Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

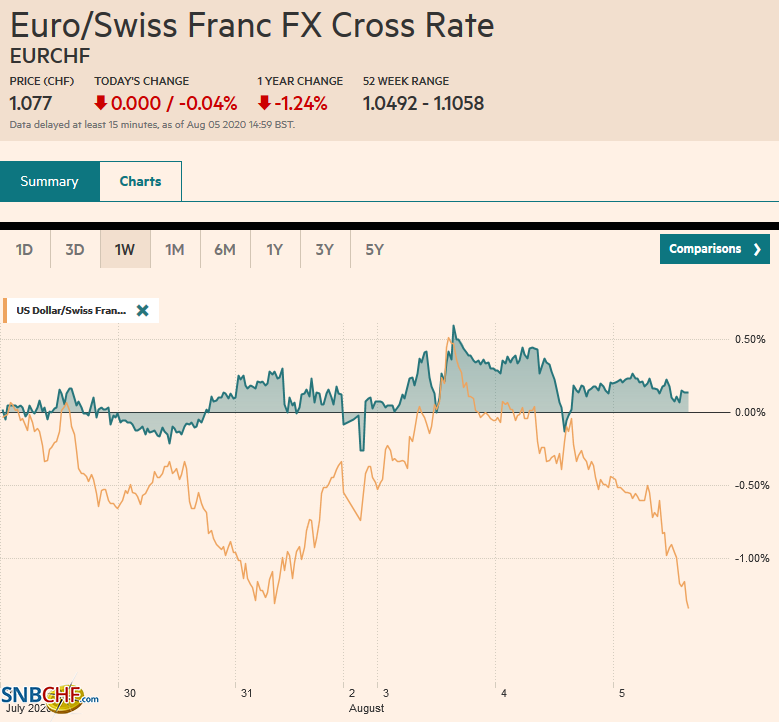

Swiss FrancThe Euro has fallen by 0.04% to 1.077 |

EUR/CHF and USD/CHF, August 5(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The drop in US yields to new lows amid paralysis in Washington, except apparently over a lip-syncing app’s threat to US national security, sent the dollar back to its lows after a modest recovery in early North American trading yesterday. The greenback remains under pressure today, falling against most of the world’s currencies. The beleaguered Turkish lira is a notable exception. The Norwegian krone and dollar-bloc currencies are leading the move. Global equities are mostly firmer, though, in the Asia Pacific region, Japan, Australia, and India were exceptions. The Dow Jones Stoxx 600 is around 0.8% firmer as it continues to recover from the losses at the end of July. US shares are firmer, and the S&P 500 is filling more of the gap from February that extends to around 3328.50, a technical objective. European bond yields are firmer as the US 10-year edges higher after reaching almost 50 bp yesterday. Gold is continuing its rally to new record highs near $2040. Oil is also higher with the September WTI contract near $42 and is poised to challenge last month’s high near $42.50. |

. |

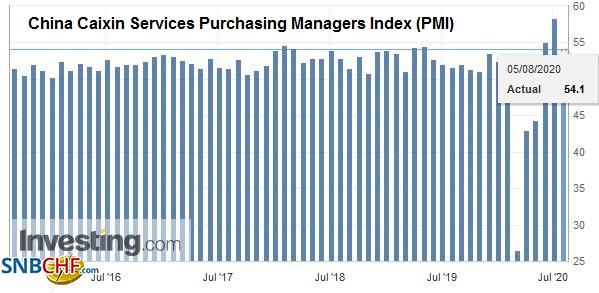

Asia PacificThere are three developments to note in China. First, the Caixin services PMI eased to 54.1 from 58.4. This was sufficient to bring the composite to 54.5 from 55.7. This report suggests that although the world’s second larger economy is recovering, the pace may be slowing. Second, as the rivalry extends into the tech space, Beijing has unveiled new efforts to aid the semiconductor and software industry. While this is consistent with its import substitution strategy, it is likely to elevate concerns about the statist approach. Third, the Chinese and US officials will have a formal review of the progress with the Phase 1 trade deal on (or around) August 15, which is incidentally the anniversary of the end of Bretton Woods. |

China Caixin Services Purchasing Managers Index (PMI), July 2020(see more posts on China Caixin Services PMI, ) Source: investing.com - Click to enlarge |

Meanwhile, the US Health and Human Services Secretary will visit Taiwan shortly. As the highest-ranking US official to visit Taiwan since the US cut ties in 1979 will likely antagonize Beijing. Taiwan is one of the potential flashpoints as the status quo looks increasingly unstable. The US does not have a mutual defense treaty with Taiwan. The US strategy has been focused on the sales of high-level weaponry. Beijing sanctioned Lockheed Martin last month of such sales. The suppression of Hong Kong appears to be boosting the support for Taiwan’s President, while some HK dissidents are going to Taipei. Reported, China continues to harass Taiwan, entering its waters and airspace.

Japan’s services PMI was revised slightly higher to 45.4 from 45.2. This, coupled with the previous upward revision in the manufacturing PMI (45.2 from 42.6) lifted the composite to 44.9 from 43.9. It underscores the impression that Japan’s recovery slower than other G7 countries. One effect seems to be undermining support for Prime Minister Abe, where the latest JNN poll shows his support has fallen to a new low of 35.4%. Many in Japan appear to want the government to declare a new state of emergency to get the virus back under control, but the cabinet is reluctant.

The dollar’s strong rally at the end of July (from ~JPY104 to ~JPY106) saw follow-through at the start of the week to almost JPY106.50 and the 20-day day moving average. However, the upside momentum faded, and the greenback slipped back to around JPY105.50 today. It is confined to around a 30 bp range above there in quiet turnover today. Although the expiring option for about $560 mln at JPY106 does not appear in play, the $2.2 bln option at JPY105 that expires today may attract interest. The Australian dollar has punched back above the $0.7200-mark for the first time this week after correcting lower from nearly $0.7230 seen at the end of last week. The intra-day technicals leave scope for marginal new highs but are getting stretched. The greenback has fallen about 0.45% against the Chinese yuan, which is a large move for this tightly managed pair. It is below CNY6.95 for the first time since mid-March. The reference rate for the dollar was set slightly lower than the bank models suggested.

EuropeThe main economic news from Europe today is the downward revisions to the service and composite PMIs from Germany and France that were partly blunted on the aggregate level by stronger readings in Italy and Spain. |

Eurozone Retail Sales YoY, June 2020(see more posts on Eurozone Retail Sales, ) Source: investing.com - Click to enlarge |

| The German services PMI was revised to 55.6 from 56.7, while the French reading was revised to 57.3 from 57.6. These revisions from the preliminary estimate saw the composites changed to 55.3 (from 55.5) and to 57.3 (from 57.6) for Germany and France, respectively. |

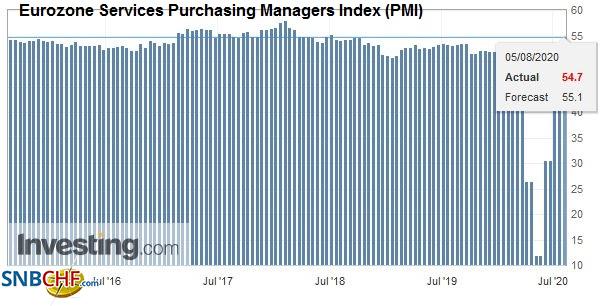

Eurozone Services Purchasing Managers Index (PMI), July 2020(see more posts on Eurozone Services PMI, ) Source: investing.com - Click to enlarge |

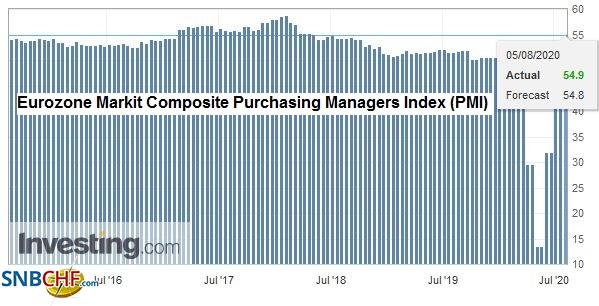

| Italy’s July services PMI rose to 51.6 from 46.4, and Spain rose to 51.9 from 50.2. The Italian composite reading improved to 52.5 from 47.6. Spain’s rose to 52.8 from 49.7. This all translates to a slightly softer EMU services PMI of 54.7 rather than 55.1 of the preliminary estimate. However, the composite was revised to 54.9 from 54.8. |

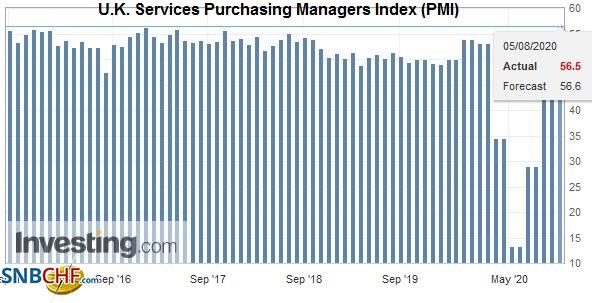

U.K. Services Purchasing Managers Index (PMI), July 2020(see more posts on U.K. Services PMI, ) Source: investing.com - Click to enlarge |

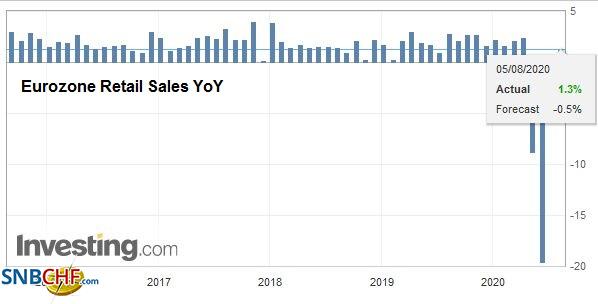

| Recall that EMU’s composite PMI was 48.5 in June. Separately, the eurozone reported that June retail sales rose by 5.7% instead of the 6.1% economists anticipated. Offsetting the disappointment was the upward revision in May’s surge to 20.3% from 17.8% initially. |

Eurozone Markit Composite Purchasing Managers Index (PMI), July 2020(see more posts on Eurozone Markit Composite PMI, ) Source: investing.com - Click to enlarge |

In the spot market, it looks like the dollar fell by 0.7% yesterday against the Turkish lira, its biggest decline in two months. Yet it conceals the turmoil in the offshore market, where the interest rate on currency swaps blew out to over 1000%, according to reports, and the implied yield of forwards jumped above 250%. Part of Turkey’s strategy has been to asphyxiate the offshore market to reduce speculative sales of the lira, for which the central bank has sold billions of dollars to defend. It appears that an offshore participant sought to cover a short lira position and found there was no market. Signs of pressure were evident in other parts of the capital markets. The price of five-year credit default swaps rose almost 4% to a little more than 582 basis points. Turkish share fell 3.0%-3.5%, as the domestic markets re-opened for a holiday on both last Friday and this Monday. The lira is under strong downside pressure today, and the dollar has surged more than 1.8%, the most in four months to reach almost TRY7.0345. This is the weakest the lira has been in nearly three months.

The euro is extending yesterday’s gains to reach almost $1.1850. Last week’s high was about $1.1910. The euro’s gain suggests the euro’s pullback turned out to last about two days and two cents. Our target of $1.1650 proved too low. That said, the intraday technicals are stretched, making a run to last week’s high difficult to envision immediately. Sterling reached a high last week near $1.3170 and pullback back to about $1.2980 yesterday. It has recovered to almost $1.3125 today. The Bank of England meets tomorrow and is expected to standpat, but signal that it will likely take more measures in the coming months.

America

Senate Majority leader McConnel acknowledged that no stimulus package will find unanimous support about the Republicans. Although we have suggested that this was the case, the official recognition of it is important. It means that another stimulus bill will require more Democrat votes, and this means that the bill will likely be larger than when the Republicans thought they could power through with only a few Democrats on board. There are good economic and political reasons for another stimulus bill. The White House and Democrats are negotiating, and for the first time, there seems to be some progress, including possibly a national moratorium of evictions and something larger than had been offered before to replace the $600 a week federal unemployment insurance. This could set the stage for another fiscal boost in September or Q4. The fissure in the Republican Party may have an adverse impact on its future electoral fortunes.

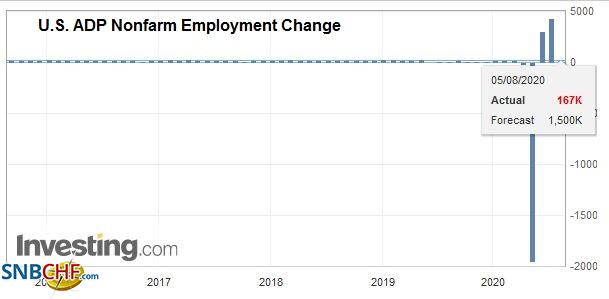

| The US sees the ADP private-sector jobs estimate. A huge back month revision last month may undermine the market impact of the report, but it is expected to confirm the slower pace of job growth that economists expected to be seen in the national report at the end of the week. The median forecast in the Bloomberg survey calls for a 1.2 mln job gain, roughly half of its initial estimate for June. Markit reports its final services PMI, while the ISM services index is expected to slip to 55.0 from 57.1. |

U.S. ADP Nonfarm Employment Change, July 2020(see more posts on U.S. ADP Nonfarm Employment Change, ) Source: investing.com - Click to enlarge |

| The June trade deficit will be reported, and with the advanced goods report and Q2 GDP done and dusted, it is unlikely to have much market impact. That said, a deficit of much different than around $50 bln may prompt talk of revisions to Q3 GDP. The API estimated US oil inventories fell by 8.6 mln barrels last week, and if echoed with the EIA official estimate today, it would put US holdings near four-month lows. Canada reports its merchandise trade balance for June, and a slightly wider deficit is expected. Brazil’s central bank meets, and the consensus is for a 25 bp rate cut. We suggest the risk is that it also announces a bond-buying program. |

U.S. Trade Balance, June 2020(see more posts on U.S. Trade Balance, ) Source: investing.com - Click to enlarge |

The US dollar is trading at new five-month lows against the Canadian dollar after being sold through CAD1.3315. The next target is near CAD1.3200. The low for the year was set in January around CAD1.2950. The implied volatility is rising at near 7% (three-month); it is at its highest level in over a month. The US dollar stopped shy of our MXN23.00 target yesterday, getting up to almost MXN22.91 before pulling back. If that is the high, the greenback could slip back to MXN22.35-MXN22.40 near-term, on its way back to the MXN22.00 area. The US dollar firmed to a two-week high against the Brazilian real near BRL5.3760 before reversing and settling at BRL5.2865. Additional dollar losses are likely today, and the initial target may be around BRL5.15.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Brazil,China,Currency Movement,Featured,newsletter,Taiwan,Turkey