Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

FX Daily, June 16: Correction Scenario Tested

FX Daily, June 16: Correction Scenario Tested16 Jun 2020

FX Daily, May 15: Much Talk but Little Action15 May 2020

FX Daily, April 15: Dollar Rises as Equities Slump15 Apr 2020

FX Daily, March 17: Even Turn Around Tuesday is Flat17 Mar 2020

FX Daily, February 14: Investors Continue to Look Past the Coronavirus

FX Daily, February 14: Investors Continue to Look Past the Coronavirus14 Feb 2020

FX Daily, December 16: China Data Surprises to the Upside while Europe’s Manufacturing PMI Disappoints16 Dec 2019

FX Daily, November 15: Market Runs with US Line that US-China Deal is Close15 Nov 2019

FX Daily, October 17: EU-UK Deal Sends Sterling and the Euro Higher17 Oct 2019

FX Daily, September 17: Markets Calm(er)17 Sep 2019

FX Daily, August 15: Animal Spirits Lick Wounds15 Aug 2019

FX Daily, May 15: Angst Continues15 May 2019

Green Shoot or Domestic Stall?17 Apr 2019

FX Daily, April 16: The Dollar and Stocks Catch a Bid

FX Daily, April 16: The Dollar and Stocks Catch a Bid16 Apr 2019

Monthly Macro Chart Review – March8 Mar 2019

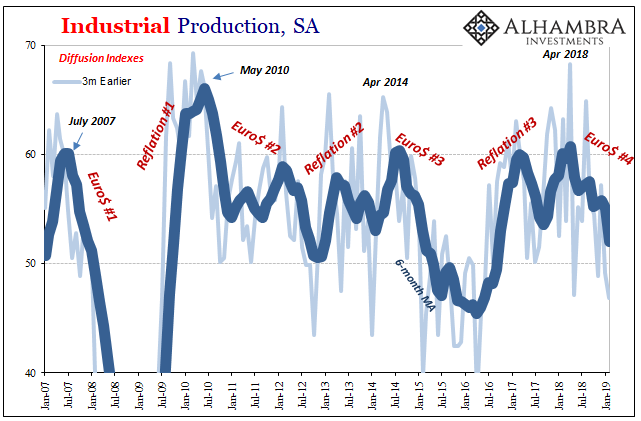

Getting Back Up To Speed On Loss Of Speed in US Economy21 Feb 2019

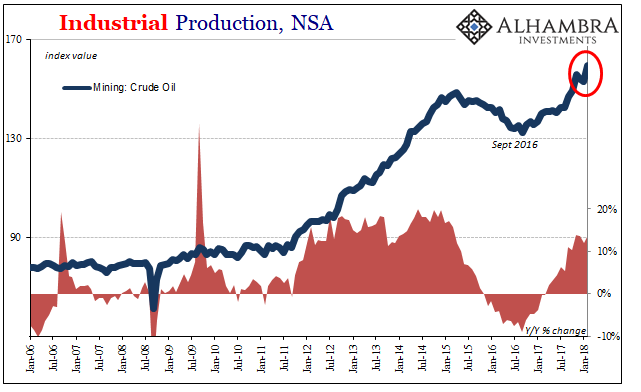

There Isn’t Supposed To Be The Two Directions of IP20 Jun 2018

Globally Synchronized Asynchronous Growth26 May 2018

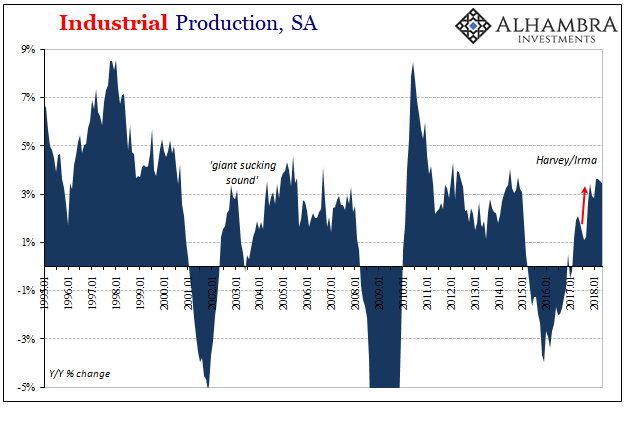

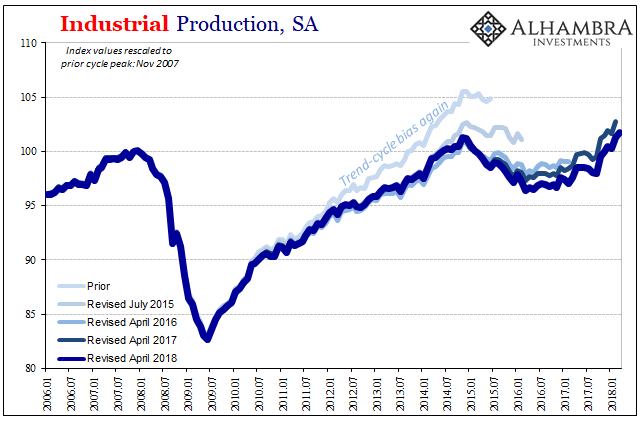

Why The Last One Still Matters (IP Revisions)26 Apr 2018

FX Daily, April 17: Dollar Recovers from Further Selling as Turnaround Tuesday Unfolds17 Apr 2018

US Industry Experiences The Full 2014 Again in February20 Mar 2018