Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

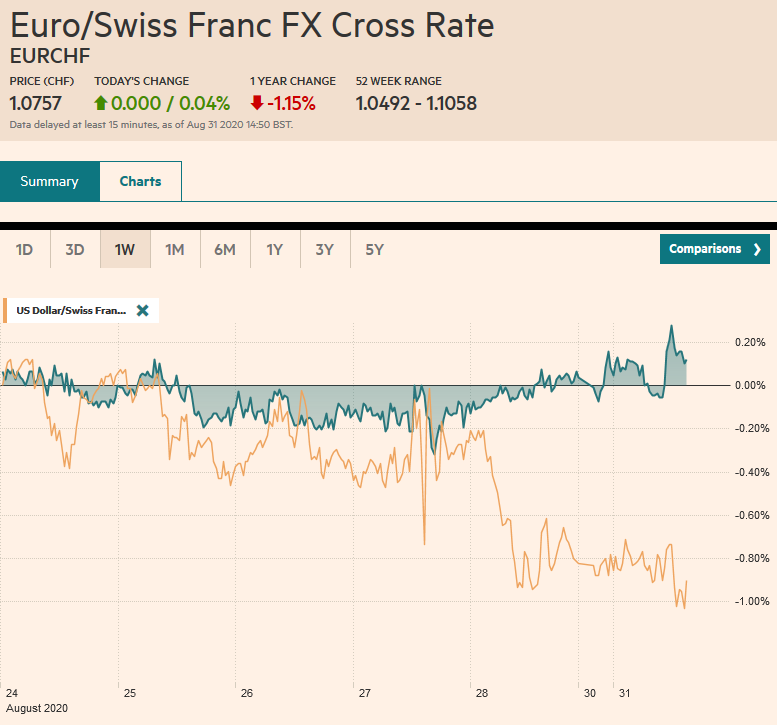

Swiss FrancThe Euro has risen by 0.04% to 1.0757 |

EUR/CHF and USD/CHF, August 31(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Markets are searching for direction at month-end. Asia Pacific shares outside of Japan lower. Berkshire Hathaway confirmed taking a $6 bln stake in Japanese trading companies over the past year, and the pullback in the yen helped lift shares. The MSCI Asia Pacific Index rose 2% last week. European bourses are higher, and the Dow Jones Stoxx 600 is up around 0.4% near midday, while the S&P 500 is poised to gap higher, as it did last Monday. Debt markets are also mixed. European yields are 1-2 bp higher, while the US 10-year benchmark is about two basis points higher at 74 bp. The dollar is mostly higher, though the Norwegian krone and Canadian dollar are resisting the tug. Most of the liquid accessible emerging market currencies, led by the South African rand and the Mexican peso, are weaker. The JP Morgan Emerging Market Currency Index, which had rallied 1.2% before the weekend, is about 0.25% lower today. Gold is consolidating after rising 1.2% last week. The shuttered US Gulf oil and refinery capacity is offsetting news of two new oil and gas field finds in Saudi Arabia, and October WTI is firm near $43.50. |

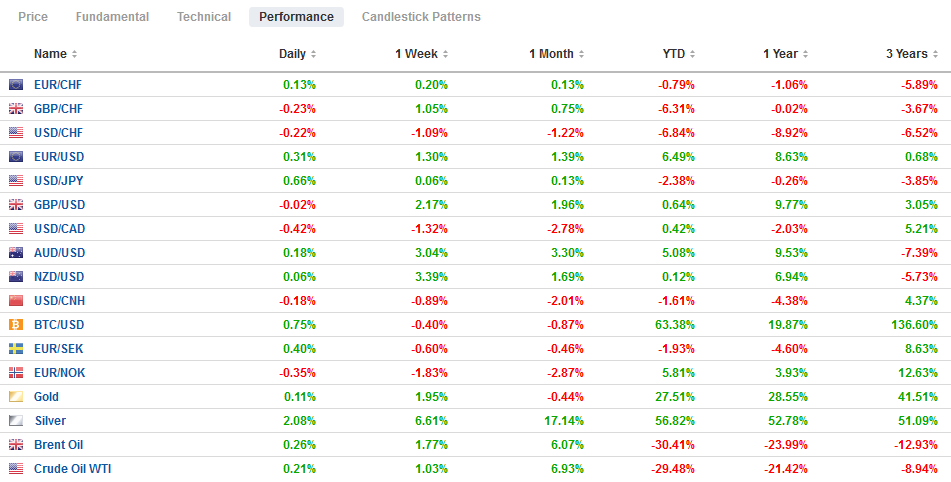

FX Performance, August 31 - Click to enlarge |

Asia Pacific

Deputy Prime Minister Aso will not replace resigning Prime Minister Abe. Instead, Abe will remain in office until the LDP chooses a successor around the middle of September. LDP parliament members and local LDP chapters will select the next party head, who, by virtue of its parliamentary majority, would become the next PM. Before Abe, the office appeared to have a revolving door for several years. The current parliament term ends next October. It is possible that an interim compromise candidate completes Abe’s term and allows the factions within the LDP to jostle and prepare for the post-Abe era. BOJ Governor Kuroda’s term extends to April 2023. He may step down earlier, and a new Prime Minister would ostensibly give him he opportunity, though, without the extensive international travel schedule, Kuroda may feel more energetic to deal with the challenges of recovery. The fall in Tokyo’s August inflation back below zero reminds us that the victory against deflation has not been secured.

It seemed kind of naive just to assume that Beijing was simply going to roll-over and allow Washington to arrange (and demand a fee!) for Tik-Tok to be sold (or banned from the US). Chinese officials waited until the end of last week to announce new export restrictions that would seem to cover some of the underlying technology used by Tik-Tok. The restrictions require an additional level of government approval. The list had not been altered since 2018. Changes have reportedly been discussed before, but it is clear that the current circumstances influenced its move that looks is designed to hamper Tik-Tok’s sale. Beijing is willing to sacrifice Tik-Tok’s US presence rather than capitulate to Washington’s demand.

| China’s August PMI showed the recovery remains intact. The manufacturing PMI slipped to 51.0 from 51.0. New orders rose to 52, while the contraction in export orders slowed. |

China Manufacturing Purchasing Managers Index (PMI), August 2020(see more posts on China Manufacturing PMI, ) Source: investing.com - Click to enlarge |

| The service PMI rose to 55.2 from 54.2. These combined to lift the composite to 54.5 from 54.1. |

China Non-Manufacturing Purchasing Managers Index (PMI), August 2020(see more posts on China Non-Manufacturing PMI, ) Source: investing.com - Click to enlarge |

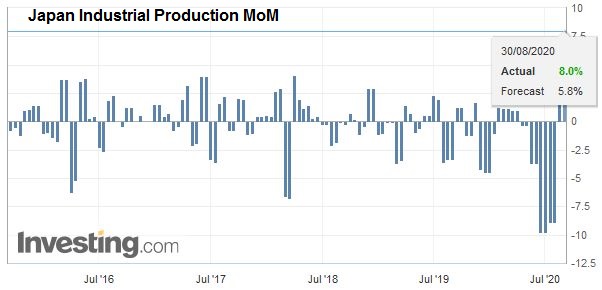

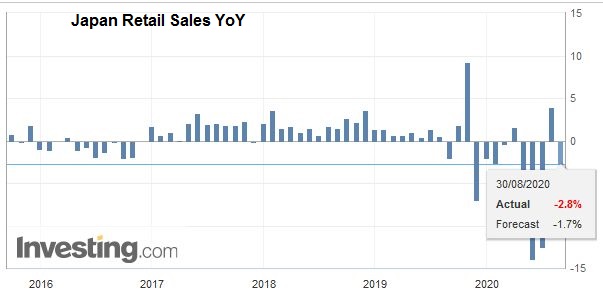

| Japan reported its industrial output recovered smartly, but the recovery in consumption is less convincing. When China reported similar developments, some observers blamed the command economy for focusing on supply rather than demand. |

Japan Industrial Production MoM, July 2020(see more posts on Japan Industrial Production, ) Source: investing.com - Click to enlarge |

| Yet, it is complicated by the fact that many manufacturing workers were regarded as essential. And social distancing impacts services more. In any event, industrial output jumped 8% in Japan in July after a 1.9% gain in June. The median Bloomberg forecast was for a 5% gain. Retail sales fell 3.3% in July (13.1% gain in June). The median Bloomberg forecast was for a 2.5% decline.

The dollar’s big outside down day before the weekend against the Japanese yen did not generate follow-through selling. The greenback remains well within the JPY105-JPY107 range of August. There is a roughly $440 mln option at JPY106 that expires today. The Australian dollar made a marginal new high to $0.7380 before consolidating in a narrow range. A break of $0.7340 could signal a 20-40 point pullback. The PBOC set the dollar’s reference rate at CNY6.8605, a little higher than the bank models suggest. The dollar fell a little below CNY6.8450 today to its lowest level since January 20 when it reached nearly CNY6.8400. Separately, the Hong Kong Monetary Authorities continue to intervene to prevent the US dollar from falling below its band. |

Japan Retail Sales YoY, July 2020(see more posts on Japan Retail Sales, ) Source: investing.com - Click to enlarge |

EuropeТhe UK’s standstill arrangement with the EU since leaving at the end of last year ostensibly ends on December 31. However, in reality, if there is no agreement by the mid-October EU summit, there may not be sufficient time to ratify the deal. This put the onus on the negotiations in the coming weeks. They do not look good. Both sides seemed to recognize the lack of progress. Reports suggest that the UK’s chief negotiator Frost has signaled to the EU negotiator Barnier that he is prepared to recommend that the UK prepares to leave without an agreement if the EU continues to demands that rules on state-aid ar aligned. It seems only reasonable then that the EU wants to understand the UK’s plans for its post-EU subsidy thrust, but apparently will not be available until at least the end of September. |

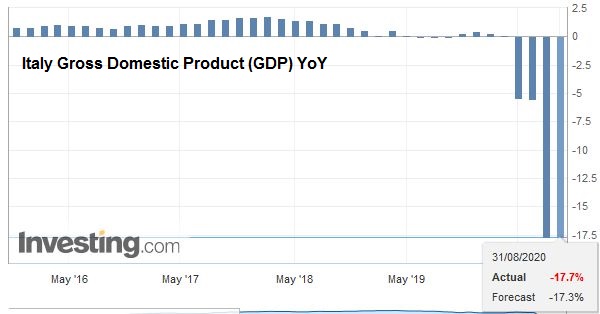

Italy Gross Domestic Product (GDP) YoY, Q2 2020(see more posts on Italy Gross Domestic Product, ) Source: investing.com - Click to enlarge |

| Despite negative interest rates, over a trillion euro of loans with a yield of minus 100 bp, and a dramatic expansion of fiscal policy, the eurozone continues to wrestle with disinflation if not deflationary pressures. It will be driven home by this week’s preliminary August CPI. It is only reasonable to ask if the new Fed initiative will impact the ECB. Currently, the ECB targets “close to but below 2%”. It is engaged in its own framework review. The perceived wisdom is that to boost inflation, it is important to lift inflation expectations. How to raise inflation expectations? The Fed says it will accept an above-target increase in the general price level. What can the ECB do? Would simply adopting a straight-forward 2% inflation target be sufficient? There seems some sympathy for an average inflation target, but there is likely to be resistance from the hard-money camp. |

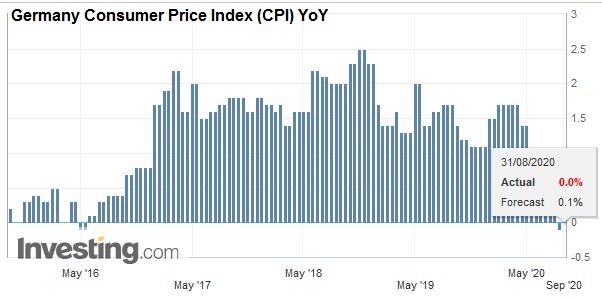

Germany Consumer Price Index (CPI) YoY, August 2020(see more posts on Germany Consumer Price Index, ) Source: investing.com - Click to enlarge |

In fact, the French (last week), Spanish and Italian August inflation readings point to a poor number for the aggregate figure out tomorrow. Recall France reported last week that its harmonized measure slowed to 0.2% year-over-year from 0.9%. Spanish numbers out today showed a year-over-year decline of 0.6%, and Italy’s harmonized measure fell 0.5% year-over-year from +0.8% in July and expectations for -0.3% reading. Germany states are reporting ahead of the national figures that will be out shortly. It is expected to be flat on the month and up 0.1% from a year ago (zero in July).

The euro rose to almost $1.1930 in Asia before pulling back to around $1.1885 in early Europe. There is an expiring option for 1.4 bln euro at $1.19 that no longer seems relevant. The high recorded this month was near $1.1965 on August 18. That seems a bit of a reach today. Remember that since the euro’s launch in 1999, its average price has been $1.20. Sterling initially extended last week’s gains too, rising to almost $1.3370 before meeting sellers in Europe who pushed it to $1.3300. Intra-day technicals are extended, and losses below $1.3300 will likely be limited, keeping the $1.3250 option expiry (~GBP272 mln) out of play.

America

The FOMC disguised its embrace of ad hocery with talk about an average inflation rate. Average implies a specific period, and Powell was clear that this was being eschewed. “In seeking to achieve an inflation average of 2% over time, we are not tying ourselves to a particular mathematical formula that defines average.” It does not simply formalize the downgrade of the Phillips Curve, but it is the rejection of rule-based decision-making entirely. The average 2% inflation is as aspirational as the 2% target previously. It does not mean that it will be achieved. Still, if nothing else, it is an expression of forward guidance that US rates stay low for longer. Today’s highlight outside is the Fed’s Vice Chairman Clarida, who will discuss the new policy framework before the equity market opens today. Judging from other Fed officials who have discussed it, there seems to be a reluctance to remove the intentional, strategic ambiguity.

A few weeks after putting a new tariff on aluminum from Canada, the US moved against Brazilian steel by cutting its quota. Brazil, who agreed on a quota in 2018 to avoid tariffs, has seen its exports to the US slow but not as much as others. The new limits come following bilateral talks and the threat of a 25% tariff. Further talks will be held at the end of the year. Seeing how the US treated fellow-USMCA partners and Brazil, Mexico took preventative action. President AMLO imposed a new pre-approval process for steel exports to the US. Starting at the end of this week, the extra check will ensure that the steel has not been re-routed from a third country. Separately, today Argentina finds out if a sufficient number of creditors have accepted its offer to restructure $65 bl of its foreign debt.

The US dollar is trading lower against the Canadian dollar for the fifth consecutive session, but it is within the pre-weekend range (roughly CAD1.3050-CAD1.3135). The greenback has not traded below CAD1.30 since January 8. Despite the Canadian dollar persistent gains (seven weeks in a row), speculators in the futures market continue to carry a net short position. The US dollar edged toward MXN21.74 before rebounding to around MXN21.85. Initial resistance is seen in the MXN21.90-MXN21.92 area. Recall that the June low was near MXN21.4650, and the 200-day moving average is around MXN21.4750. The greenback has fallen for the past three weeks against the peso.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Brazil,Brexit,China,Currency Movement,ECB,Featured,FOMC,Japan,Mexico,newsletter