Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Risk of 50 bp cut by the Fed Tomorrow Keeps the Greenback on the Defensive

Risk of 50 bp cut by the Fed Tomorrow Keeps the Greenback on the Defensive17 Sep 2024

Little Discussion about the US Budget Deficit in the Debate, But Falling Yields Drag the Greenback Lower11 Sep 2024

Fragile Turn Around Tuesday6 Aug 2024

Market Boosts Odds of a BOE Rate Cut this Week29 Jul 2024

Yen’s Surge Continues, while PBOC Surprises with Another Rate Cut, and US 2-30 Year Yield Curve Ends Inversion25 Jul 2024

Euro Trades Quietly Ahead of ECB Meeting18 Jul 2024

Market Takes JPY Lower Despite Intervention Speculation, While Sterling Shines12 Jul 2024

No Turn Around Tuesday as Greenback Remains Firm2 Jul 2024

Greenback Consolidates Last Week’s Surge25 Mar 2024

Powerful Short Squeeze Continues to Lift the Yen11 Jul 2023

Yen: Short Overview24 Apr 2023

Japan Surprises

Japan Surprises20 Dec 2022

Caution Advised in Chasing FX, but Wow!11 Nov 2022

The Yen and Yuan Continue to Weaken7 Sep 2022

EMU GDP Surprises, while the Yen’s Short Squeeze Continues29 Jul 2022

What Happened Today in a Few Bullet Points4 Jul 2022

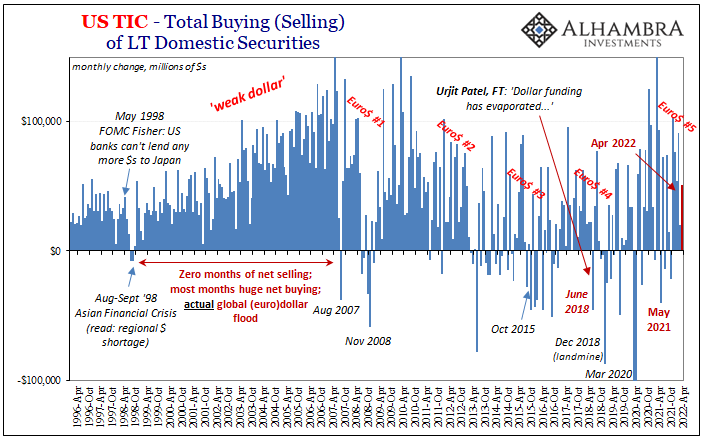

Angry April TIC Zeroed In On China’s CNY and Japan’s JPY21 Jun 2022

Expect the Unexpected from the Fed

Expect the Unexpected from the Fed28 Apr 2022

Yen Blues19 Apr 2022

Greenback Starts New Week on Firm Note18 Apr 2022

Expect the Unexpected from the Fed

2022-04-28

by Stephen Flood

2022-04-28

Read More »