Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

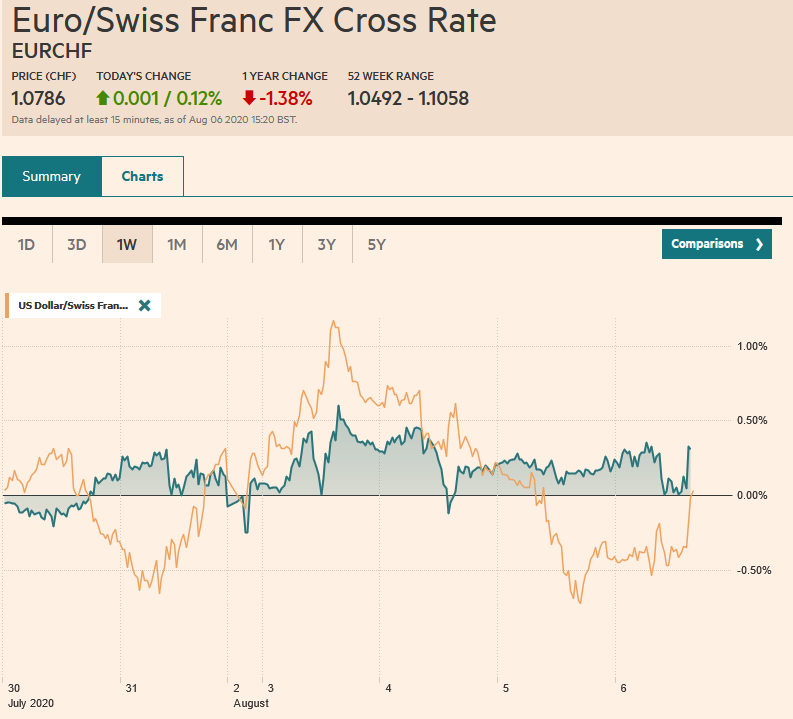

Swiss FrancThe Euro has risen by 0.12% to 1.0786 |

EUR/CHF and USD/CHF, August 6 Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The Australian dollar powered to marginal news highs for the year as the move against the US dollar continued yesterday. The euro stopped a few hundredths of a cent below the high seen at the end of last week. However, neither sustained the upside momentum and have come back offered today. The greenback is narrowly mixed against the major currencies, with sterling performing best, encouraged perhaps by the more upbeat message from the Bank of England. Led by the continued sell-off of the Turkish lira (~3%), emerging market currencies are on the downside as well. The JP Morgan Emerging Market Currency Index is lower for the fifth session in the past six. Equities are mostly lower. In the Asia Pacific regions, Chinese, Japanese, and Hong Kong markets edged lower. Still, the rest of the area was higher, led by India, where the central bank refrained from cutting rates as many expected. European shares are a little heavier. Since the 2% rally on Monday, the Dow Jones Stoxx 600 is consolidating at (~0.5%) lower levels. US shares are little changed after the S&P 500 closed a gap left on the charts from the breakaway move in February. Asia Pacific bond yields may have been dragged higher by the backing up in US rates yesterday, but the US 10-year is back around 52 bp, and European yields are 2-3 bp lower. Gold was hovering a little below the $2055 record-high set yesterday. Oil is heavy, with the September WTI contract trading nearly $2 lower than yesterday $43.50 peak. The 200-day moving average, which it has not surpassed in six months is just above $43.85. |

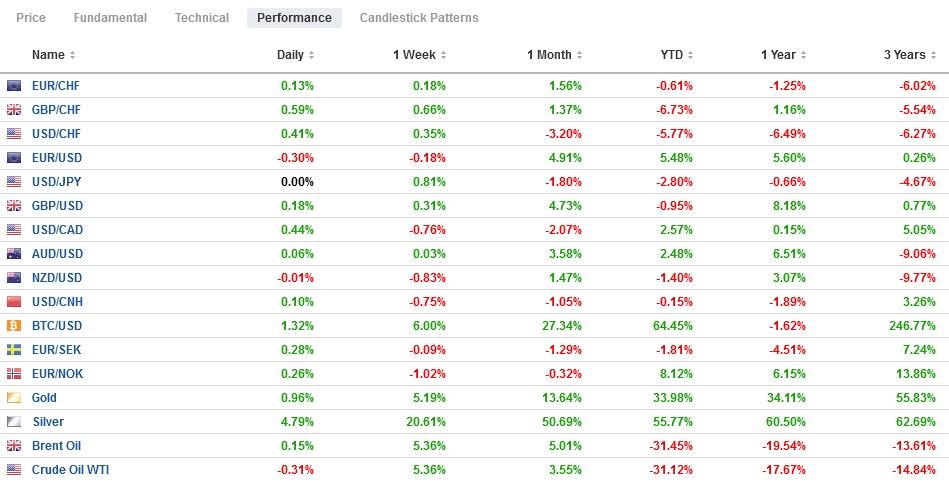

FX Performance, August 06 - Click to enlarge |

Asia Pacific

As the US opens up a new front in the confrontation with China over apps, China says it wants to avoid a Cold War, though stopped short of suggesting any change in behavior. US Secretary of State indicated a broader push against Chinese apps beyond TikTok. He wanted “untrusted” Chinese apps to be removed from app stores, for US companies not to make apps available for Huawei phones, and refrain from using China’s cloud services. Separately, China announced that effective at the start of this week, it would cut the transaction fees for currency transactions for a dozen emerging markets currencies for three years to help facilitate the Belt-Road Initiative.

The Reserve Bank of India surprised many with its standpat decision. The repo rate remains at 4% and the reverse repo at 3.35%. We had thought another rate cut was likely as the economy remains in poor shape (July composite PMI 37.2 vs. 37.8 in June), and price pressures are expected to fall. We suspect the RBI will still feel pressure to cut rates this year after today’s pause.

Japan and the UK appear to be getting closer to reaching a trade agreement. It seems to be mostly rolling over the treaty with the EU to the UK. This is particularly important for the auto sector. In Japan, there has been some suggestion to unwind last year’s controversial sales tax increase, but the LDP policy chief rejected it. Lastly, the MOF reported that Japanese investors stepped up their foreign bond-buying last week. The JPY1.15 trillion (~$11 bln) of net new purchases was the most in a couple of months.

The dollar is trading within yesterday’s roughly JPY105.30-JPY105.85 trading range. Indeed it has been confined to about 15 ticks on either side of JPY105.55. There are nearly $2 bln of options struck between JPY105.60 and JPY105.85 that expire today. There is another option for $660 mln at JPY105.25 and $445 mln at JPY106.00 that also expire today. The Australian dollar is also consolidating within yesterday’s range. Some momentum traders are disappointed that it did not maintain the upside momentum yesterday after new highs for the year were recorded. Two sets of expiring options may be important in the North American morning. The first is about A$525 mln at $0.7195 and another A$520 mln at $0.7150. Yesterday’s low was a little above $0.7150. The Chinese yuan weakened for the first time since Monday. The PBOC set the dollar’s reference rate at nearly in line with the bank models at CNY6.9438. Today is the fifth session that the dollar has not been above CNY7.0. Meanwhile, the US dollar remains pinned to its floor against the Hong Kong dollar.

EuropeAs widely anticipated, the Bank of England stuck to its policy stance but seemed more upbeat than expected. Governor Bailey reaffirmed that negative rates remain a tool in its kit, but said there were no plans to use it. UK rates firmed a little, but the curve remains below zero out seven years. The BOE’s Gilt purchases are going to slow to GBP4.4 bln a week from around GBP6.9 bln. In the worst of the financial crisis in March and April, the UK’s purchases peaked near GBP13.5 bln a week. The BOE suggested the economic hit and the loss to banks may not be as great as feared in May, though the risks were on the downside. It sees Q2 contraction near 21% (due next week) and rebounding by 18% in Q3. Inflation is expected to remain below 1% until Q2 21. German factory orders surged in June, and the details are among the most promising signs of the European recovery. Factory orders jumped 27.9%. The median forecast in the Bloomberg survey was for little more than a 10% gain in line with the 10.4% rise in May. It suggests that Q2 German GDP may be revised up from the initial estimate of -10.1%. Capital equipment orders were particularly strong. Domestic orders rose by a heady 35.3% and orders from the eurozone, where exports have been soft, rose by 22.3%. Orders from outside of the eurozone rose 31.7% after a minor 1.4% increase in May. Separately, the IFO reported that the number of German workers n the shortened hours program (Kurzarbeit) fell to 5.6 mln in June from 7.3 mln in May. The euro made a marginal new high near $1.1915 before retreating to around $1.1840 in early European turnover. The market appears to want to push higher. The profit-taking after new highs are reached suggests short-term momentum traders are an important part of the story. There are not large options expirations to note today, but tomorrow there are two option strikes that could be important. The first is for 1.1 bln euros at $1.1850, and the second is for 1.2 bln euros at $1.19. Sterling too has made a marginal new high just shy of $1.3185. The high since the Covid-crisis struck was $1.3200 in early March. The year’s high is closer to $1.3285. Support is seen near $1.3100. |

EUR/BGN Currency Pair - Click to enlarge |

America

In the US, Canada, and to a less extent, Mexico, the resumption of auto production serving as a catalyst, as it were, for factory orders, manufacturing, and trade. Mexico reports June’s vehicle production and exports today. Increased domestic sales of autos in North America are helping boost consumption measures. While US auto sales increased in July (14.5 mln unit seasonally adjusted annual pace vs. 13.06 mln in June), it appears that last month’s manufacturing and retail sales recovered a slower rate than June (due next week). Several Fed officials have acknowledged what the NY Fed’s weekly economic activity index suggests that the economy has lost some momentum.

Ahead of tomorrow’s national employment figures, and ADP’s estimate plays up fears of a disappointing report, the US reports weekly jobless claims. Weekly jobless claims have risen for the past two weeks by 126k after bottoming in mid-July near 1.3 mln. Economists look for a small decline to 1.4 mln from 1.434 mln in the week ending July 25. That improvement is unlikely to be sufficient to boost optimism. Moreover, signs from Washington suggest that White House and Democrat negotiators are wide apart and cannot even reach agreement on the broad framework. President Trump is said to be considering executive action.

As widely expected, Brazil’s central bank delivered a 25 bp rate cut to bring the Selic rate to a record low of 2%. In the unanimous decision, the central bank kept the door ajar to an additional cut. It did not indicate plans to use its authority, granted by Congress earlier, to buy sovereign and corporate bonds. The central bank warned that the government’s fiscal plans could be inflationary. The key to the outlook maybe next month’s budget proposals for 2021.

The US dollar fell to six-month lows against the Canadian dollar (~CAD1.3235) yesterday and remains near those lows as the North American dealers return to their posts. Initial resistance is seen in the CAD1.3300-CAD1.3315 area. Employment data for both the US and Canada will be reported tomorrow. The US dollar pulled back after approaching MXN23.00 in the middle of the week. It has found support near MXN22.30, a little below the 20-day moving average. However, with the downward trajectory of US rates, look for the MXN22.60 area to cap the greenback’s bounce.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Bank of England,Brazil,China,Currency Movement,Featured,India,newsletter