Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

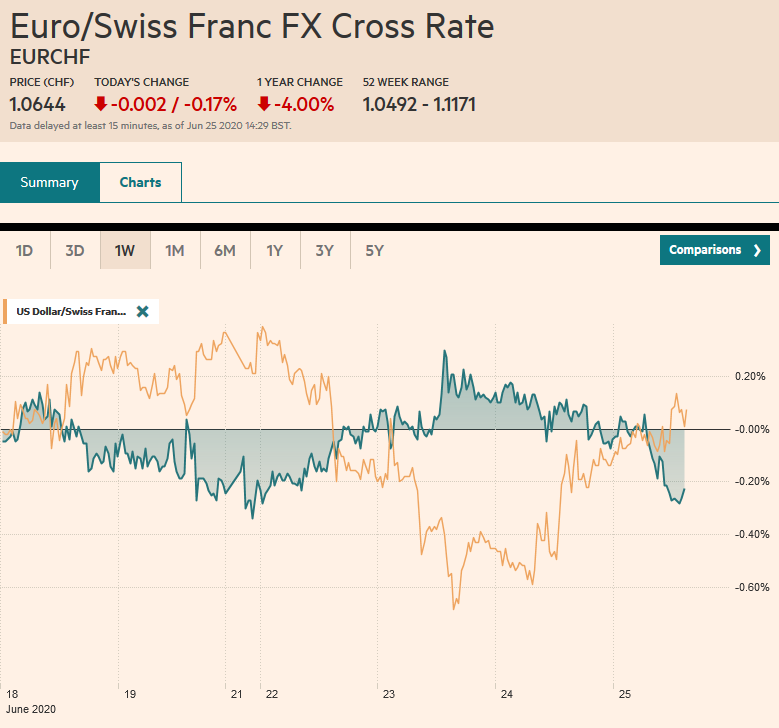

Swiss FrancThe Euro has fallen by 0.17% to 1.0644 |

EUR/CHF and USD/CHF, June 25(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Given the huge run-up in risk assets this quarter, and the technical indicators warning of corrective forces, concerns over the new infections is pushing on an open door. The S&P 500 gapped lower yesterday and fell 2.6%, led by energy and airlines. The NASDAQ snapped an eight-day rally. Follow-through selling in the Asia Pacific region saw most markets fall at least 1%, with Korea and Australia seeing losses in excess of 2%. China, Hong Kong, and Taiwan markets were closed for national holidays. European shares opened lower but have steadied after dropping about 2.8% yesterday. US shares are trading with a downside bias. Bonds are mostly little changed, while peripheral spreads in Europe are a little wider. The US 10-year yield is about 67 bp, the lower-end of a two-week range. The foreign exchange market is subdued. The New Zealand dollar, which was hit the hardest yesterday (-1.25%), is leading the majors higher today with around a 0.4% gain. The dollar-bloc currencies and the Swedish krona, along with sterling, are firmer, while the euro, yen, and Swiss franc are nursing small losses. Emerging market currencies are mostly lower. Gold reached only $1780 yesterday before reversing lower. It found support above $1755 today. Oil is stabilizing after yesterday’s slide. The August WTI contract fell 5.8% yesterday and eased further today to almost $37 a barrel before returning to the $38-area. |

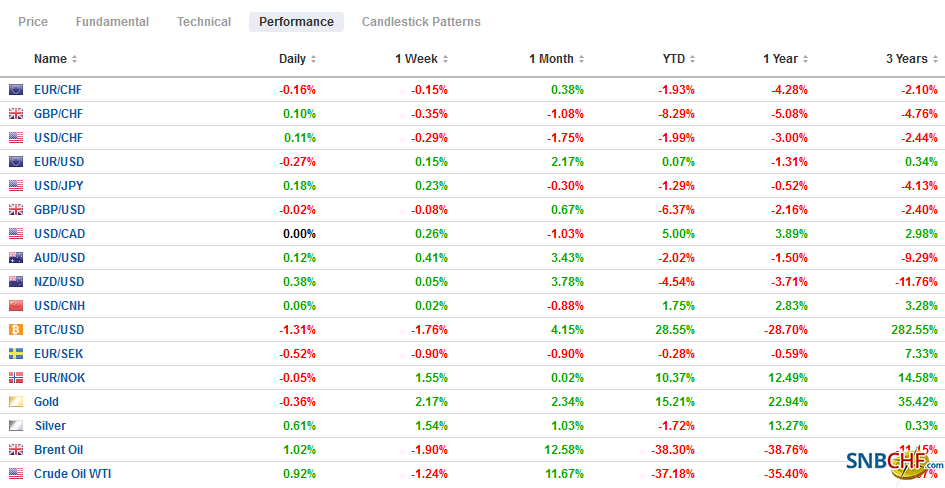

FX Performance, June 25 - Click to enlarge |

Asia Pacific

Japan reported its All-Industries Activity Index plummeted 6.4% in April after a revised 3.4% decline in March (initially -3.8%). Japan’s economy contracted in Q4 19 and Q1 20, and a third quarterly decline is likely before a recovery in the second half.

The Philippines’ central bank surprised the market with a 50 bp rate cut. The overnight deposit rate sits at 1.75%, and the overnight borrowing rate is 2.25%. The market seemed to have been split between no change and a 25 bp cut. Monetary policy is bearing the brunt as the fiscal response has been limited. The central bank has cut rates by 150 bp in the past three meetings, cut reserve ratios, and provided liquidity. With inflation near 2%, the central bank may be hesitant to cut rates further.

After falling to almost JPY106 on June 23, perhaps linked to yen-demand related to Softbank divestiture of T-Mobile, the dollar recovered yesterday and extended those gains today to almost JPY107.30, its highest level since the middle of last week. There is an option for about $500 mln at JPY107.40 that expires today, and another one at JPY107.00 for around $475 mln. The JPY107.50-JPY107.65 area may offer formidable near-term resistance. Australia reported its largest single-day increase in infects in a couple of months, but Aussie found support near $0.6850 after peaking earlier this week around $0.6975. Look for offers in the $0.6880-$0.6900 to cap it today.

Europe

French President Macron has proposed a new furlough program that could cover a large share of lost income for up to two years starting next month. If employers and unions agree on fewer hours to protect job security, the government will pay 85% of the costs for up to two years. The government would cover 80% of the deals struck after October 1. The government will also foot 80% of the bill for re-training.

The ECB took a fresh initiative today that caught the market by surprise and is helping lift the European financial shares today. The central bank will establish a new precautionary facility to provide euros to central banks outside of EMU to help address liquidity issues that may arise from the crisis. The new backstop, EUREP, will be available until the middle of next year. It will lend euros against collateral of euro-denominated paper from eurozone governments and supranationals. This is an important initiative. The ECB had been criticized during the Great Financial Crisis for not doing enough to help ease the liquidity crisis in eastern and central Europe.

The ECB will reportedly give the Bundesbank documents that it had previously shared with the European Court of Justice regarding its considerations of proportionality. The Bundesbank will then share with the German parliament. While this all seems very rational, the problem is that it still allows the German court ruling to impinge on the European Court of Justice ruling, and leaves open the challenge to the primacy of EU law. Separately, note that Macron and Merkel will meet on June 27, apparently to talk about German taking over the rotating EU presidency in H2 and the EU Recovery Fund. Lastly, despite cries that the US decision to remove troops from Germany was an “abandonment” of Europe, there are reports today suggesting a redeployment, like we suggested, to Poland.

The euro peaked Tuesday near $1.1350 and fell to about $1.1250 yesterday and a little below $1.1220 today, where a 775 mln euro option expires today. The $1.1200 area itself may be more formidable. There is a 1.6 mln euro option there today that rolls off and an expiring 1.9 bln euro option there tomorrow. Initial resistance is now seen near $1.1240 and then $1.1260. Sterling found support ahead of $1.24 in Asia and early European activity today after peaking this week near $1.2550. However, the buying interest faded around $1.2465, and another try at $1.2400 looks likely. Note that Turkey’s central bank decision on rates is still awaited. It is expected to announce a 25 bp rate cut to bring the one-week repo rate to 8%. The lira is slightly weaker for the third consecutive session.

America

Fitch took away Canada’s AAA rating yesterday, citing the pandemic-inspired increase in the country’s deficit and debt. The other two major rating agencies see Canada as a triple-A credit. Fitch says almost, but not quite at AA+. This year’s deficit of around 12.5% this year (~1% in 2019) will lift Canada’s debt to about 115% of GDP. It leaves Germany as the only AAA-rated sovereign by the three main agencies in the G7.

| The market may not have been surprised as much as some media outlets suggest. As investors and economists thought through the implications of Canada’s fiscal response, it was not so far-fetched. We had highlighted the risk in our May monthly. If anything, after the announcement, the pullback in the Canadian dollar accelerated. The 10-year yield finished unchanged a little below 55 bp. Owing to a rise in the consumer staple sector, the S&P/Toronto Stock Composite Index fell by around 1.75% (S&P 500 fell by about 2.6%). |

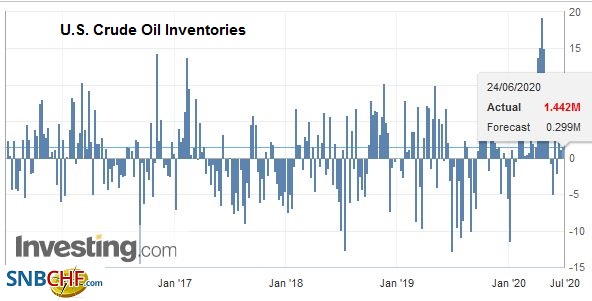

U.S. Crude Oil Inventories, June 25 2020(see more posts on U.S. Crude Oil Inventories, ) Source: investing.com - Click to enlarge |

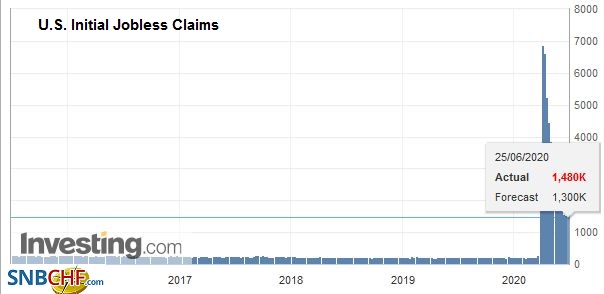

| The US reports weekly jobless claims, which have been stickier than many expect. More than 1.3 mln new filings are expected after 1.5 mln previously. May durable goods orders are expected to have jumped back in May (~10%) after collapsing by 17.7% in April. Also, the May trade balance will be reported. The deficit is expected to be around $68 bln. |

U.S. Initial Jobless Claims, June 25 2020(see more posts on U.S. Initial Jobless Claims, ) Source: investing.com - Click to enlarge |

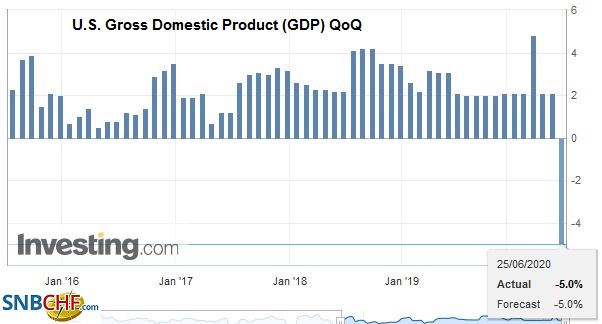

| The GDP estimate for Q1 is unlikely to change much from the 5% previously reported. Mexico reports April retail sales (median forecast in the Bloomberg survey is for an 18% decline (-0.8% in March). However, the highlight for Mexico today will be the Banxico rate decision. Most expect a 50 bp cut to bring the overnight target to 5.0%. |

U.S. Gross Domestic Product (GDP) QoQ, Q1 2020(see more posts on U.S. Gross Domestic Product, ) Source: investing.com - Click to enlarge |

The US dollar bottomed near CAD1.3485 two days ago and rose to CAD1.3640 yesterday. It edged up to CAD1.3665 in Asia before pulling back to almost CAD1.3600 in Europe. It could ease a little more, but the upside may be the path of least resistance, especially if equities remain soft. The greenback made a marginal new high for the month against the Mexican peso, reaching almost MXN22.9750. A break of MXN23.00 would initially target the MXN23.25 area. Support is seen around MXN22.70. The S&P 500 approached its 200-day moving average (~3020) yesterday, and a break targets the month’s low set on June 15 around 2965.50. On the upside, the gap created by yesterday’s sharply lower opening (~3115 to 3127) offers important resistance.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,Canada,Currency Movement,ECB,EUR/CHF,France,FX Daily,newsletter,Philippines,U.S. Crude Oil Inventories,U.S. Gross Domestic Product,U.S. Initial Jobless Claims,USD/CHF