Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

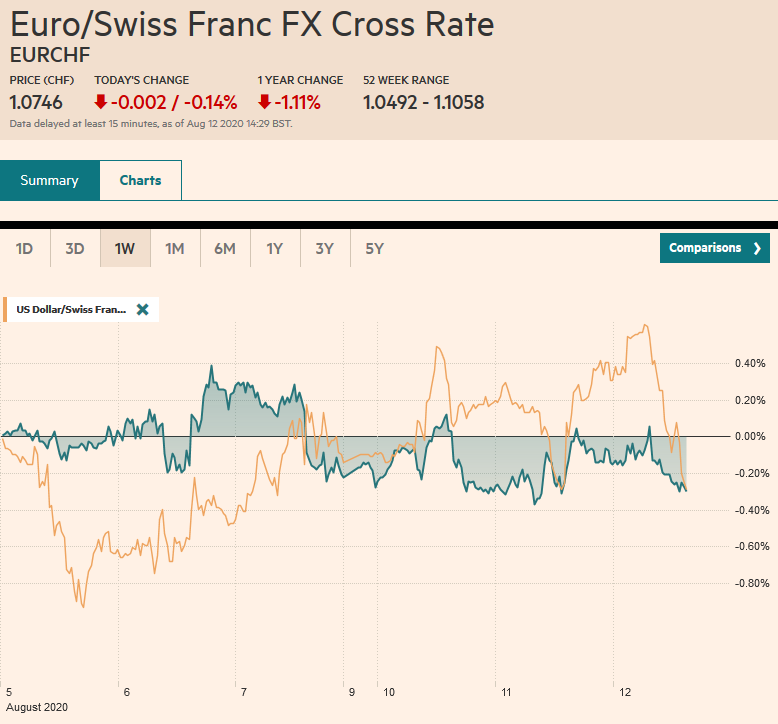

Swiss FrancThe Euro has fallen by 0.14% to 1.0746 |

EUR/CHF and USD/CHF, August 12(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The biggest rise in the US 10-year yield in a couple of months, as the record quarterly refunding, got underway may have helped stabilize the dollar after an earlier decline. The S&P 500 threatened to extend its advance for the eighth consecutive session yesterday, but a late sell-off stopped it cold after scaling to new five-month highs. Although it posted a key reversal by closing below Monday’s low, there has been no follow-through selling, and higher share prices point to an opening gain of around 0.6%. The NASDAQ continued to underperform. Asia Pacific equities were mixed. The weaker yen helped lift Japanese shares, while Hong Kong and Korean shares continued to advance. However, other markets in the region, including China, Taiwan, Australia, and India fell. European stocks edging higher, but the Dow Jones Stoxx 600 remains a few percentage points off last month’s high. Bond yields are 2-4 bp firmer across the board, which puts the US benchmark yield near 68 bp. A week ago, it was approaching 50 bp. New Zealand’s expansion of its asset purchases helped New Zealand bonds buck the move, and the benchmark 10-year yield is almost 5 bp lower near 71 bp. The New Zealand dollar joins the yen as the weakest of the majors today. The Scandis are the strongest. The Turkish lira remains under pressure, falling another 1.4% or so against the greenback, while most emerging market currencies are little changed. The JP Morgan Emerging Market Currency Index is posting a small gain after yesterday’s 0.35% gain, the largest in a couple of weeks. Gold dropped like a ton of bricks, losing around 5.7% in its largest drop since April 2013. It sliced through our $1950 target and skidded to nearly $1863 in Asia. It recovered to back to $1950 before the buying dried up in early Europe. Oil remains firm after the API estimated US inventories fell for the third consecutive week. The September WTI contract looks pinned between the 20-day moving average near $41.30 and the 200-day moving average around $43.65. |

FX Performance, August 12 - Click to enlarge |

Asia Pacific

The Reserve Bank of New Zealand left its cash rate target unchanged at 25 bp but announced an NZD$100 bln expansion of its long-term asset purchase program. Unlike other major countries, New Zealand’s fiscal initiatives remain aggressive and are larger and more front-loaded than the RBNZ had anticipated. However, with Auckland back under lockdown, the central bank kept its options open going forward. It suggested three areas it could move, which itself is a bit of forward guidance. It could launch a term lending facility (long-term cheap loans), cut the cash rate further (though so far, no current account deficit country has adopted negative policy rates), or purchase foreign assets. The latter shows that the exchange rate is on the central bank’s radar screen too.

The US sanctions on 11 Hong Kong officials that were recently announced put Chinese banks in an awkward position. They have to honor the US actions by not doing business with the said officials or risk their access to US dollar funding. According to press reports, Chinese banks are complying. At the end of last year, the top four Chinese banks had around $1.1 trillion of dollar-funding. Of course, Chinese officials loath complying, but the dependence of dollar funding drives home the long reach of the US and the role of the dollar in the world economy. In retaliation, Beijing sanctioned eleven US officials, but with little teeth compared with the US.

No date has been set for senior US and Chinese officials to review the Phase 1 trade agreement. It is still expected in the coming days. By most reckoning, China’s purchases of US goods trails far behind where it ought to be if it were on track to comply with the $200 bln increase over 2017 levels by the end of next year. Reports suggest Beijing wants to talk about US actions to ban TikTok and WeChat next month if they are still under Chinese ownership. The former may not be, but the latter will. China does not allow US giants, like Google and Facebook, though US actions were not tit-for-tat, cited on national security grounds.

The dollar extended its recovery off the JPY104 approached at the end of July and now has poked through JPY106.80 for the first time in more than three weeks. However, the momentum is stalling, and the intraday technicals warn of a likely pullback in North America. Initial support is seen near JPY106.40. A $1.1 bln option at JPY106 expires tomorrow (a smaller one expires there today, but is unlikely to be impactful). After peaking near $0.7190 yesterday, the Australian dollar was sold down to around $0.7110 in regional turnover before recovering to about $0.7135 in Europe. Additional near-term gains are likely to be capped ahead of $0.7150. The PBOC set the dollar’s reference rate a touch firmer than the bank models at CNY6.9597. The dollar slipped against the yuan for the third consecutive session, the longest losing streak in a little more than a month.

EuropeTwo issues are coming to a head this week that may underscore the divergence between the US and Europe, and that divergence may continue on the other side of the US elections. First, there is an opportunity to review the tariffs, accepted by the WTO, for the illegal subsidies given to Airbus. Some reports suggest that new tariffs on alcohol are under consideration. And, incidentally, the UK may not be in the EU, and it may be seeking a free-trade agreement with the US, but it will not protect it in these matters. Second, the US is pressing at the UN Security Council to make the ban on arms sales to Iran permanent. Europe has failed to achieve a satisfactory workaround after the US withdrew, and Iran is pushing the envelope under the treaty. Europe broke from the US decision to unilaterally withdraw from the deal and does not want to accept a fait accompli now. Russia and China threaten to veto it if it got to a vote, which itself requires a 2/3 majority. |

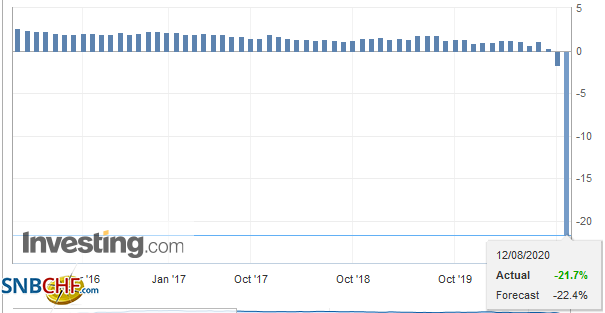

Eurozone Industrial Production YoY, June 2020(see more posts on Eurozone Industrial Production, ) Source: investing.com - Click to enlarge |

| It was confirmed. The UK Q2 contraction of 20.4% quarter-over-quarter was the largest decline in output seen among the large economies. No sector was spared. Services output fell by 20%, industrial output by 17%, consumption by 23%, business investment collapsed by almost 31.5%. Even government spending fell. Still, the bright spot is that it is history. June output expanded by 8.7%, and May’s output was revised to 2.4% from 1.8%. |

U.K. Gross Domestic Product (GDP) YoY, Q2 2020(see more posts on U.K. Gross Domestic Product, ) Source: investing.com - Click to enlarge |

| The early projection is for the economy to grow by around 13% here in Q3. The magnitude of the Q2 contraction may encourage the government to extend the furlough program (~10 mln people) and could see additional fiscal measures. |

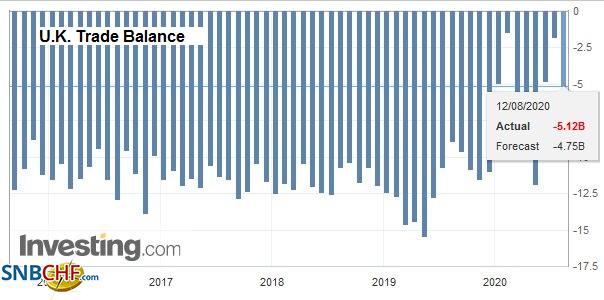

U.K. Trade Balance, June 2020(see more posts on u-k-trade-balance, ) Source: investing.com - Click to enlarge |

The Turkish lira surrendered yesterday’s gains, and the dollar is back straddling the TRY7.3 area. Although Erdogan has called for lower rates, the central bank is forcing funding costs higher. Today, it removed a discount for primary dealers, and funding cots reportedly rose to around 9.75%. This is almost 200 bp more than the July average (~7.35%). Given the elevated volatility, the apparent policy confusion, and the lack of reserves, the rise in funding costs is hardly sufficient to stop the rot.

The euro briefly poked through $1.18 yesterday, but the corrective pressures emerged in late North American dealings, and the single currency did not find support until close to $1.1710 in late Asian turnover. The bounce in Europe brought it back to around $1.1780. The intrasession technical reading is stretched, and another bout of profit-taking is likely in North America today. Similarly, sterling peaked around $1.3130 in North America yesterday and fell to about $1.3010 in Asia earlier today. The bounce in Europe to almost $1.3070 appears to have exhausted the buying and stretched the intraday technical readings. Look for North American operators to sell into these sterling gains.

America

The record quarterly refunding kicked-off with the $48 bln sale of three-year notes for a sliver below 18 bp. The record low yield did not deter investors, and the bid-to-cover was 2.44, a smidgeon higher than the recent average. Another sign of the strength of demand was that primary dealers, who are obligated to participate, took 30.7% of the issue, the least this year. Indirect participants, which include asset managers and foreign central banks, bought 57% of the new three-year note, the most in around 3.5 years. Today, Treasury sells $38 bln of 10-year notes, which is about 9 bln more than last quarter’s sale. On Thursday, it will sell $26 bln of the 30-year bond. Yields have backed up in recent days, despite no new fiscal stimulus and expectations that this week’s economic data will show some moderation from June. The 10-year yield closed 12 bp higher than it was on August 6, and the 30-year yield was nearly 15 bp higher. The bearish steepening saw the 2-10 year curve saw 50 bp for the first time in a month.

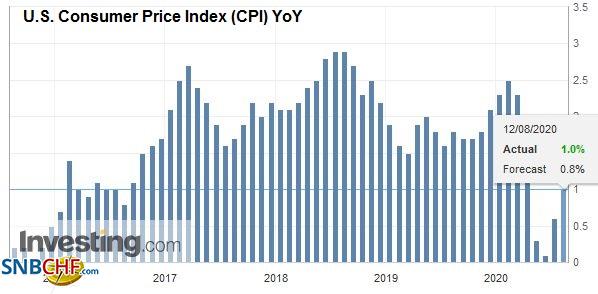

| The 0.6% rise in US headline July producer prices was larger than expected and mostly a function of core prices, which rose by 0.5%. Still, the takeaway is not that inflation is rising. Indeed, with the headline year-over-year rate at -0.4%, deflation is a better description. The core rate of 0.3% suggests disinflationary forces remain. Good prices were lifted by a 5.3% rise in energy prices, while food prices fell by 0.5%. |

U.S. Consumer Price Index (CPI) YoY, July 2020(see more posts on U.S. Consumer Price Index, ) Source: investing.com - Click to enlarge |

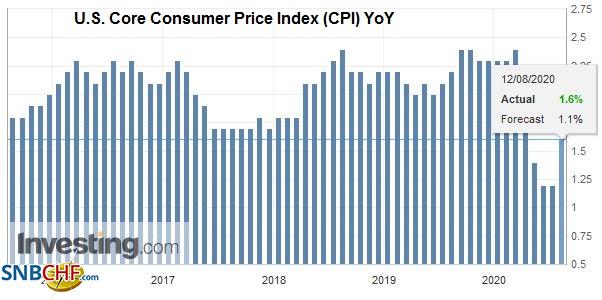

| Prices of final services rose by 0.5%, the most in a little more than a year, led by portfolio management, and vehicle and machine wholesaling costs. Final demand prices for personal consumption rose by 0.5%, while the July CPI on tap today, is expected to increase by 0.3%. If so, the year-over-year rate would edge up to 0.7% from 0.6%. The core rate is forecast to ease to 1.1% from 1.2%. While higher prices in some sectors are possible due to bottlenecks, it is difficult to envision a general increase in prices with the much-unused industrial capacity, a higher level of unemployment than at the peak of the Great Financial Crisis, and a velocity of money that is flatlining. |

U.S. Core Consumer Price Index (CPI) YoY, July 2020(see more posts on U.S. Core Consumer Price Index, ) Source: investing.com - Click to enlarge |

Joe Biden’s pick of Kamala Harris as his Vice-President candidate is not particularly surprising; she was widely seen as a likely, if not the most likely pick. Still, we see little economic significance. It is more about politics, and even here, we do not expect a significant bump in the polls.

The US dollar is trading within yesterday’s range against the Canadian dollar (~CAD1.3270-CAD1.3360). Canada reported strong housing starts data yesterday, underscoring our observation that auto and housing are among the sectors leading the recovery in both the US and Canada. The US dollar is little changed ahead of the North American session, where it seems poised to probe higher. A test on yesterday’s highs seems reasonable. Mexico reported robust June industrial output figures yesterday (17.9%), led by manufacturing. Mining and utility output lagged. A 50 bp rate cut is widely expected to be delivered tomorrow. The dollar slipped to a six-day low yesterday near MXN22.26 before bouncing back to MXN22.50. Although, as the North American dealers return, the greenback is near its lows (~MXN22.30), expect yesterday’s lows to hold and for the dollar to recover.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,China,Currency Movement,Featured,Gold,newsletter,RBNZ,Turkey