Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss Franc |

EUR/CHF - Euro Swiss Franc, December 14(see more posts on EUR/CHF, ) - Click to enlarge |

|

The Pound is entering mid-December in the same fashion it begun the month after having a very strong November as well. After being buoyed by Donald Trump’s victory and the High Courts ruling that parliamentary approval is needed before invoking Article 50, the Pound has been boosted further after economic data has also impressed, with yesterday being a good example of this. Yesterday morning it was announced that UK inflation rose 1.2% in November. The expectation was for 1.1% so the improvement on this figure confirms that prices are increasing at a faster rate than analysts have been expecting. Whilst the data release was welcomed by Sterling bulls and the Pound gained yesterday approaching the 1.30 mark, should the inflation figure begin to exceed 2% I think the Pound could come under pressure. The next market mover this week could be this mornings UK Employment data at 9.30am and then on Thursday the Bank of England will be announcing its most recent interest rate decision. Although no change is expected I think there could be swings within GBP/CHF exchange rates if the BoE offer us much of an insight into their plans for next year. |

GBP/CHF - British Pound Swiss Franc, December 14(see more posts on GBP/CHF, ) - Click to enlarge |

FX RatesThe global capital markets are subdued going into the FOMC meeting. The dollar is little changed. Equities are trading with a slight downside bias, while bond markets are firm. Italian bonds and stocks continue to outperform their European counterparts. There have been three new economic reports that add to the macro picture today: Japan’s Tankan survey, China’s credit figures, and the UK employment report. |

FX Performance, December 14 2016 Movers and Shakers Source: Dukascopy - Click to enlarge |

| However, before tomorrow and the BOE and Norges Bank meetings is today’s FOMC meeting. A 25 bp increase is so widely expected that the failure to deliver it would be more destabilizing than a hike. The aspirational policy of the new US Administration is not the basis on which monetary policy can be formed. It may disappoint some participants if the FOMC’s economic projections are little changed from September. Many hope that the outlook for fiscal policy will be clearer by the March meeting when the forecasts are updated, but that may be optimistic. The new Administration does not take off until late January, and it seems to have indicated that trade will be its first economic focus, not stimulus, which will have to be carefully negotiated with Congress. |

FX Daily Rates, December 14 - Click to enlarge |

| The market will likely take its cues from the dot plot rather than the statement. The press conference will also be important because it is there that Yellen will be pressed about how the Fed thinks about fiscal policy. It will also likely be the forum in which the steepening of the yield curve will be discussed. There are some who argue that the steepening of the term structure means that the Fed may be slipping behind the curve of inflation expectations. We expected Yellen to deftly deflect concerns about the Fed’s independence. Given the length of terms and other considerations, it is possible that the next president can nominate a majority of the Board of Governors over the next 18-24 months. |

FX Performance, December 14 - Click to enlarge |

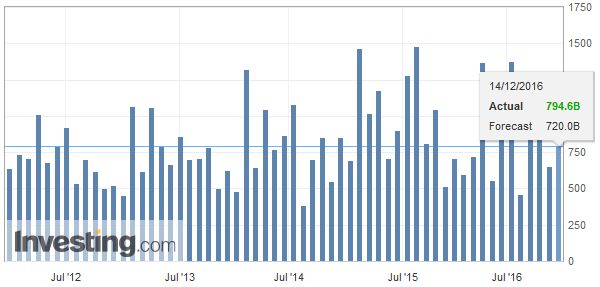

ChinaThe Chinese economy appears to be stabilizing but at the cost of another large rise in aggregate financing. Aggregate financing rose CNY1.74 trillion, almost twice the CNY896 bln in October, and the largest since March. The breakdown suggests that around 2/3 can be accounted for by new mortgage lending. With the economy seemingly on stronger footing, officials may do more next year to rein in some of the excesses. China also reported that its foreign exchange deposits rose 11.4% in the year through November. In October the increase was 4.8%. Like the recent reserve data, it provides further evidence of capital outflows. Separately, we note that the tax incentive to buy small autos in China is to expire at the end of the month. Many hoped it would simply be renewed as it has proven helpful to boost auto sales. However, official reports suggest it will be raised to 7.5% from 5%. Initially, it had been set at 10%. |

China New Loans, November 2016(see more posts on China New Loans, ) Source: Investing.com - Click to enlarge |

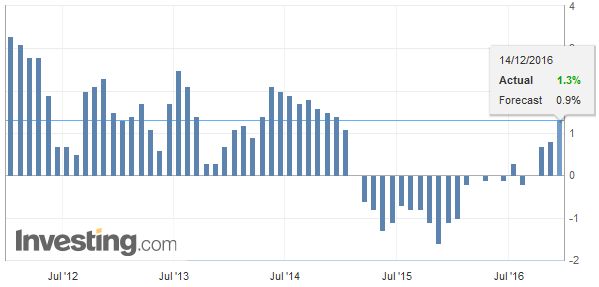

United KingdomThe UK employment data was decidedly mixed. The claimant count rose by 2.4k increased of the 6.5k of the Bloomberg median, However, the October series was revised to 13.3k from 9.8k. Regular earnings (excluding bonuses) rose 2.6% in the three-month year-over-year period through October, compared with 2.4%. It is the fastest pace since August 2015. However, employment fell for the first in more than a year in the three months through October. The 6k losses are small; it bears out the ONS point that the labor market has leveled out recently. Sterling slipped to test the session low near $1.2640 on the news. There is no implication for tomorrow’s MPC meeting. Policy is expected to remain on hold, and a limited tolerance for a near-term inflation overshoot is likely to be reiterated. The sharp decline in sterling is expected lift prices, but that pressure may ease in H2 17. The central bank of Norway meets tomorrow too. Although its deposit rate is most likely to remain at 0.5%., the risk is fro a dovish signal given krone’s recent strength, especially against the euro. |

U.K. Unemployment Rate, November 2016(see more posts on U.K. Unemployment Rate, ) Source: Investing.com - Click to enlarge |

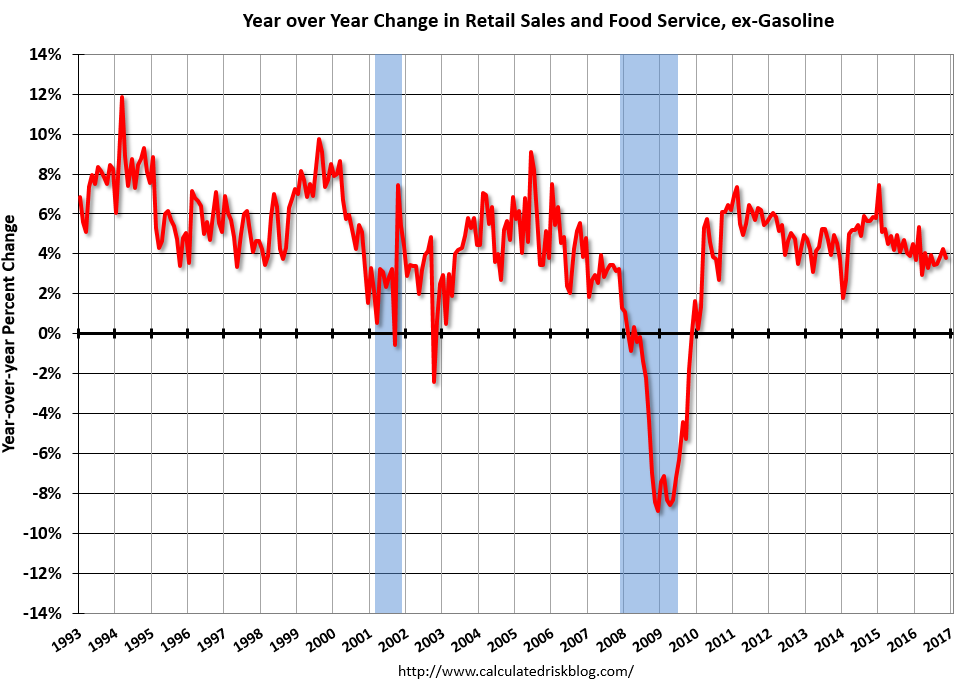

United StatesAhead of the FOMC meeting, the US reports retail sales, PPI, industrial output and business inventories. The most important are the retail sales, which are roughly 40% of the two-thirds or more of the economy accounted for by consumption. After strong gains in October (headline and GDP-measure both rose 0.8%), a milder 0.3% rise is expected. Late yesterday API reported a 4.68 mln barrel build in US oil inventories, and this is weighing on oil prices today after a four-day 6% rally. It makes the official DOE estimate more important today. A 1.35 mln barrel draw is expected. |

US Retail Sales, November 2016(see more posts on U.S. Retail Sales, ) Source: macro.economicblogs - Click to enlarge |

| Flattish PPI followed by a drop in capacity utilization may weigh on yields. |

U.S. Producer Price Index (PPI) YoY, November 2016(see more posts on U.S. Producer Price Index, ) Source: Investing.com - Click to enlarge |

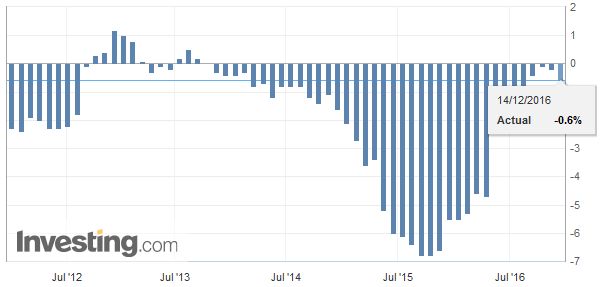

| Industrial output and manufacturing may disappoint. Capacity utilization is expected to slip to 75.1 from 75.3. This would be the lowest usage rate since May. |

US Industrial Production, November 2016(see more posts on U.S. Industrial Production (ZH), ) Source: macro.economicblogs - Click to enlarge |

Switzerland |

Switzerland Producer Price Index (PPI) YoY, November 2016(see more posts on Switzerland Producer Price Index, ) Source: Investing.com - Click to enlarge |

Japan

Japan’s Tankan survey results for large businesses were in line with expectations. The diffusion index for large manufacturers rose to 10 from 6. It is the high for the year, after having been stuck at 6 for the first three-quarters. It is expected to slip to 8 in March 2017. Large non-manufacturers’ sentiment was expected to edge up but was flat at 18. It is expected to slip to 16 in March. Sentiment among small companies posted small gains, which are expected to be short-lived as well.

Perhaps the most disappointing part of the survey was the sharper than expected decline in capex plans. They were reduced to 5.5% from 6.3%. Capex plans in Q1 are often the weakest of the year. It has been the case for the past six years. If Q1 readings were excluded, today’s results show the weakest capex intentions since Q3 13.

Japanese stocks were mixed with the Topix down slightly and the Nikkei up slightly. The Nikkei’s advancing streak extended to it seventh consecutive session. Most other markets in the region saw minor losses. Australia’s ASX200 was the notable exception, rising 0.7%. The MSCI Asia-Pacific Index eked out an ever so small of a gain. Of note, foreign selling of Indonesian equities continued to the 24th consecutive session. However, since December 1 the equity market gained almost 4.5%, but today’s 0.6% fall may have signaled a near-term top.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$JPY,China,China New Loans,EUR/CHF,FX Daily,gbp-chf,newslettersent,Switzerland Consumer Price Index,U.K. Unemployment Rate,U.S. Industrial Production (ZH),U.S. Producer Price Index,U.S. Retail Sales