Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Swiss Franc |

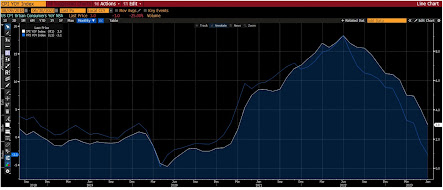

EUR/CHF - Euro Swiss Franc, December 13(see more posts on EUR/CHF, ) - Click to enlarge |

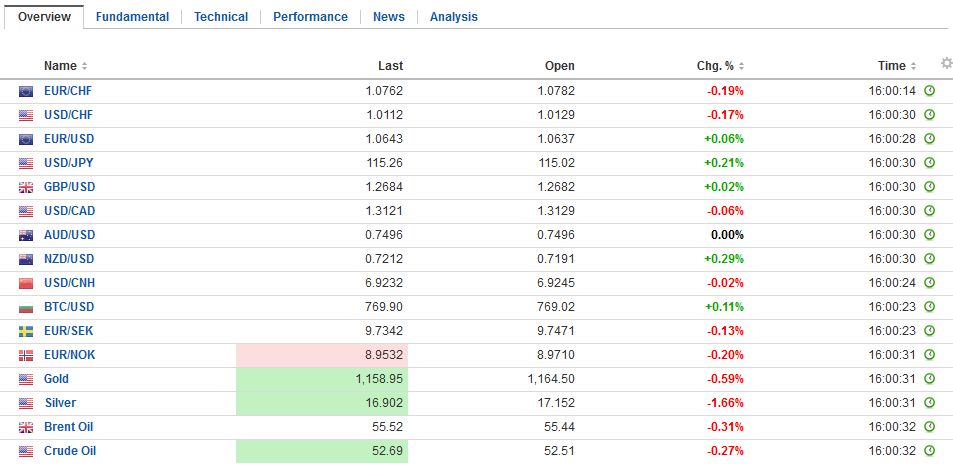

FX RatesThe US dollar is little changed against most of the major currencies. The dollar finished yesterday’s North American session on a soft note, but follow through selling has been limited. After rallying to near 10-month high above JPY116 yesterday, the greenback finished on session lows near JPY115.00. Initial potential seemed to extend toward JPY114.30, but dollar buyers reemerged near JPY114.75, and it rose back the middle of the two-day range (~JPY115.40 area). |

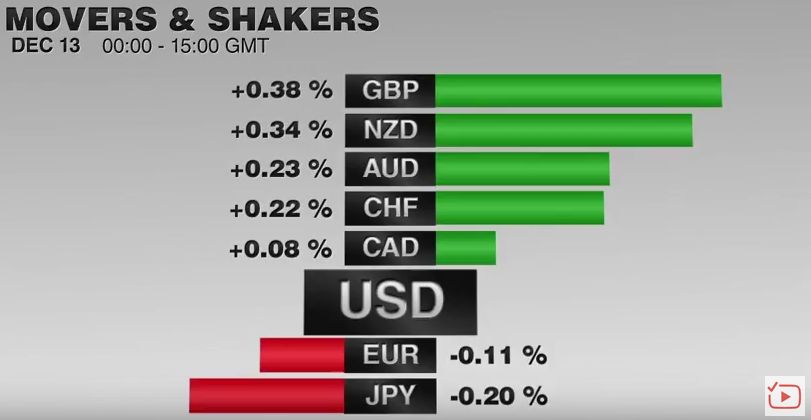

FX Performance, December 13 2016 Movers and Shakers Source: Dukascopy - Click to enlarge |

| The euro was unable to extend yesterday’s recovery that carried it to about $1.0650. It has held above $1.06 so far but looks vulnerable to a push into the $1.0580 area. Sterling is the strongest of the majors, up about 0.2% and extended yesterday’s gains. Last week’s highs are a half a cent higher at $1.2775. However, we suspect that additional gains above the $1.2725 area will require a broader dollar pullback. |

FX Daily Rates, December 13 - Click to enlarge |

| The Nikkei gapped higher yesterday, and despite the lower opening, the gap was not entered, and Japanese stocks recovered. The Nikkei closed 0.5% higher, extended its advance to the sixth consecutive session. The Topix gained a little more, and also extended its streak to six sessions. |

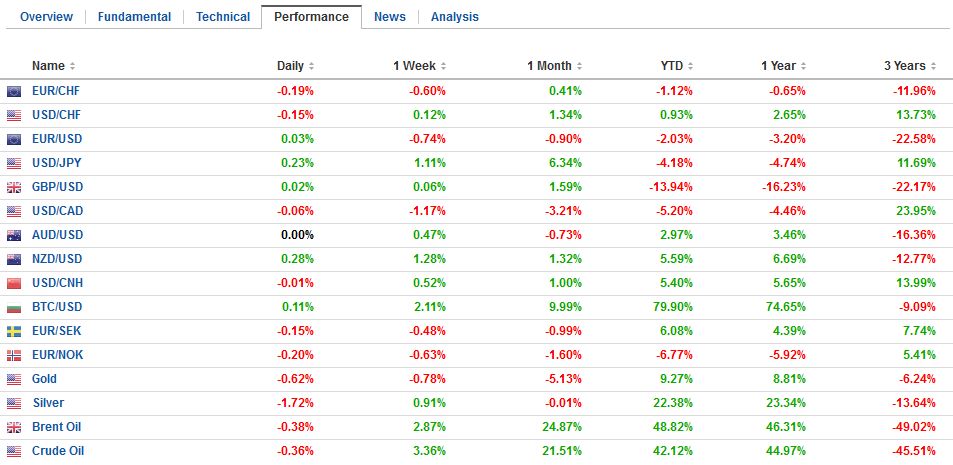

FX Performance, December 13 - Click to enlarge |

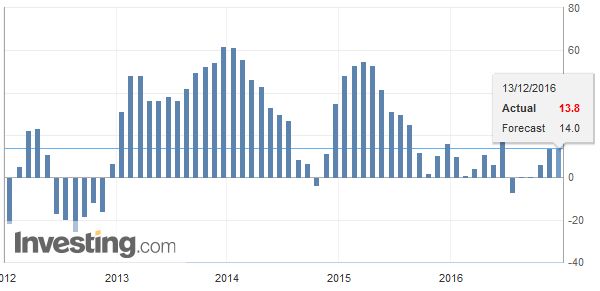

ChinaChina eclipsed Japan in terms of news. The data suggest the economy is finding better traction. November industrial output rose 6.2%. The median expected no change to the 6.1% pace seen in both September and October. It matches the 11-month average. |

China Industrial Production YoY, November 2016(see more posts on China Industrial Production, ) Source: Investing.com - Click to enlarge |

| Chinese shares recovered from early losses. The Shanghai Composite fell 1.1% before recovering to eke out less than a 0.1% gain. Telecom, consumer staples, and energy led the way. Financials were the weakest sector, losing 1.2%. Some reports suggested that the PBOc, operating through a couple of major banks, may have intervened to sell US dollars around CNY6.9, but of course, confirmation remains elusive. |

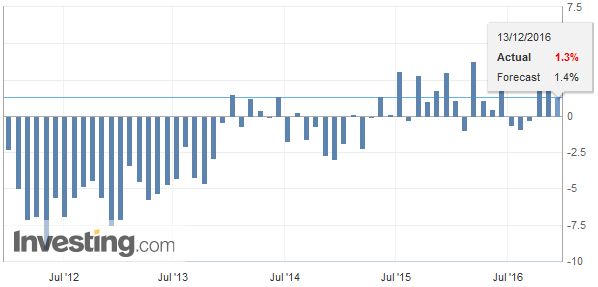

China Fixed Asset Investment YoY, November 2016(see more posts on China Fixed Asset Investment, ) Source: Investing.com - Click to enlarge |

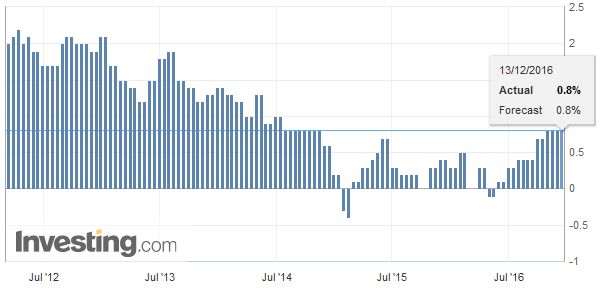

| Retail sales rose 10.8%, the most since last December. The Bloomberg consensus was for a 10.2% increase. Fixed asset investment was steady at 8.3%, as expected. |

China Retail Sales YoY, November 2016(see more posts on China Retail Sales, ) Source: Investing.com - Click to enlarge |

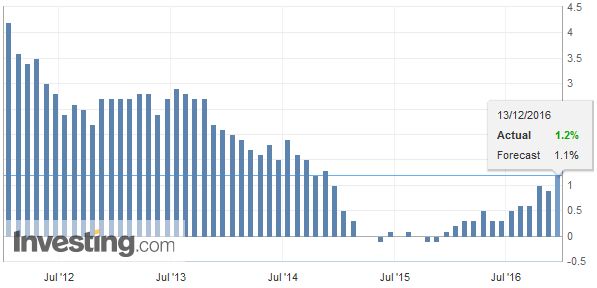

Eurozone Employment Change QoQ |

Eurozone Employment Change, Q3 2016(see more posts on Eurozone Employment Change, ) Source: Investing.com - Click to enlarge |

ItalyEuropean economic data featured Italian industrial output, Germany CPI and ZEW, and UK prices. Like France and Germany, Italy’s October industrial production disappointed. The median forecast was for a 0.2% increase after a 0.8% decline in September. Instead, output was flat, with the year-over-year pace slipping to 1.3% from a revised 1.9% (from 1.8%). Although Italian banks bad loan situation and the need to raise capital is the main focus outside of Italian politics, stronger and sustained growth could ease many of Italy’s problems. Among the banks, Monte Paschi has been the focus as its tries to raise five bln euros, including debt for equity swap. Today it was Italy’s largest bank, Unicredit who announced plans to 13 bln euros in a rights offering next year as part of a larger restructuring effort. Note that amount it wants to raise is almost as much as the present market value. In earlier capital raising exercises in 2008, 2009 and 2012, the bank raised 15.5 bln euros. Italian bank shares opened lower after yesterday’s gains were reversed. However, the FTSE Italia All-Share Banks Index quickly recovered and is up nearly 2.8% near midday in Italy, putting the index near the three-day high. The broader Italian equity market is leading the major bourses higher with a 1.4% gain today. Over the five-day advance is 4..8%, matching the Nikkei’s advance over the same period. The Dow Jones Stoxx 600 is up 0.6% today and is up 3.3% over the past five sessions. Most sectors are higher, but energy and materials. Italy’s 10-year benchmark yield is off nine bp is leading the decline in European bond yields today. Germany’s is off three basis points, while Spain is off two. .Germany’s CPI match the preliminary estimate, leaving the year-over-year rate at 0.7%. The ZEW survey showed a rise in the assessment of the current situation (63.5 from 58.8), while the expectation component was unchanged at 13.8%. |

Italy Industrial Production YoY, November 2016(see more posts on Italy Industrial Production, ) Source: Investing.com - Click to enlarge |

Spain Consumer Price Index (CPI) YoY |

Spain Consumer Price Index (CPI) YoY, November 2016(see more posts on Spain Consumer Price Index, ) Source: Investing.com - Click to enlarge |

Germany CPI |

Germany Consumer Price Index (CPI) YoY, November 2016(see more posts on Germany Consumer Price Index, ) Source: Investing.com - Click to enlarge |

Germany ZEW Economic Sentiment |

Germany ZEW Economic Sentiment, November 2016(see more posts on Germany ZEW Economic Sentiment, ) Source: Investing.com - Click to enlarge |

United KingdomThe UK reported CPI readings a little firmer than expected. The year-over-year headline rate rose to 1.2%, the highest in two years. The core rate rose to 1.4% from 1.2%. The decline in sterling is adding to the inflation pressures. UK import prices rose almost 15% in the year through November, the quickest pace in five years. ONS reported that clothing, motor fuels, and electronic equipment prices rose most. Output prices rose 2.3%, which is also a bit quicker than expected. It is the strongest rise since April 2012. Input prices fell 1.1% on the month, but the year-over-year pace quickened to 12.9% from a revised 12.4% (was 12.2%). The Bank of England meets this week. It is expected to tolerate upward pressure on prices, though its tolerance is not infinite. Base effects and sterling may obfuscate the underlying signal until H2 17. |

U.K. Consumer Price Index (CPI) YoY, November 2016(see more posts on U.K. Consumer Price Index, ) Source: Investing.com - Click to enlarge |

United States

The news stream in North America will be subdued today, with only import prices on tap. A soft report is expected. Things pick up tomorrow with the retail sales, PPI, industrial production, and, of course, the FOMC meeting.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,$CNY,$EUR,$JPY,China Fixed Asset Investment,China Industrial Production,China Retail Sales,EUR/CHF,Eurozone Employment Change,Germany Consumer Price Index,Germany ZEW Economic Sentiment,Italy,Italy Industrial Production,newslettersent,Spain Consumer Price Index,U.K. Consumer Price Index