Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

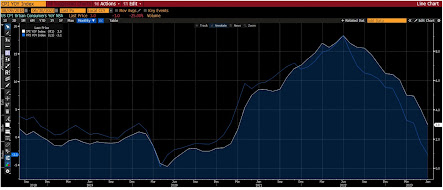

Dollar Jumps

Dollar Jumps28 Feb 2024

The Greenback is in Narrow Ranges to Start the Week12 Feb 2024

Dollar Retreat Extended, but Turn Around Tuesday may have Already Begun20 Nov 2023

Dollar Consolidates Amid Rate Volatility16 Nov 2023

The Dollar Continues to Press Against JPY150; Risk Off Ahead of the Weekend20 Oct 2023

Sharp Fall in US Yields ahead of Large Supply10 Oct 2023

The Greenback is Softer Ahead of CPI but Key Chart Points Remain Intact10 Aug 2023

Fitch Roils Markets2 Aug 2023

The Dollar Regains Composure28 Jun 2023

PBOC Sends Signal in Lower Dollar Fix, while the Canadian Dollar makes a 9-Month High27 Jun 2023

The Dollar Consolidates after Powell Sapped its Mojo22 May 2023

Narrow Ranges in FX: Calm before the Storm?10 May 2023

Dollar Comes Back Bid, as First Republic Taken Over (Mostly) by JP Morgan1 May 2023

Financial Stress Continues to Recede29 Mar 2023

Investors Shaken by Rising Rates22 Feb 2023

Markets Catch Collective Breath16 Feb 2023

Yen Retreats Ahead of Formal BOJ Announcement Tomorrow and US CPI13 Feb 2023

Euro Closed above $1.09 but Follow-Through Buying Limited26 Jan 2023

Risk Appetites Survive China Keeping Zero Covid Policy7 Nov 2022

RBA Hikes by 25 bp, Chinese Stocks Surge, and the Greenback Trades Heavier1 Nov 2022