Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

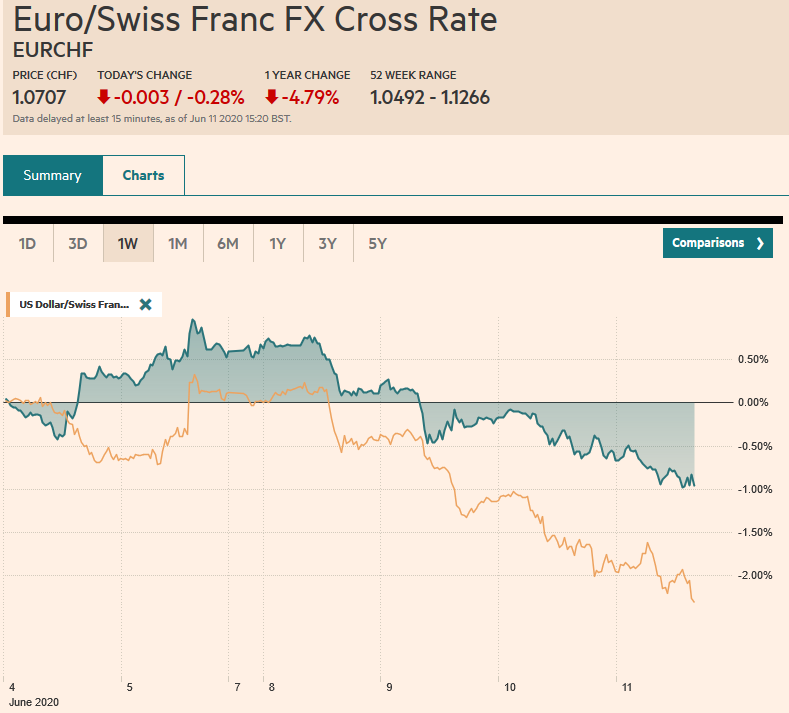

Swiss FrancThe Euro has fallen by 0.28% to 1.0707 |

EUR/CHF and USD/CHF, June 11(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

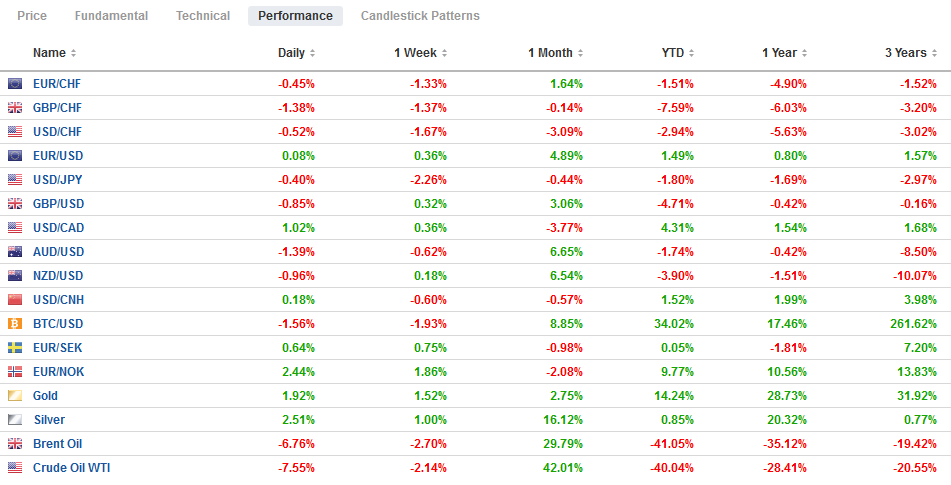

FX RatesOverview: Many observers are attributing the sell-off in risk assets today to the Federal Reserve’s pessimistic outlook, yet, as we note below, the Fed’s median GDP forecast this year is better than many international agency forecasts, including the OECD’s that was issued yesterday. Moreover, some near-term trends were already in place. Although the MSCI Asia Pacific Index snapped its longest advance in three years today, Europe’s Dow Jones Stoxx 600 is lower for the fourth consecutive session, and the S&P 500 will likely fall today for the third successive session. Both of these streaks are the longest since the first half of March. Bond yields are tumbling. The US 10-year yield, which had been flirting with 90 bp at the end of last week, is struggling now to hold above 70 bp. European benchmark yields are 2-5 bp lower after the Australian and New Zealand yields fell 8-9 bp. The dollar itself is mixed against the majors. The recently high-flying dollar-bloc and Scandis are down the most, while the Swiss franc and yen are higher. The euro is holding its own, while sterling is in the high beta camp of weaker currencies today. Led by the liquid and accessible currencies, like the Mexican peso, Russian rouble, and the South African rand, the JP Morgan Emerging Market Currency Index is off for the third consecutive session. Meanwhile, gold is consolidating is gains that carried it to almost $1740 yesterday, and July WTI is unwinding its recent gains to return to where it settled last week (~$38.20). |

FX Performance, June 11 - Click to enlarge |

The Abe government is considering extending its cash payment of JPY100k (~$940) to Japanese citizens living abroad. It would be funded out of the second supplemental budget. The requirement is the person would have to be on the resident register as of late April. The latest figures available showed 1.39 mln Japanese were on the register at the end of 2018. It raises the question of whose economy will be stimulated by the measures: the Japanese economy as the payment is in yen or will it boost spending in the current locale of the ex-pat.

Separately, Japan reported that last week, investors bought more than JPY1.06 trillion of foreign bonds. This was the most since the first week of March. We are reluctant to read much into it. The buying seems to be seasonal at the start of the quarter. For their part, foreign investors sold almost JPY740 bln of Japanese bonds. This is the largest weekly divestment since late March and offsets the purchases of the past three weeks in full. Equity transactions were unremarkable.

Hong Kong Monetary Authorities appear to have continued to intervene to prevent the US dollar from falling through the lower band. The recent inflows appear drawn to the new IPOs. This demand is likely to ease over the next week. The greenback initially extended its loss against the Chinese yuan, falling to about CNY7.0560, the lowest since the end of April, before bouncing to CNY7.0750 and running out of steam. The reference rate was set a little above CNY7.06, which was a bit firmer for the dollar than the models suggested.

The US dollar extended its losses against the yen to about JPY106.80. It is the fourth consecutive session the greenback is moving lower after peaking at the end of last week shy of JPY110. While the JPY106.45 may offer some support, the next important level is near JPY106.00. The JPY107.30 area now maybe resistance. The Australian dollar’s seven-rally ended Tuesday, and it has been consolidating, albeit choppily, since. Today’s setback saw it approach the week’s low (~$0.6900), and recover toward the middle of the roughly one-cent range today or around $0.6955 in the European morning. It settled last week near $0.6970.

Europe

European finance ministers meet again today to try to see if a meeting of the minds is possible ahead of next week’s heads of state summit to ideally agree on a European Recovery Fund. It seems as if some of the objections were largely negotiating tactics. Denmark, for example, has indicated that while it is still skeptical of the subsidy component (grants), its priority is that it maintains its EU budget rebate. Austria suggested a similar approach is possible. There are still some principled objections for others, including Eastern and Central Europe. Note too that Eurogroup (finance ministers of the eurozone) head Centeno term ends next month, and he has indicated he will step down. Spain’s finance minister Nadia Calvino seems to be the early favorite.

The US threatened tariffs on European autos if it did not cut the tariffs on US lobsters recently, but that may be a sideshow to the coming clash over the digital tax of several European countries. The issue slowly working its way through the US channels, and it is getting closer to the surface. It could become the next important flashpoint.

The euro initially rallied to new highs after the FOMC meeting and briefly poked above $1.1420 before pulling back in late Asia to test yesterday’s lows near $1.1325. It has climbed back to $1.1400 in the European morning. While the North American session has seen the euro bid more often than not over the past few weeks, the intraday technicals warn that consolidation may be the most likely scenario today. On the upside, many have their near-term sights set at $1.15, where there are some chunky options that expire next week. Sterling rose to almost $1.2815 after the FOMC meeting and drifted down until reaching the $1.2650 in the European morning. It was bid back to yesterday’s lows (~$1.2725). It needs to get above $1.2750 to signal a retest on the highs. The downtrend line that connects last December’s election highs and the early March high is found near $1.2875 now. Consolidation here too looks likely.

America

The Federal Reserve confirmed that US rates will remain low for some time. Only two of the 17 Fed officials expect that a hike before the end of 2022 will be warranted. Its growth forecasts are a bit above others (OECD forecast the US economy would contract by 7.4% this year compared with the median Fed forecast a 6.5% decline in output). Still, it committed to buying no less than $80 bln a month of Treasuries and $40 bln of mortgage-backed securities (which is the current pace). Although unemployment may not have peaked, the median forecast is for 9.3% at the end of this year and 6.5% at the end of next year. The headline PCE, which the Fed targets at 2%, is forecast (median) at 0.8% in 2020 and 1.6% next year.

While last week’s May employment report may have led some, including in Congress, to question the merits of more fiscal support, this is not a majority view. Powell also advocated more fiscal stimulus is needed as there were limits on monetary policy (lend but not spend). Treasury Secretary Mnuchin also has endorsed more measures. That is what is being negotiated. Not if to spend, but how and where. Mnuchin cited the need for support for retail, travel, and leisure. The $600 extra weekly unemployment compensation is set to expire at the end of next month. The battle over it is likely to intensify. We suspect a compromise will be found to extend it but perhaps at a reduced level. Separately, it still seems premature to look past the virus despite (or because) of the relaxations that seem to be going forward. There is a spike in several re-opened states. Texas reported its highest one-day number of infections, and Florida reported the most new cases in a seven day period. Hospitalizations in California have risen for nine of the past 10 days top reach their highest in nearly a month.

The US reports May producer prices today. Deflation is expected to be evident in the headline rate. Excluding food and energy, producer prices are forecast to slip closer to zero from 0.6% in April. However, at the same time, weekly jobless claims for last week will be reported. Around 1.5 mln Americans may have filed unemployment benefits for the first time down from nearly 1.9 mln the previous week. Canada has no economic reports, while Mexico publishes its April industrial output figures. In March industrial production fell by 3.4% on the month. In April, the decline is expected to be around 15%.

The US dollar appears to have left a bullish hammer candlestick yesterday, and follow-through buying lifted it to CAD1.35 today. It reached almost CAD1.3315 yesterday. A move above CAD1.3515 would target the CAD1.3630 area initially. The dollar has carved a base around MXN21.45-MXN21.50 in recent sessions. We suspect there is potential toward MXN23.00-MXN23.25 in the coming days. One step at a time, though, and today it has tested the MXN22.32 area. The nearby resistance is around MXN22.40. Initial support is likely around yesterday’s highs (~MXN22.00).

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$CNY,Currency Movement,EU,EUR/CHF,federal-reserve,Japan,newsletter,USD/CHF