Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

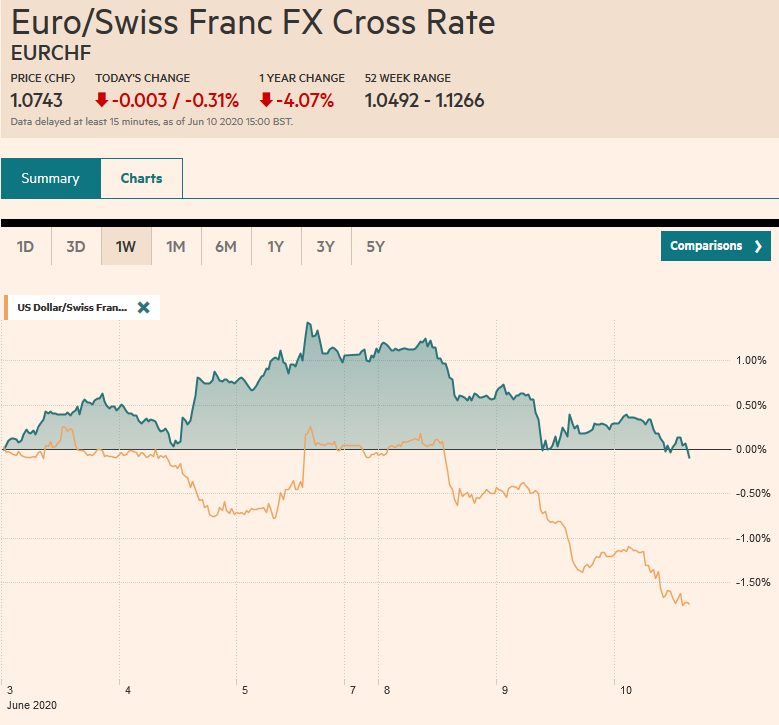

Swiss FrancThe Euro has fallen by 0.31% to 1.0743 |

EUR/CHF and USD/CHF, June 10(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The pullback ins US shares yesterday has not derailed the global advance. Japanese and Chinese markets were mixed, the Hang Seng slipped, and Indonesia was hit with profit-taking, but the MSCI Asia Pacific Index eked out a small gain. It has fallen once past two and a half weeks. The Dow Jones Stoxx 600 opened higher but is falling for the third consecutive session. It has fallen 1.5% over the past two sessions, and US shares are trading a little lower. Benchmark 10-year bond yields are narrowly mixed. The US 10-year yield that was flirting with 90 bp at the end of last week is struggling to hold above 80 bp now. North American operators sold into the dollar’s bounce that was seen in Asia and the European morning yesterday. The greenback is under pressure today, falling against all the majors but the Scandis and most emerging market currencies. The dollar made new lows for the move against the yen and British pound. The Indonesian rupiah, which has been the strongest of the Asian emerging market currencies over the past month (6.7%), is lower for the third consecutive session. Nevertheless, corrective/consolidative forces, perhaps ahead of the FOMC meeting, still seem to grip the foreign exchange market. Gold, which saw $1670 last week, is back testing $1720. Nearby resistance is seen near $1725 and then $1734, a four-week downtrend line. Crude oil prices are giving back yesterday’s gains. The API reported an 8.4 mln barrel build, which, if confirmed by the EIA, would be the largest in nearly two months. |

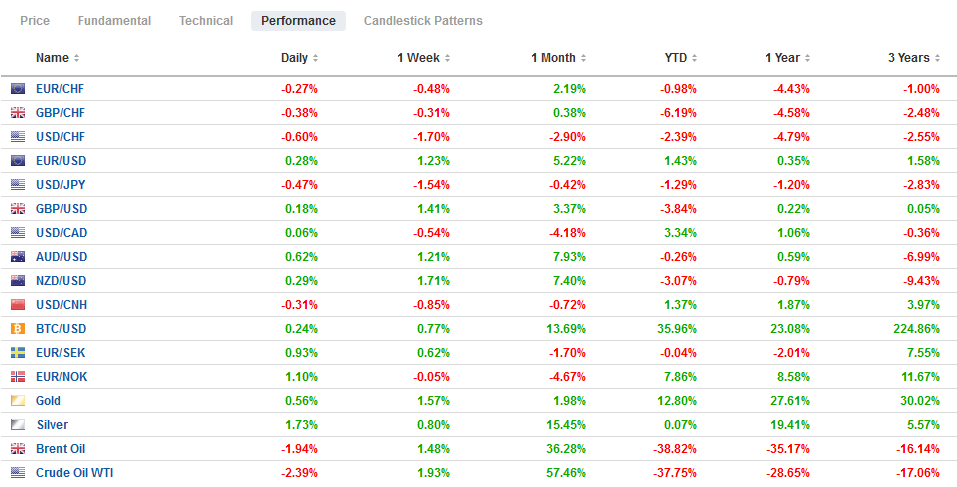

FX Performance, June 10 - Click to enlarge |

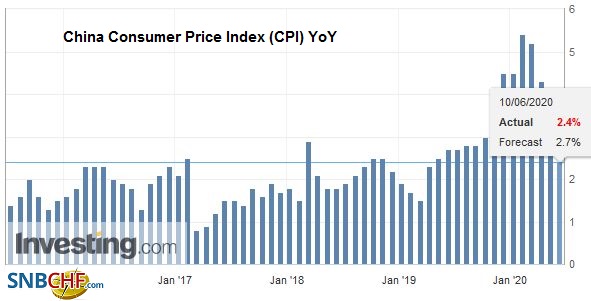

Asia PacificChina’s data reports included May CPI and PPI, and lending figures. The May CPI fell to 2.4% from 3.3% in April, and the decline was more than economists expected. Pork prices fell on the month, and food prices in general moderated. In May, they were up 10.6% from a year ago, 3.5 percentage points lower than in April. |

China Consumer Price Index (CPI) YoY, May 2020(see more posts on China Consumer Price Index, ) Source: investing.com - Click to enlarge |

| Non-food prices rose 0.4% year-over-year. Separately, the deflation in producer prices, which is also a proxy for income and profits of producers, continued. Producer prices were 3.7% lower than a year ago, after falling 3.1% in April. These reports help fan expectations that the PBOC will continue to ease monetary policy. |

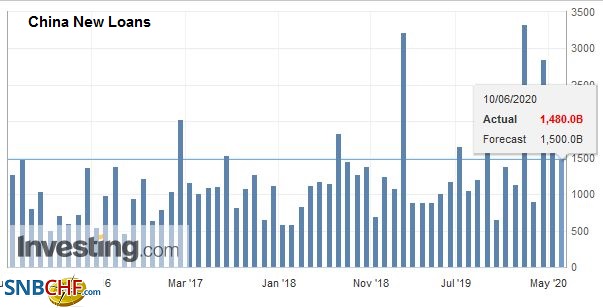

China New Loans, May 2020(see more posts on China New Loans, ) Source: investing.com - Click to enlarge |

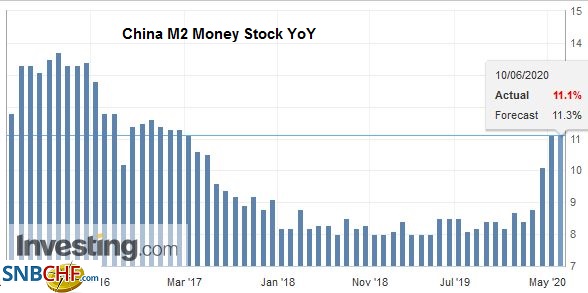

| Meanwhile, aggregate lending remained strong (CNY3.19 trillion) in May, which represents a small acceleration from April (CNY3.09 trillion). Bank lending slowed, implying that the non-bank financial institutions (shadow banking) increased. |

China M2 Money Stock YoY, May 2020(see more posts on China M2 Money Stock, ) Source: investing.com - Click to enlarge |

Japan also reported deflation in producer prices. The 2.7% year-over-year decline in May producer prices was a bit faster than expected after a 2.4% decline in April. Separately, core machinery orders, a proxy for capital expenditures, fell 12%, considerably more than the 7% decline projected by the median forecast in the Bloomberg survey. The BOJ meets next week, and at most, economists see the possibility of tweaking the support for large businesses.

The Hong Kong Monetary Authority continues to defend the upper end of the Hong Kong dollar’s band. In contrast, the forward points continue to unwind the surge seen after the US began looking into removing its special trade privileges. The lack of follow-up has eased anxiety, while flows drawn to IPOs and interest rates keep the HK dollar firm. The PBOC set the dollar’s reference rate a little above where models suggest, as it tries to slow the dollar’s fall. The greenback fell to about CNY7.0625, its lowest level since the end of April.

The US dollar fell below JPY107.30 to set a new low here in June. It has stabilized in the European morning, but the trendline off the May lows has been broken, and now may serve as resistance near JPY107.65. A break of JPY107 would target the JPY106 area. The Australian dollar traded on both sides of Monday’s range yesterday, and the close was 1/100 of a cent below Monday’s low. It bounced back to straddle the $0.7000-area today. Still, corrective/consolidative pressures are still evident. Yesterday’s high was near $0.7040.

Europe

The first 3-month dollar-swap between the Fed and the ECB expires tomorrow. It was for almost $76 bln. At today’s auction, European banks took only $480 mln. This is confirmation of the normalization of the funding markets. Yesterday, the demand at the BOJ’s dollar-auction to replace the three-months swap saw demand halved.

French industrial output for April was horrific. It imploded by 20.1% on the month, with manufacturing tanking nearly 22%. The German figures were reported last week and showed an approximately 18% contraction. The aggregate data for the eurozone will be published ahead of the weekend, and a 20% drop in expected.

The UK, which was the first G7 country to join China’s Asian Infrastructure Investment Bank, is making a significant diplomatic u-turn. It is going to gradually reduce ties with Huawei. It is looking like others have done, to tightened direct investment rules to deter state-owned companies from taking over UK businesses. It will also look to reduce its reliance on imports from China. The UK has also offered to take more immigrants from Hong Kong. Meanwhile, trade talks with the EU are not going well, and some EU countries, including Ireland, are urging the region to prepare the disruption that is likely if the UK and EU do not reach a new trade deal. Prime Minister Johnson and EU President von der Leyen could talk soon to see if politicians can break the stalemate.

The euro recovered smartly yesterday and posted a big outside up day. It has extended its recovery today but has stopped shy of last week’s high near $1.1385 in the European morning. There is an option for about 715 mln euros at $1.1390 that expires today. Initial support is seen a little above $1.1330. There is an option for one billion euros at $1.13 that expires today. Sterling also saw a brilliant recovery yesterday, and follow-through buying today has lifted it to about $1.2785. The next important chart resistance is near $1.30. Support is seen near $1.27, and the 200-day moving average is just below there.

America

The FOMC meets today amid an incredible rally in equities and a bearish steepening of the yield curve. No doubt the Fed welcomes the preliminary evidence that the economy has begun to recover. However, the FOMC is likely to be more cautious last week’s employment data than the speculators who used it as yet another reason to buy risk assets. They know full well that reaching its objectives will be a formidable struggle, and this will likely be borne out by the new economic forecasts that were eschewed during in fog of March. Officials recognize that additional action from the central bank may still be needed. Yet, more than lending is necessary. Spending is required, and Chair Powell is likely to reiterate the need for more fiscal support and extending existing efforts. There are many unknowns, and the course of the virus remains uncertain.

Powell has shown a sensitivity to the disparity of income and wealth. Besides pushing further on full employment, there may be little a central bank can do about the disparity of income. The disparity of wealth is more complicated because its reach is limited. It has innovated in this crisis by having facilities that encourage lending to small and medium-sized businesses, which it did not do during the Great Financial Crisis. Monetary policy has been asked to do a great deal, but there are still limits. However, it can target something further out the curve than overnight money. While we increasingly expect that yield-curve control will be adopted, we think it might not be quite ready now. That said, it may be preferable to do it from a position of strength rather than being perceived to have been backed into it by speculators, so the narrative would go, that previously tried to force the adoption of negative interest rates.

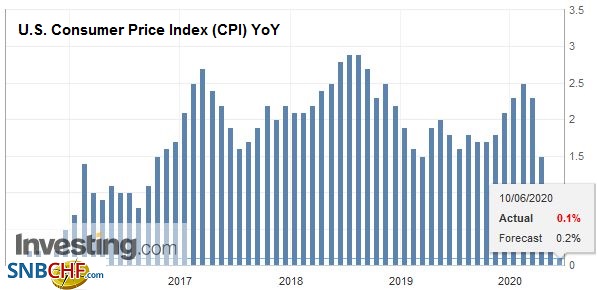

| The US reports May consumer prices. They are expected to be flat at both the headline and core levels. This will keep the year-over-year rate at about 0.3% for the headline and around 1.3% (from 1.4%) at the core level. |

U.S. Consumer Price Index (CPI) YoY, May 2020(see more posts on U.S. Consumer Price Index, ) Source: investing.com - Click to enlarge |

| There is no policy implication. The Fed targets the PCE deflator and often talks about the core PCE deflator. The headline PCE deflator stood at 0.5% in April, and the core deflator was at 1.0%. Inflation and market-based inflation measures suggest the Fed can continue to focus on 1) ensuring the capital markets and bank lending functioning and 2) support the nascent recovery. |

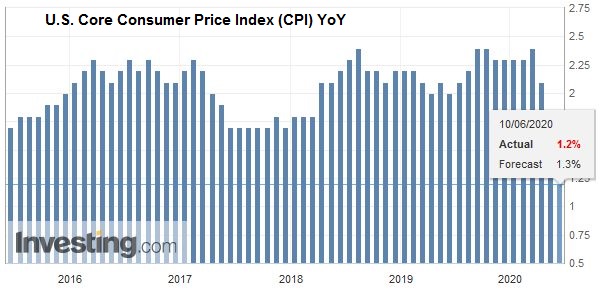

U.S. Core Consumer Price Index (CPI) YoY, May 2020(see more posts on U.S. Core Consumer Price Index, ) Source: investing.com - Click to enlarge |

The US dollar is finding support ahead of CAD1.3350, but the upside seems capped near previous support near CAD1.3460, which is also where the 200-day moving average is found. Initial resistance is around CAD1.3430. The greenback rose from about MXN21.47 yesterday to almost MXN22.00. Since breaking below MXN22.00 on June 2, it has not resurfaced above it. Although it closed on its highs, there was no follow-through dollar buying. Still, corrective forces are evident. Initial support is now seen near MXN21.70.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,China Consumer Price Index,China M2 Money Stock,China New Loans,Currency Movement,EUR/CHF,federal-reserve,Gold,newsletter,U.S. Consumer Price Index,U.S. Core Consumer Price Index,USD/CHF