Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

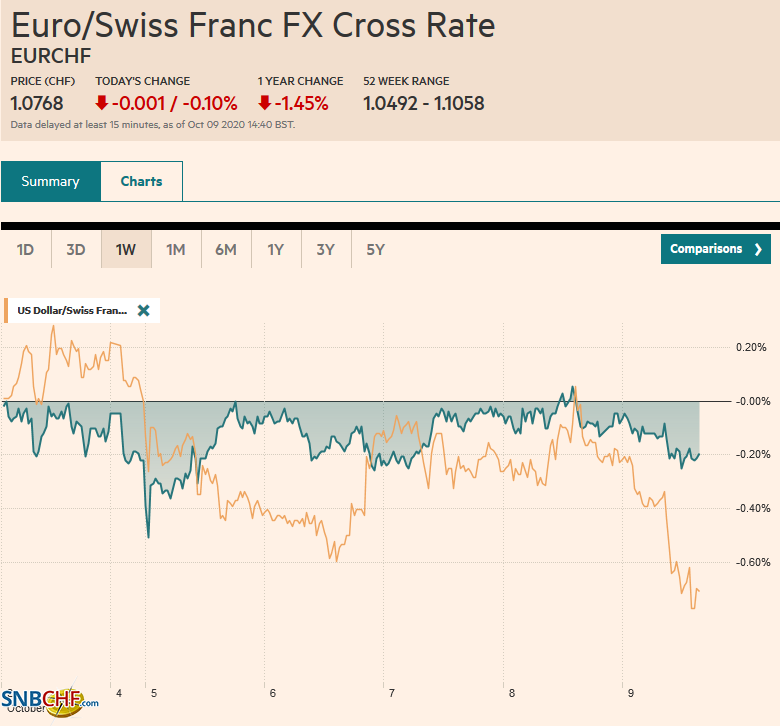

Swiss FrancThe Euro has fallen by 0.10% to 1.0768 |

EUR/CHF and USD/CHF, October 09(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The on-again-off-again fiscal stimulus in the US is back on as the White House now supports a broad stimulus program, but not as big as the Democrats $2.2 trillion package. It is the narrative being cited as the rebuilding of risk appetites is the wobble earlier in the week. Chinese markets re-opened with a bang. Shanghai led the Asia Pacific bourses higher with a 1.7% gain, and the onshore yuan rose 1.1%, a bit more than expected after a favorable fix by the PBOC. Europe’s Dow Jones Stoxx 600 moved above the 200-day moving average yesterday and remains above it today. It is up modestly, for the sixth session of the past seven. The S&P 500 and NASDAQ gapped higher yesterday, closed near the highs, and look likely to gap higher again. Benchmark 10-year bond yields are 1-3 basis points lower in Europe, and Italy’s 10-year yield is at a new record low. The 10-year US yield is around 0.77%, up about six basis points on the week that saw a new supply. The dollar is on its back foot, falling against nearly all the world’s currencies today. The euro is knocking on $1.18, and even the yen is better bid. The JP Morgan Emerging Market Currency Index is edging higher and is up about 0.5% on the week. Gold has rallied more than 1% today to about $1916, putting it within striking distance of the week’s high set on October 6 near $1921. The US Gulf storm has shuttered more than 90% of the oil capacity, driving WTI for November delivery higher. It is straddling the $41 a barrel level as it puts the finishing touches on its best week since May (~10.5%). |

FX Performance, October 9 - Click to enlarge |

Asia PacificChina’s markets reopened after the holiday. The Caixin PMI was a bit confusing. Recall that before the holiday, the manufacturing PMI slipped to 53.0 from 53.1. Today it reported the services PMI rose to 54.8 from 54.0, which was better than expected. However, the composite fell to 54.5 from 55.1. More attention was paid to the yuan’s strength, which is now at levels last seen in April 2019. There appears to be a regime change under which, as we have suggested, Beijing sees it in its interest to accept an appreciating currency. It has been encouraging foreign portfolio investment. The apparent recovery, high yields, and inclusion in global benchmarks makes it more attractive for global asset managers. |

China Caixin Services Purchasing Managers Index (PMI), September 2020(see more posts on China Caixin Services PMI, ) . |

| Japanese labor earnings and spending for August improve sequentially but were not as strong as expected. Cash earnings were off 1.3% year-over-year after a revised 1.5% decline in July. It appears that the lion’s share of the JPY100k emergency payments has been distributed. Household spending was off 6.9% from a year ago, better than the 7.6% contraction in July, but economists had forecast a 6.7% decline. The data is consistent with a modest recovery in Japan and yesterday’s BOJ report showing eight of nine regions improving. |

Japan Household Spending YoY, August 2020(see more posts on Japan Household Spending, ) Source: investing.com - Click to enlarge |

The dollar has stalled a little above JPY106. It is a little heavier in a narrow range. It has not traded below JPY105.80, where a nearly $610 mln option will be cut today. On the topside, there are options for around $1.9 bln struck in the JPY106-JPY106.10 area. The Australian dollar is firm. It is approaching $0.7200. The week’s high is about $0.7210, representing a (50%) retracement of the decline since September 1. Above there, the next target is near $0.7260. The PBOC set the dollar’s reference rate at CNY6.7796. The median bank model in the Bloomberg survey anticipated a fix near CNY6.7854. The market will be particularly sensitive to officials’ signals on how far they are willing to accept yuan strength. Last year, the dollar’s low was near CNY6.67, and the CNY6.60 is an important chart area.

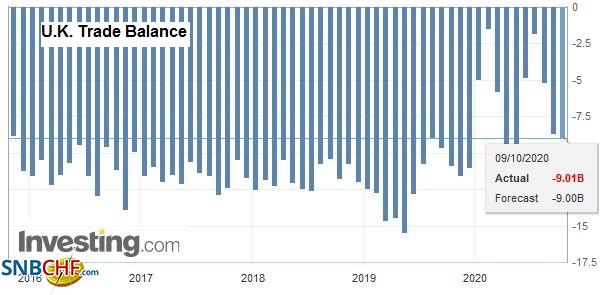

EuropeThe UK’s August GDP was less than half of the 4.6% expansion that the median forecast in the Bloomberg survey projected. The 2.1% expansion follows the downwardly revised 6.4% growth in July (from 6.6%). To be sure, this a monthly GDP, not quarterly or annualized. However, what is important is relative to expectations and sequentially. Industrial production was a big miss, coming in at 0.3% instead of the 2.5% rate economists expected. Services expanded by 2.4%, again half of what had been anticipated. If there was a bright spot with today’s data, the overall trade balance remained in surplus (GBP1.36 bln), while economists had expected a flat report. The July trade surplus was revised to GBP1.69 bln from GBP1.07 bln. Still, the overall disappointment weighed on sterling and reinforces speculation of further easing by the BOE as early as next month. |

U.K. Trade Balance, August 2020(see more posts on u-k-trade-balance, ) Source: investing.com - Click to enlarge |

Italy’s 10-year yield fell to new record lows near 0.72%. Investors appear to be feeling better about the country. Political risk is at a low ebb, and the economy, with the help of strong fiscal support, is doing better. Italy reported a 7.7% surge in industrial output in August. Economists were looking for something closer to 1.5%. The July output was revised to 7.0% from 7.4%. Of the large EMU countries, Italy has been the only one to surprise on the upside with industrial output. France reported a 1.3% increase in industrial production, while expectations for a 1.7% increase, after a 3.8% gain in July. Recall that earlier this week, Germany reported an unexpected 0.2% decline.

The euro is still encountering offers around $1.18. On October 6, it nearly reached $1.1810, which is the (50%) retracement objective of the decline from September 1 high above $1.20. Above there, the next retracement (61.8%) is closer to $1.1860. The market appears to be absorbing offers that may be related to the 1.5 bln euros in options between $1.1795 and $1.1800 that expire today. Between uncertainty surrounding the UK-EU trade talks, sterling has not been able to return to the $1.30-level since earlier in the week, which is also the potential neckline of a bottoming pattern. There is an option for almost GBP230 mln at $1.30 that expires today. Another one, for about GBP360 mln, is struck at $1.29 and also rolls off today.

America

The US economic calendar is light, featuring the final wholesales inventory report for August and the Fed’s Barkin speaks to a regional Chamber of Commerce before the equity market opens. The focus is squarely on the prospects of fiscal stimulus. Lagging in the national polls and in swing states, the administration seems to be showing considerably more flexibility than as recently as the start of the week. Separately, the US has announced new broad sanctions on Iran’s financial sector, including 18 banks that had not been included previously.

The economic highlight for North America today is Canada’s jobs report. It is expected to report an increase of 150k jobs, or perhaps better said, a return of about 150k employees last month. In August, Canada saw a nearly 246k increase in employment, and the bulk (~206k) were full-time positions. The unemployment rate is expected to move back below 10% from 10.2% in August, while the participation rate may tick up to 64.7% from 64.6%.

As reflected in rising equities and rising commodity prices, Robust risk appetites, especially oil’s 10%+ gains this week, have underpinned the Canadian dollar. With today’s losses to CAD1.3160, the US dollar has retracement (61.8%) of the gains since September 1. A break of that area targets CAD1.31, but is likely headed back toward that September 1 low just below CAD1.30. The CAD1.32 area should hold back corrective upticks. The greenback is lower against the Mexican peso for the seventh time in the eight sessions. It is finding some bids below MXN21.30, but we suspect a break of MXN21.25 would signal a test on last month’s low near MXN20.8450.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,China,Currency Movement,Featured,Italy,newsletter,U.K.