Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Swiss FrancThe euro continues to weaken against the franc at 1.0922. But the speed of the descent has slowed. The dollar is stronger, in particular against EUR, CHF and AUD. The ECB bond buying program has finally started. For us the main reason of the weaker Euro was, however, the bad US jobs report, that will delay also a normalization of rates in the euro zone. |

via Dukascopy |

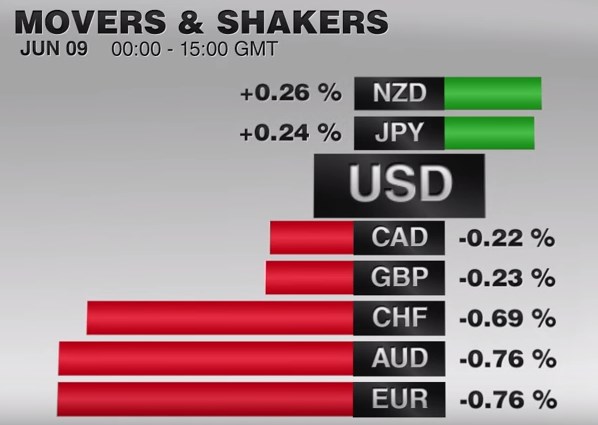

FX RatesThe US dollar is posting modest upticks against most of the European currencies and the Canadian and Australian dollars.However, it has fallen against the yen and taken out the recent low, leaving little between it and the May 3 low near JPY105.50. The New Zealand dollar though is the strongest of the major currencies; gaining 1.5% following the RBNZ’s decision to leave rates on hold, and signal of little urgency to cut again in the near-term. |

Click to enlarge. |

| In recent days, the odds of a New Zealand rate cut had fallen, and like other major central banks appears to be wanting to keep its powder dry. The Kiwi’s push to new highs since last June was also a function of Governor Wheeler’s guidance. He suggested that the output gap has closed and that prices were stabilizing, but could accelerate higher. He explicitly indicated that there was not need for additional stimulus at this juncture. Wheeler also noted the resurgence in house prices. |

Click to enlarge. |

Ironically and counter-intuitively, South Korea surprised the market by delivering a 25 bp rate cut earlier today, to bring the key seven-day repo rate to 1.25%, and the won finished the Asian session stronger than it was at the start. It is the first cut since last June. Only one of 18 economists polled by Bloomberg expected the cut. The won closed marginally higher but firmer than most of the regional currencies, but the Malaysian ringgit and Thai baht. However, the interest rate surprise failed to lift Korean shares, but the 0.15% decline was among the smallest in Asia today.

United StatesFalling interest rates, with 10-year US Treasury yields at their lowest levels since February, and record low Gilt and Bund yields, coupled with falling equities, may be underpinning the yen. Newswires have also played up the idea that several of the largest, or highest profile macro hedge funds, have been talking up their positioning for a renewed crisis. Recall that the recent G7 summit, Japanese Prime Minister Abe had talked about the risks of a Lehman-like crisis, which were widely dismissed part of his effort to build a case to postpone the sales tax hike. The LDP had been instrumental in supporting the sales tax increase that the DPJ government had proposed. The tax deal the coup de grace to the troubled DPJ governments and a revolving door in the prime minister’s office. |

Click to enlarge. |

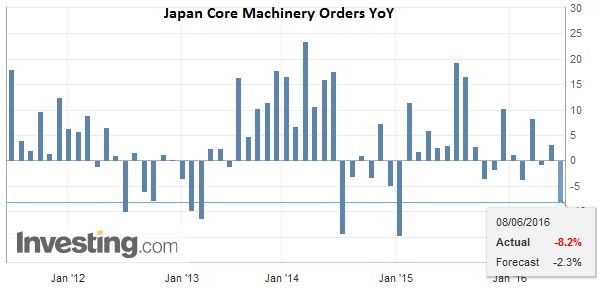

JapanJapan reported machine orders plummeted 11% in April. The median guesstimate was for a 3% decline after a 5.5% rise in March. Machine orders are used as a proxy for capex. Despite Q1 GDP having been revised higher, and speculation that it had undermined the need for more stimulus, the momentum does not appear sustained in Q2. With the July upper house election around the corner, it would not be surprising to see details of the fiscal stimulus being discussed in greater detail next week. Expectations for BOJ easing appear to have been pushed from next week into the end of next month. |

Major economic data – click to enlarge. |

ChinaChina and Taiwan markets were closed today, but this did not prevent China from reporting its inflation figures. Headline inflation CPI was softer than expected with a 2.0% increase year-over-year, down from 2.3% in April. It is the first decline in eight months. It is the lowest since January and reflects the easing of the spike in food prices. Food price inflation fell to 5.9% from 7.4%, while non-food prices were flat at 1.1%. Separately, producer price deflation continues to moderated. In May, it stood at -2.8% after April’s -3.4%. It is the least producer price deflation since November 2014. It is the fifth consecutive month of improvement. The last positive print of Chinese PPI on a year-over-year basis was in January 2012. |

Click to enlarge. |

News from Europe is light and launch of the ECB’s corporate bond buying program is among the main talking points. The ECB’s self-designed rules allow it to buy corporate bonds that at least one of the approved rating agencies regard as investment grade. Although it has not been confirmed by officials, market participants suspect that the ECB did buy a corporate bond yesterday, in the first day of the program, that was rated investment grade by only one agency. The ECB says it will not have to sell the bond if at some point that one rating agency cuts its assessment.

The idea is in buying such an instrument; the ECB is demonstrating its resolve. Nevertheless, we are not convinced that what is holding back investment in Europe is that corporations do not have the funds or that interest rates are too high. For its part, the euro edged closer to our $1.1420 objective in Asia before being sold in Europe to $1.1350. The intraday technicals suggest that the downside in the North American morning may be limited. A retest on the highs seems reasonable, especially given the continued narrowing of the US two-year premium over Germany. That premium stands near 131 bp, which is off about 10 bp in the past week.

The euro has traded on both sides of yesterday’s range, but we would not attribute much significance to it in the current context, where it seems to besimply a slight range extension.The close will be important, and then only a close below $1.1350 would be notable.

More concerning is the Australian dollar’s performance. We have brought to your attention the fact that the Aussie has been a good leading indicator of the US dollar’s direction. It bottomed in mid-January, well before the broader turn in the markets on Feb 11. More recently, it peaked in late-April, while the other currencies did not peak until May 3. It bottomed on May 24, while the other major currencies did not bottom until May 30.

Earlier today the Australian dollar extended its recent gains to near our $0.7500 objective. However, it has since reversed lower and is possibly setting up key reversal. That would require a close below yesterday’s low near $0.7430. Meanwhile, a break of $0.7420 could signal a move toward $0.7380.

Graphs and additional information on Swiss Franc by the snbchf team

Full story here Are you the author?Tags: China Consumer Price Index,China Producer Price Index,FX Daily,Japan Core Machinery Orders,Japanese yen,newslettersent