Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

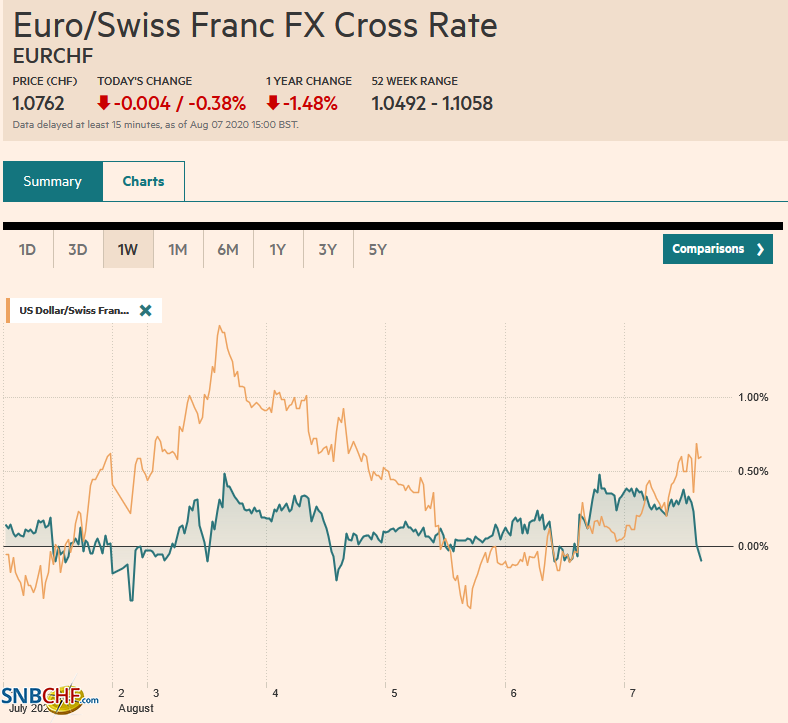

Swiss FrancThe Euro has fallen by 0.38% to 1.0762 |

EUR/CHF and USD/CHF, August 7(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

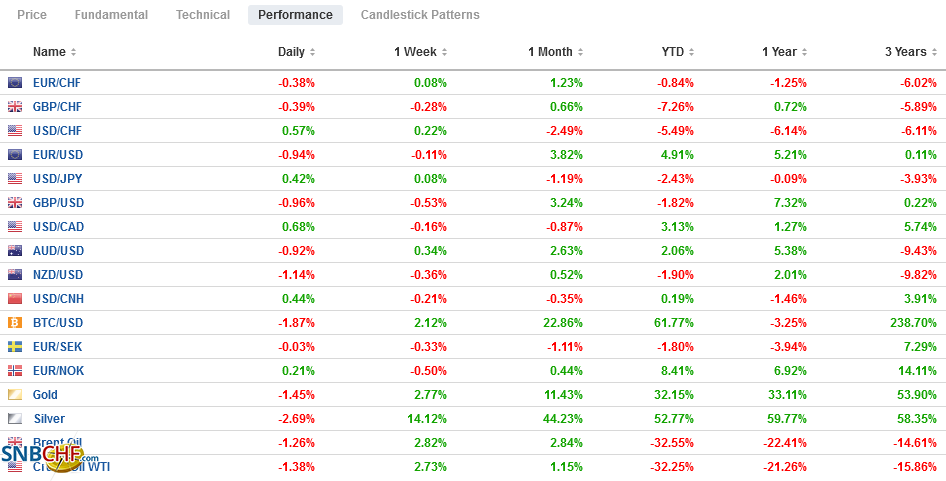

FX RatesOverview: Escalating dramas may be behind the position adjustment today ahead of the US jobs data. The US and China feud expanded beyond Tiktok to WeChat, and efforts to tighten disclosure rules for Chinese companies listed in the US are nearing. The negotiations between the White House and the Democrats broke down, preventing or at least delaying additional stimulus. The US reimposed 10% tariffs on unprocessed aluminum from Canada, while Ottawa threatened dollar-for-dollar retaliation. After making new highs for the move yesterday, the euro and sterling have come back offered, and the dollar is enjoying a broad bounce. Most of the major currencies are off by around 0.40%-0.60% near midday in Europe. The yen is faring better, nursing marginal losses. Let by the continued sell-off of the Turkish lira and South African rand (~-1.0%), emerging markets currencies are lower, pushing the JP Morgan Emerging Market Currency Index down around 1.2% for the week, which would be the largest loss in almost two months. Gold rose to a new high (~$2075) before it, too, saw profit-taking that pushed it back to $2048-$2050. September WTI reached $43.50 in the middle of the week and is consolidating nearly $2 a barrel lower. It finished last week near $40.25 a barrel. |

FX Performance, August 07 - Click to enlarge |

Asia Pacific

The US banned TikTok and WeChat. WeChat’s parent Tencent was walloped, falling around 10% at one point and pushed the Hang Seng down by 2.3% before closing about 1.6% lower. Separately, reports suggest that the US SEC is getting closer to tightening the disclosure rules for Chinese companies listed in the US.

While the drama with the apps plays out, the US still has not terminated the extradition treaty with Hong Kong as Germany, the UK, Australia, and New Zealand have done. Several Chinese companies have listed in the US over the last couple of months, and Chinese trade data seems unperturbed by the symbolic actions and rhetoric. Defying economists’ forecasts for a fall in Chinese exports, they rose by 7.2% (year-over-year) after June’s 0.5% gain. Imports fell by 1.4%. Economists had anticipated a small increase. The net result is an eye-popping trade surplus of $62.33 bln (~$46.4 bln in June).

Of particular interest, exports to the US rose by 12.5% (year-over-year), the strongest in a couple of years. Imports from the US rose by 3.6% (11.3% in June), leaving them down 3.5% year-over-year, while the Phase 1 trade agreement, of course, called for an increase not only over 2019 but over 2018 as well. China’s trade surplus of $32.46 bln with the US was a little smaller than the March and April surplus put together (~$38 bln). Separately, China’s oil imports eased by 3.6% on the month, while industrial metal imports jumped (iron ore +11% month-over-month and copper ore (+13%). China’s steel exports rose by 13%.

The sharp swings in the foreign exchange market last month appear to be helping lift the dollar value of central bank reserves. Earlier this week, South Korea reported a $4 bln increase to $416 bln. Today, Japan said its reserves rose by $19.3 bln, the most in six years, to $1.402 trillion. China’s reserves rose by $42 bln to $3.154 trillion, the most in six years.

The dollar is in a 20 pip range against the yen below JPY105.70. Yesterday’s range was about 40 pips and the day before a little more than 50. There is an option for almost $800 mln at JPY105.50 that expires today and for $1.7 bln that expires on Monday. Today, there are also options for $1.2 bln struck between JPY105.80 and JPY106.00 that also expire. The Australian dollar made a marginal new high for the year today but again was rebuffed in ahead of $0.7250. A convincing break of the $0.7180 area may point to losses toward $0.7120. The PBOC again set the dollar’s reference rate in line with the bank models. The dollar gained marginally to pare this week’s loss to about 0.25%.

Europe

Ideas that the eurozone recovery is more robust than the US got a boost from the June industrial output figures. The ball got rolling with Italy’s report yesterday that showed a stronger than expected rise of 8.2% after the 41.6% increase in May. Today’s Germany, France, and Spain followed suit with better than expected output figures. France reported a 12.2% increase following a nearly 20% recovery in May. Spain’s industrial production rose 14% in June, almost matching the May increase. Germany reported stronger than expected factory orders yesterday and an acceleration in industrial production in June (8.9% vs. 7.8% in May).

Germany also reported trade figures that also point to a broader recovery. Exports rose by nearly 15% in June, above market expectations and on top of the 8.9% gain the previous month. The pace of imports nearly doubled to 7% in June from 3.6% but was below forecasts. The net result is a doubling of the monthly trade surplus to 15.6 bln euros from 7.0 bln euros in May.

The Turkish lira is off a little more than 1% today to bring this week’s drop to around 5% and sits at new record lows. It appears that the central bank’s effort to worth through the state banks to support the lira has been abandoned. The central bank issued a statement saying it would unwind some of the liquidity measures taken to support the economy but said nothing about rates. Three-month implied volatility has doubled from last month’s lows to over 24%, the highest since April. The skew in the 3-month gives calls a 9% premium over puts.

The euro made a new high yesterday near $1.1915 and has retreated to test the $1.18 area in the European morning, just above a three-day low. The low for the week was set on Monday a little below $1.17. There is an option for 1.2 bln euros at $1.1850 that will be cut today. On Monday, an option for 2.7 bln struck at $1.18 expires. At the end of last week, we thought there was potential toward $1.1650, but new buying emerged well ahead of it. Sterling reached about $1.3185 yesterday and has been sold to about $1.3085 so far today. The week’s low was set nearly a cent lower. A US employment report that does not alter generally held views could see North American traders, who appear to have led the dollar’s recent decline, take advantage of the dollar bounce to sell.

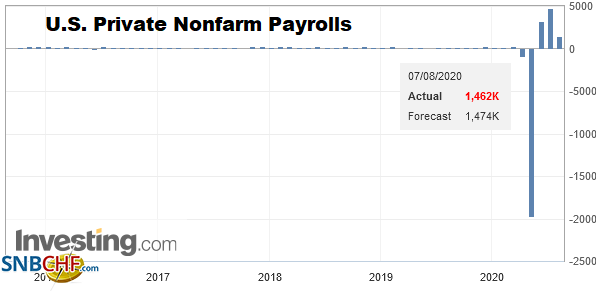

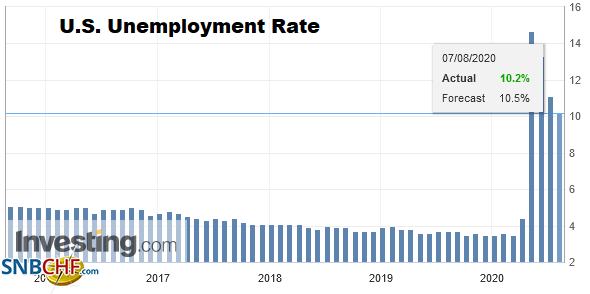

United StatesA week ago, the median forecast in the Bloomberg survey was for a gain of 1.75 mln jobs in today’s US jobs report, of which 375k were to be in manufacturing. As more economists submit their forecast and others update theirs, the median has fallen to 1.4 mln, and the number of manufacturing jobs project was reduced to 266k. The median loss of government jobs (overall minus private sector) has fallen to 280k from 450k a week ago. Of course, there have been new inputs too. he ADP estimate was unnervingly low at 167k (vs. median forecast of 1.2 mln). Admittedly, the past two month’s massive revisions (May from -2.8 mln to +5.8 mln and June from 2.4 mln to 4.3 mln) need to be taken into account. The ISM services employment index fell to 42.1 from 43.1. Challenger estimated that layoffs rose by 54% in July over June, the third-largest increase this year. Weekly initial jobless claims fell last week (249k) after increasing by 127k in the previous two weeks, but the week for which the non-farm payroll survey was conducted, they had fallen by 100k from the same week in June. None of these measures are without their flaws, but the takeaway is that a general impression that the recovery stalled as the virus flared up. That this is discounted explains the modest reaction to the ADP report and the latest weekly jobless claims. This means that there probably is a wide range of jobs data that will not really tell investors and businesses anything new. In the Bloomberg survey with 79 forecasts, only two were looking for an outright loss of jobs (500k-600k). At the high-end was a forecast for 3.2 mln and a total of four projections of three million or more. In June, the US created 4.8 mln jobs. |

U.S. Private Nonfarm Payrolls, July 2020(see more posts on U.S. Nonfarm Payrolls, ) Source: Investing.com - Click to enlarge |

| It probably will take something closer to it that would suggest strong momentum going in this month when roughly 12 mln people lose their $600 a week federal unemployment insurance, which will likely weaken consumption. Unfortunately, the payroll savings tax cut that President Trump is reportedly considering mandating by executive order, but it may only involve collecting the taxes, which would not help those who are not on a payroll, and companies would likely put aside the taxes anyway. |

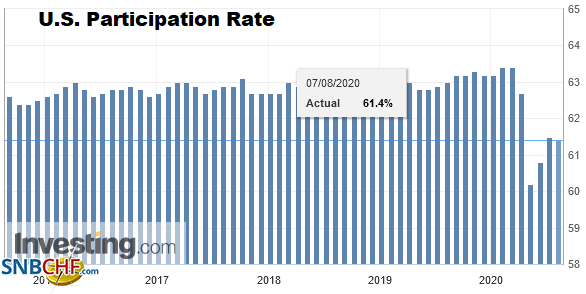

U.S. Participation Rate, July 2020(see more posts on U.S. Participation Rate, ) Source: investing.com - Click to enlarge |

U.S. Average Hourly Earnings YoY, July 2020(see more posts on U.S. Average Hourly Earnings, ) Source: Investing.com - Click to enlarge |

|

U.S. Unemployment Rate, July 2020(see more posts on U.S. Unemployment Rate, ) Source: Investing.com - Click to enlarge |

Canada also reports July employment data today. In March and April, it lost about three million jobs, and in May and June gained 1.25 mln. It has recouped a little more than 40% of the jobs. Economists expect another gain of almost 400k jobs (953k in June). One issue is how many jobs lost were permanent and how much is temporary (whatever that means). In turn, this may depend on how much an economy will be able to open up without a vaccine.

The US dollar found support near CAD1.32 in the middle of the week. It consolidated yesterday and is moving higher today. Resistance is seen in the CAD1.3400-CAD1.3430 area. An expiring option for $1.2 bln at CAD1.3400 may be relevant. Mexico and Brazil are expected to report an uptick in July CPI today. Mexico’s is expected to edge up to 3.62% from 3.33%. It bottomed in April at 2.5% year-over-year. Brazil’s inflation bottomed in May near 1.8% and is expected to have risen to 2.30% from 2.13% (have to appreciate the precision of reporting CPI to a hundredth of a percent). The greenback firmed to almost MXN23 (~MXN22.91) early this week and backed off to find support near MXN22.30. Initial resistance is seen near MXN22.60 today. The US dollar has gained about 1% against the peso this week and is coming into today with around a 2% gain against the Brazilian real.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Canada,China,Currency Movement,Europe,Featured,jobs,newsletter,Trade,Turkey