the other hand, Q2 GDP was revised down to -0.2% from -0.1%. Growth in Q1 was revised to 0.5% from 0.4%. It begs the question of the definition of a recession. Net-net the economy contracted in the six months from March to September. It does not really change the facts on the ground. The ordoliberals that do not see a need for fiscal stimulus will not see it after today’s report, and those that do, nearly everyone outside of Germany, still will. |

Eurozone Gross Domestic Product (GDP) YoY, Q3 2019(see more posts on Eurozone Gross Domestic Product, ) Source: investing.com - Click to enlarge |

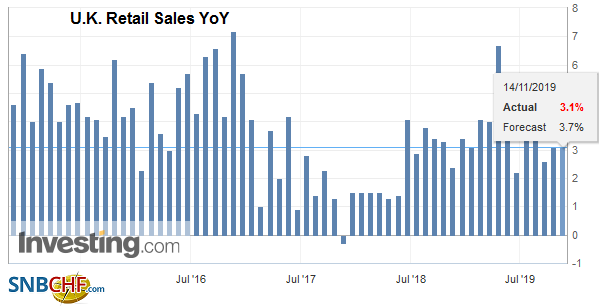

| The UK’s October retail sales report disappointed, falling 0.3%, excluding petrol. It is the second decline in three months and pushes the year-over-year rate to 2.7%. Include auto fuel, retail sales edged 0.1% lower. Economists expected both measures of retail sales to have expanded by 0.2%, partly on ideas of household stockpiling ahead of the October 31 Brexit deadline. Ideas that the UK Tories may still win next month’s election helped sterling shrug off the disappointing economic data. |

U.K. Retail Sales YoY, October 2019(see more posts on U.K. Retail Sales, ) Source: investing.com - Click to enlarge |

The euro remains pinned near $1.10, where there is an option for nearly 700 mln euros that expires today. On the top side, another set of options for around 1.6 bln euros is found in the $1.1040-$1.1050 area, but the euro may struggle to move above $1.1020. While we suspect the euro’s decline from the recent test on the $1.1180 area is nearly complete, there is little evidence to hand one’s hat on today. Sterling is going nowhere quickly. It continues to trade in a narrow range seen over the last few days (~$1.2815-$1.2875). There is an option for around GBP300 mln at $1.2850 that will be cut today.

America

Most observers seemed to think that at the end of last month, the FOMC delivered a hawkish cut by signaling the end of the midcourse correction with the third rate cut of the year. However, many saw the Fed’s hold more tentative, and Powell seemed to confirm an easing bias remains. He did this by playing up the risks, where all to the downside, slowing global growth, trade developments, and persistently low inflation can adversely impact expectations. Yes, the current stance is appropriate, the Chairman said, provided that the economy stays on the path the Fed expects in the face of noteworthy risks. Powell’s testimony may have been a tell–the minutes of the October FOMC meeting, released next week, maybe more dovish than had appreciated. Powell speaks to the House Budget Committee. Seven other Fed officials speak today, but after several dissents in recent months, everyone seems to be singing from the same song now.

The US reports October PPI and weekly jobless claims. The base effect points to a material decline in the year-over-year rise in producer prices (0.9% from 1.4% for the headline and 1.5% from 2.0% for the core pace). However, the report rarely has a lasting impact on trading. Tomorrow the US reports the more market-sensitive retail sales (and industrial production). Canada reports new house prices. The central bank of Mexico meets later today and is expected to the third 25 bp rate cut here in H2 that would brine the overnight target rate to 7.5%, which is where it was June last year.

The month of November is nearly half over, and the Canadian dollar has only risen against the US dollar in two sessions this month. Today could be the fifth consecutive session without a gain. The US dollar is trading in the upper end of yesterday’s range, just below the 200-day moving average near CAD1.3275. The market may test the CAD1.3300 area, but the technical indicators are getting stretched. The US dollar spiked to almost MXN19.53 yesterday but settled below MXN19.40. Yesterday’s high largely met the (61.8%) retracement objective of the dollar’s decline from the October 2 high. Support is pegged in the MXN19.30-MXN19.34 area. The risk-off mood and the pressure from other Latam currencies, for which the peso is often seen as a liquid and accessible proxy, may have exaggerated the peso’s recent weakness. The carry may still attract flows in a more stable market.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,China Retail Sales,Currency Movement,EUR/CHF,Eurozone Gross Domestic Product,federal-reserve,FX Daily,Germany,Japan Gross Domestic Product,newsletter,Trade,U.K. Retail Sales,USD/CHF