Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

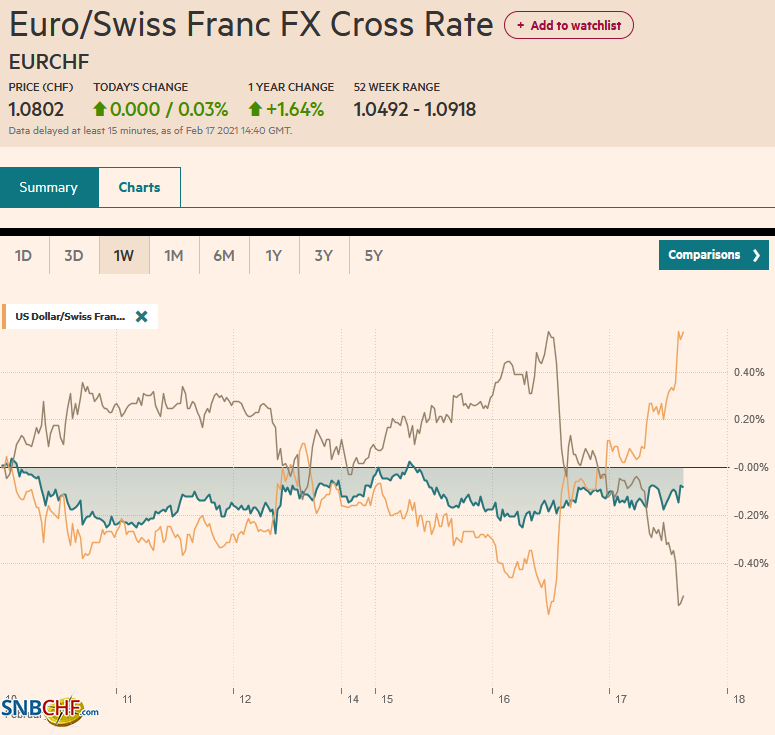

Swiss FrancThe Euro has risen by 0.03% to 1.0802 |

EUR/CHF and USD/CHF, February 17(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: After reversing higher yesterday, the US dollar sees follow-through gains today, leaving the euro around a cent lower from yesterday’s highs. Sterling’s surge is also being tempered. Most emerging market currencies are lower as well. The jump in bond yields has stalled, but only after Australia and New Zealand yields surged eight basis points to play catch-up with the dramatic rise in the US yesterday that saw the 10-year benchmark trade near 1.31%. The yield has come back a little softer today at 1.29%. European bond markets are slightly softer. Profit-taking in US equities yesterday has also spilled over into today’s activity, weighing on Asia Pacific and European equities. The MSCI Asia Pacific Index fell for only the third time this month. Europe’s Dow Jones Stoxx 600 is lower for the second consecutive session, while the US shares little changed with a heavier bias. In the face of rising yields and the dollar’s bounce, gold took it on the chin. The 50-day moving average has slipped below the 200-day moving average for the first time in two years. It is trading near three-month lows today. The weather disruption continues to ripple across the US Midwest, leaving March WTI hovering in around a half dollar range on either side of $60. |

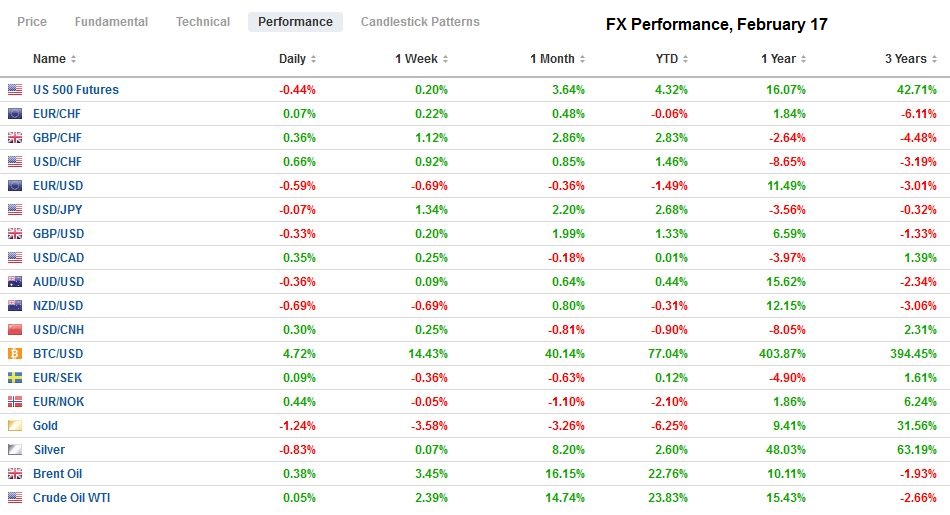

FX Performance, February 17 - Click to enlarge |

Asia Pacific

Japan’s January trade deficit was about half of what economists expected (-JPY324 bln vs. -JPY625 bln. Exports rebounded (6.4% vs. 2.0%), while the import recovery was weak (-9.5% vs. -11.6%). However, the details were revealing. Exports to China rose 37.5% year-over-year, bolstered by chip-making equipment. Exports to the US were off 4.8% year-over-year. Auto exports were weak. Shipments to Europe were 1.6% lower from a year ago. Some pundits may argue that China’s trade surplus means it is a net taker from the world’s aggregate demand, but such assessments do not do justice to China’s imports from some countries, like Japan, even if not the US. Singapore also reported strong January exports today (12.8% year-over-year, more than twice the median in Bloomberg’s survey).

The dollar rose a little above JPY106.20 in Tokyo, its highest level since last September. Rising US rates are seen as the main driver. Initial support is near JPY105.80. The 200-day moving average is around JPY105.50, where a $405 mln option expires today. After trading on both sides of Monday’s range yesterday, the Australian dollar settled just inside that range. While avoiding a technical key reversal, there was follow-through selling today that took it to about $0.7730 after briefly punching above $0.7800 yesterday. Working through the nearly A$760 mln option at $0.7750 that expires today, maybe lending it support. A break of $0.7720 is needed to signal more than a flattish consolidation. Australia reports January employment figures first thing tomorrow. China’s markets re-open tomorrow. After testing the CNH6.40 area on Monday and Tuesday, the greenback has bounced back and is near CNH6.4420 now. It was a little below CNH6.43 when the holiday started.

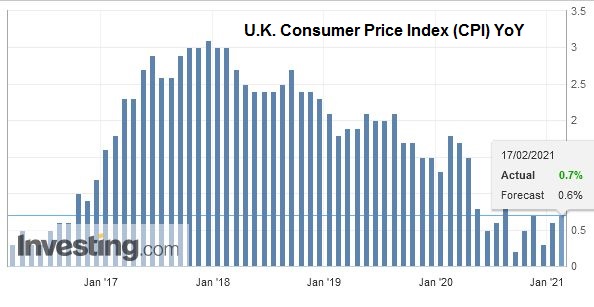

EuropeThe UK’s January consumer prices were a touch firmer than expected. CPIH, the preferred measure, which includes owner-occupied housing costs, ticked up to 0.9% from 0.8% year-over-year. The headline CPI eased by 0.2% in the month, half the decline economists expected, lifting the year-over-year rate to 0.7% from 0.6%. The core rate was unchanged at 1.4%. Producer prices were also slightly firmer than expected, with output prices rising by 0.4% on the month and input prices rising by 0.7%. There is not much to take away from these figures. Price pressures remain modest, and the greater challenge is aggregate demand. January retail sales are due at the end of the week, and a sharp decline is expected. While the rise in US yields is the stuff headline are made of, the magnitude of the increase in global yields may not be appreciated. Consider that over the past month, the 10-year US Treasury yield has risen by about 20 bp. The 10-year Gilt yield is up more than 30 bp. Canada’s yield has increased by nearly 32 bp. Sweden and the Netherlands have seen their benchmark yields rise 22-23 bp. German and French yields are up 17-18 bp. Australia’s 10-year yield has risen by 33 bp over the past month, while New Zealand’s yield has surged by 50 bp. Italy is the exception. Its benchmark yield is off nearly six basis points. Germany sold 30-year bonds today, and the yield was positive for the first time since last March. |

U.K. Consumer Price Index (CPI) YoY, January 2021(see more posts on U.K. Consumer Price Index, ) Source: investing.com - Click to enlarge |

The euro posted a key reversal yesterday, and follow-through selling took it to a six-day low near $1.2060. The euro frayed the $1.2150-cap yesterday, rising to almost $1.2170 before reversing lower and settling below Monday’s lows. A break now of $1.2035 would lend credence to our view that the euro’s downside correction is not over. There is an option for 540 mln euros at $1.2020 that expires today. While intraday moment readings are stretched, the North American participants have appeared more dollar-friendly in recent sessions. Sterling briefly poked above $1.3950 yesterday before retreating. It is heavy today, testing support near $1.3860 in the European morning. Intraday indicators are stretched, but a break here could signal a test on the $1.38-level, which houses an option for about GBP255 mln that expires today.

America

Fed talk was interesting yesterday and may offer insight into what Chair Powell will say next week during his semi-annual congressional testimony. The common theme was that inflation is not a problem. Kansas Fed President George told her audience that she was not concerned by the rise in long-term yields, linking it to growing optimism about future growth. San Francisco’s Daly argued that unwanted inflation is not around the corner and that there are still downward pressures on prices. She warned that a worry about inflation now leading to premature tightening of financial conditions could cost millions of jobs. St. Louis Fed President Bullard said that the FOMC is not thinking about tapering and also played down any immediate inflation threat. He also pushed back against claims that the spectacular rise in Bitcoin has no impact on Fed policy.

Bullard seemed more sympathetic to arguments that Bitcoin poses a greater challenge to gold than to the dollar. It seems like a bit of a Rorschach test. Some claim that Bitcoin says something about the world economy and the US place in it, which appears to be more a confirmation bias than a robust demonstration of linkages to the dollar’s role as numeraire and as largest reserve asset. It is a new skin for old wine. The arguments are wrecked on the same shoals as the earlier attempts. There is simply no compelling alternative. To shift reserves out of Treasuries because of the rise of Bitcoin results in lower yields, less liquidity, and arguably less security and transparency. That claim there has been a loss of trust in the dollar is not supported by the IMF’s authoritative data. Dollars held in reserves rose 25% from the end of 2016 through Q3 2020 to $6.9 trillion.

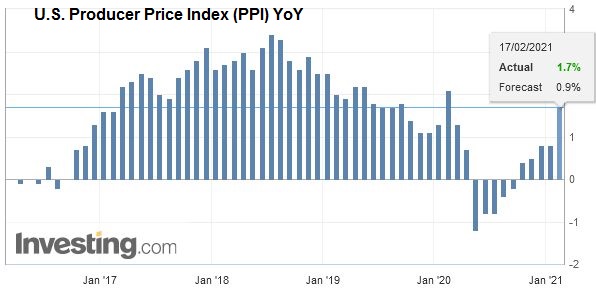

| The US economic diary today includes January PPI, retail sales, and industrial production. The minutes from last month’s FOMC meeting are released late in the session. A modest 0.2% increase in PPI is expected, which given the base effect, would be consistent with a tick lower in the year-over-year rates. The risk seems to be on the upside. |

U.S. Producer Price Index (PPI) YoY, January 2021(see more posts on U.S. Producer Price Index, ) Source: investing.com - Click to enlarge |

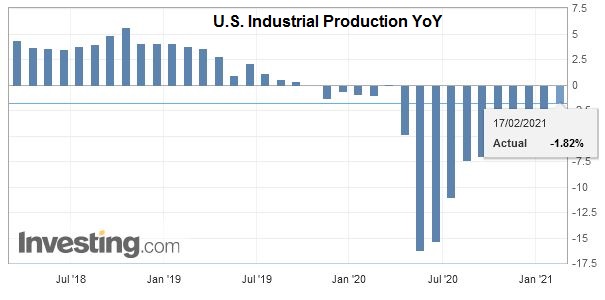

| Industrial production likely slowed from December by a 0.5% increase in January, and a 0.7% boost in manufacturing output is still constructive reports. However, the most important time series today is retail sales. |

U.S. Industrial Production YoY, January 2021(see more posts on U.S. Industrial Production, ) Source: investing.com - Click to enlarge |

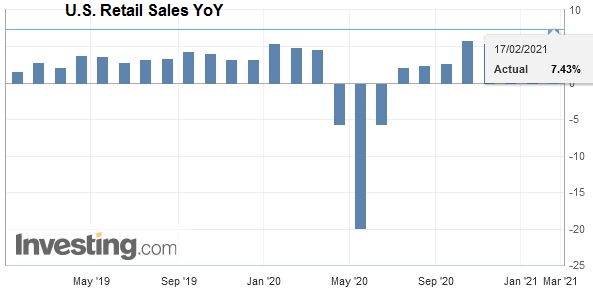

| Retail sales fell every month in Q4 and are expected to have snapped the decline in January. Note that the Q4 slump in retail sales (cumulative ~-2.2%) translated into a 2.5% increase in consumption in the GDP calculations. Recall that in Q3, 20 retail sales rose by a cumulative 4.2%, and consumption rose 41% in the GDP report. |

U.S. Retail Sales YoY, January 2021(see more posts on U.S. Retail Sales, ) Source: investing.com - Click to enlarge |

Canada reports January CPI figures today. After falling by 0.2% in December, consumer prices are expected to have risen by 0.5% in January. The year-over-year rate likely rose to 0.9% from 0.7%. It has not been above 1% since last February. However, this is seen to be distorted by energy prices, among other factors. The takeaway is that the underlying core measures that the Bank of Canada puts more stock are considerably more stable and higher.

The US dollar reversed higher yesterday against the Canadian dollar. It initially approached CAD1.26 before recovering to briefly traded above CAD1.27. Follow-through buying has been limited the greenback to about CAD1.2720 today, seen in both Asia and then again in Europe. Last week, the US dollar ran into resistance in the CAD1.2765-CAD1.2785 area. Initial support is seen near CAD1.2680. The US dollar forged a shelf in the MXN19.90 area and from there launched an assault yesterday on the MXN20.25 area, its highest level since February 5. Buying today lifted the greenback to almost MXN20.2770. The MXN20.50-MXN20.60 area capped the greenback last month and so far here in February.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Currency Movement,Featured,federal-reserve,inflation,newsletter,Trade