Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

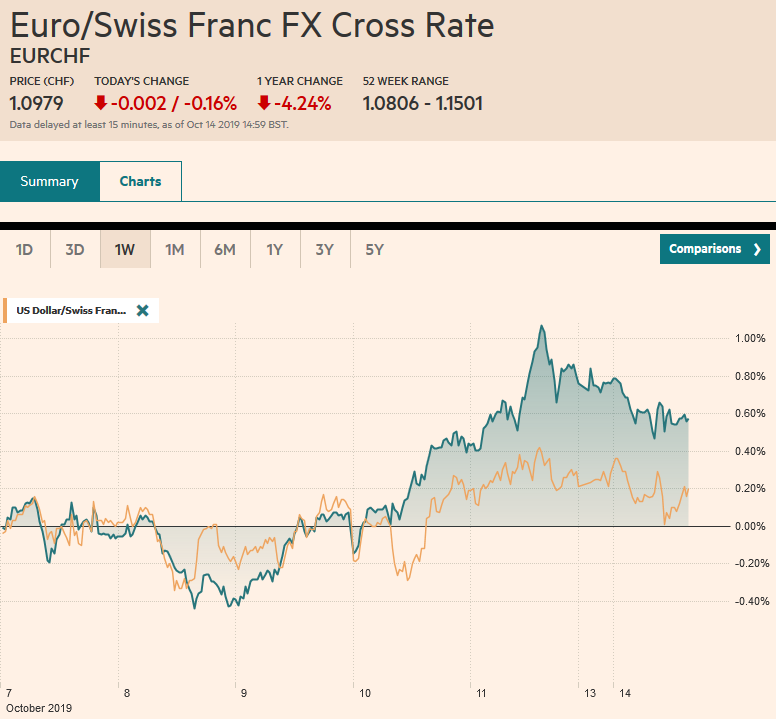

Swiss FrancThe Euro has fallen by 0.16% to 1.0979 |

EUR/CHF and USD/CHF, October 14(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Japanese and Canadian markets are on holiday today. While the US bond market is closed, equities maintain their regular hours today. Asia Pacific equities rallied, led by 1% of more gains in China, Taiwan, South Korea, and Thailand. The buying did not continue in Europe, and after a 2.3% rally before the weekend, the Dow Jones Stoxx 600 is about 0.75% lower in the European morning. US shares are trading slightly heavier, and the gap in the S&P 500 created by last Friday’s sharply higher opening is worth monitoring (~2948.5-2963.1). Benchmark yields in Asia Pacific were pulled higher by the rise in US yields at the end of last week, while European yields are coming back softer, with core rates off a couple for basis points. UK 10-year Gilt yields are off around seven basis points on the lack of progress over the weekend with Brexit talks, which dragged sterling lower. The Antipodean and Scandi currencies are off 0.4%-0.5%, while sterling is nearly 0.75% lower. The Japanese yen and Swiss franc are steady to firmer. Among emerging market currencies, the Turkish lira is the weakest, off about 0.5%. East and Central European currencies are softer, while Asian currencies are mostly higher. The Singapore dollar firmed after a slight easing by the Monetary Authority, and the dollar fell below CNY7.05 briefly for the first time since August 19. Oil is trading around 1% lower, while gold is steady. |

FX Performance, October 14 - Click to enlarge |

Asia Pacific

Chinese coverage of what the US has dubbed “phase one” of a trade agreement was not nearly as ebullient. Nothing was signed. China will buy more agriculture products from the US, which is has long been willing to do. It has a food shortage, and this is evident in today’s trade numbers and will likely be seen in the CPI figures due tomorrow. The US will not go forward with the increase in tariffs on around $250 bln of Chinese goods from 25% to 30%, which we have argued was largely symbolic. If a good is not competitive with a 25% levy, a 30% level or a 50% level makes a marginal difference at best. Trump and Xi are to meet on the sidelines of the APEC meeting next month. The mid-December tariff on about $160 bln of Chinese goods, which have not been subject to a punitive tariff, is what is in play.

| China’s imports and exports were weaker than August and lower than expected. The trade surplus widened to $39.65 bln in September from $34.78 bln. Exports were off 3.2% year-over-year after the 1.0% decline in August and forecasts for a 2.8% decline. Pork imports are 44% higher from a year ago, and beef imports are 54% higher, but overall imports contracted 8.5% in September following a 5.6% decline in August. The median forecast in the Bloomberg survey anticipated a 6% decline. The surplus with the US (~$26 bln) is roughly two-thirds of China’s surplus. Exports to the US are more than a fifth lower (22%) from a year ago, and imports from the US are down 16%. What is not told in these numbers are the exports from China to the US that are made by US companies in China. Separately, China reported auto sales fell 6.6% year-over-year in September, the 15th decline in the past 16 months. |

China Trade Balance (USD), September 2019(see more posts on China Trade Balance, ) Source: investing.com - Click to enlarge |

Singapore Monetary Authority took a small step toward easing policy for the first time in three years. It conducts monetary policy through its currency and slightly reduced the appreciation of the foreign exchange band. It left unchanged the band’s width and the level within the band. The move was widely anticipated, even before the news that the economic growth was half as much as expected in Q3 (0.6%), which put year-over-year growth at a meager 0.1%. About a third of the economists polled by Bloomberg expected a more aggressive easing of policy. The Singapore dollar gained about 0.3% today, in line with the Chinese yuan and the South Korean won.

The dollar has been confined to within a 20-tick range on either side of JPY108.35 as it consolidates last week’s 1.25% rise. There is an option for almost $430 mln at JPY108.50 that expires today. We suspect the risk is on the downside now and look for the JPY108 area to be tested in North America. The Australian dollar has unwound most of its pre-weekend gains. Initial support may be seen near $0.6750, which also corresponds to a (61.8%) retracement of the gains from the second half of last week. The neckline of a possible head and shoulder bottom pattern, we noted, is near $0.6740, and it is not usual in the pattern to come back and retest the breakout.

EuropeThe optimism that spurred the powerful short-squeeze in sterling was slapped by the cold hand of realism over the weekend. Johnson’s plan was present to the cabinet as the EC negotiators were far from satisfied.The UK is offering a complex dual customs system that seems to turn Northern Ireland into a Schrodinger’s cat that is both in the UK’s customs territory for some goods, depending on the final destination, or the EU’s customs territory. Officials were reluctant to recognize it as a break-through. Some cautioned that it would undermine the EU customs code, while others were skeptical that it would be approved by Parliament as Johnson himself objected to a vaguely similar plan when offered by former Prime Minister May. Contrary to Johnson’s expectations, the EC is not capitulating. Time is running out ahead of the EU summit later this week. An emergency summit on October 29-30 remains a distinct possibility. |

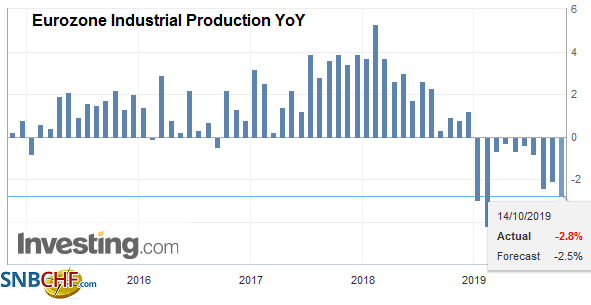

Eurozone Industrial Production YoY, August 2019(see more posts on Eurozone Industrial Production, ) Source: investing.com - Click to enlarge |

Johnson’s Queen’s Speech today, where the government’s legislative agenda is laid out, is a bit of a sideshow where Brexit is still center stage. It might be best understood of the domestic platform Johnson will run at the election that could be held next month. The Tories continue to enjoy a lead over Labour in the polls, but a majority still seems out of reach.

In Hungary, Prime Minister Orban lost control of Budapest in lost elections as well as several other large cities. It is a blow but not a mortal wound. Orban’s Fidesz Party has a large majority in parliament, and national elections are not scheduled until 2022. Still, it may show the limits on its rule. On the other hand, the ruling Law and Justice Party in Poland won over 40% of the vote while the leading opposition party, the Civic Coalition, garnered a little more than a quarter of the vote. The Law and Justice Party will be able to secure a slightly larger majority in Parliament. The election may embolden it in its clash with the EU more immediately over the independence of the judiciary.

The euro rallied almost a cent in the last two sessions of last week and is consolidating in its pre-weekend range today. It found bids near $1.1015 in Europe, and there is an option for about 905 mln euro at $1.10 that expires today. Initial resistance is seen near $1.1050. Sterling had tested the $1.27 area ahead of the weekend on the Brexit optimism and tested $1.2550 late Asian and early European dealings. There is an option for almost GBP480 mln at $1.2540 that rolls off today. The immediate risk extends toward $1.2520, but stronger support may not be seen until closer to $1.2450.

America

The US bond market is closed today, though the equity market is open. Canada’s markets are closed for Thanksgiving. There are no economic reports today or Fed speeches. The week’s highlights include the first survey data for October and September retail sales and industrial production figures. The Fed’s Beige Book in preparation for the October 29-30 FOMC meeting will be released in the middle of the week. The implied yield of the January fed funds futures contract rose 9.5 bp last week, but with the Fed addressing the reserves and refi issues last week, we think it clears the path of another rate cut at the end of the month.

Last week’s announcement was another way the Fed is trying to help the market distinguish between its purchase of T-bills as different that QE. QE was part of monetary policy, and it was announced at FOMC meetings. It was the purchase of long-term securities. Some T-bills that the Fed buys at the start of the program, as early as this week, will roll off before the pre-announced buying program is complete. The T-bill purchase was treated by the debt market as an easing of policy. On the contrary, rates across the curve increased last week. Quantitative easing was driven by the desire to boost the asset side of the Fed’s balance sheet. The current operations are driven by the need to create new liabilities (excess reserves).

The US dollar fell from around CAD1.3350 on October 10 to below CAD1.3200 a day later, helped by strong optics of Canada’s jobs report and an offered greenback. The full-time jobs created can be traced to government hiring, but even so, the central bank’s neutral standing was reinforced. Corrective pressures could lift the US dollar toward CAD1.3240-CAD1.3260 without inflicting damage to the Loonie’s technical tone. The greenback’s slump at the end of last week saw it test the 200-day moving average against the Mexican peso near (~MXN19.26). It is consolidating those losses today, and initial resistance is seen near MXN19.40.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Brexit,China,China Trade Balance,EUR/CHF,Eurozone Industrial Production,Hungary,newsletter,Poland,Singapore,Trade,USD/CHF